Energy and Power Market Research Reports & Consulting - The report captures in-depth strategic insights on crucial topics which helps our clients make their informed decisions

The global generator sales market is expected to grow at a CAGR of 5.9% during the forecast period. It is estimated to be USD 19.9 billion in 2021 and is projected to reach USD 26.5 by 2026. The major factors driving the generator sales market include the growing demand for uninterrupted and reliable power as some of the best power grids are also subject to downtime, growth of healthcare infrastructure, rising demand for IT infrastructure management, and rapid urbanization in developing countries.

The other fuel type segment which includes propane, LPG, and bio-diesel is expected to be the fastest growing fuel segment of the generator sales market from 2021 to 2026. Countries around the world have set emission reduction targets and are working toward achieving these targets, which has resulted in the increased share of environmentally friendly fuel for power production. Countries such as the US, Brazil, Canada, Germany, France, and the UK are expected to increase their focus on environmentally friendly technologies, driving the market for propane, LPG, and bio-diesel-powered generators during the forecast period.

The industrial segment is expected to be the fastest growing generator sales market, by end-user, during the forecast period. The industrial end-user segment includes the utility/power generation, oil & gas, and other industries such as mining, marine, chemicals, military, and manufacturing. Growth of the oil & gas sector in China, Mexico, the US, Canada, and African countries is creating a new market for generator sets. Also, the growth of the manufacturing sector in Asia Pacific is expected to drive the demand for generators.

The 1,000–2,500 kVA power rating segment is expected to be the fastest growing segment of the generator sales market during the forecast period. 1,000–2,500 kVA generators are mainly used for CHP plants, large manufacturing units, power plants, and marine applications. The above 1,000–2,500 kVA generators are economical and can be deployed for continuous power applications. The adoption of natural gas and other renewable gases for the 1,000–2,500 kVA generators is the major reason for the fastest growth projection of the segment during the forecast period.

Asia Pacific is expected to be the fastest growing market for generator sales from 2021 to 2026, followed by the North America. Countries such as the US, China, Canada, and India are the largest markets for generator sales. India and China are rapidly developing large economies. Both countries are implementing policies to boost their industrial sectors. Inadequate power transmission & distribution networks in developing countries in Asia Pacific are also expected to create a demand for generator sets. Due to these factors, Asia Pacific is projected to grow at the highest CAGR during the forecast period.

The major players in the generator sales market are Caterpillar (US), Cummins (US), Rolls-Royce Holdings (UK),Mitsubishi Heavy Industries, Ltd. (Japan), and Generac (US). Between 2017 and 2021, the companies adopted growth strategies such as new product launches, contracts & agreements, mergers & acquisitions, and expansions to capture a larger share of the generator sales market.

Browse Related Reports:

Asia Pacific Generator Sales Market by Fuel Type (Diesel, Gas), Power Rating (<100kVA, 100-350kVA, 350-1000-2500kVA, 2500-5000kVA, >5000kVA), Application (Standby, Continuous, Peak Shaving), End-User, Country - Forecast to 2025

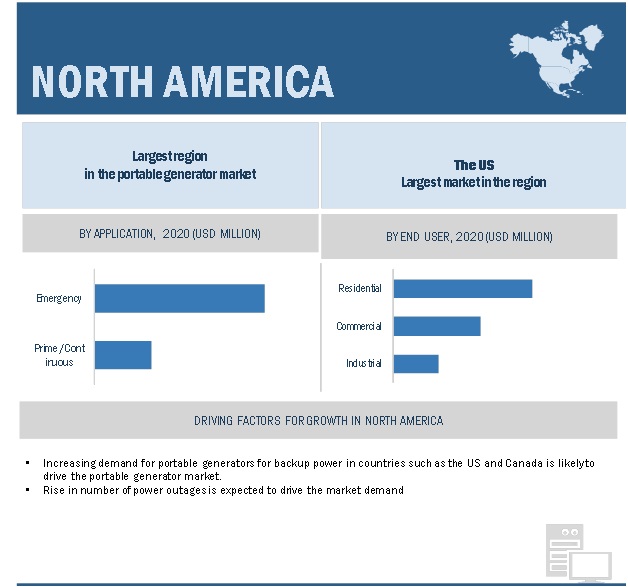

Portable Generator Market by Fuel (Gasoline, Diesel, Natural Gas, Others), Application (Emergency, Prime/Continuous), Power Rating (below 5 kW, 5–10 kW, 10–20 kW), End User (Residential, Commercial, Industrial), and Region - Global Forecast to 2026

The portable generator market is projected to reach USD 2.5 billion by 2026 from an estimated USD 1.8 billion in 2021, at a CAGR of 6.7% during the forecast period. Increasing instances of power outages owing to aging grid infrastructure and extreme weather conditions are the key factors driving the growth of the portable generator market. Increasing adoption of dual fuel and inverter portable generators are expected to offer lucrative opportunities for the portable generator market during the forecast period.

Impact of COVID-19 on portable generator market:

COVID-19 has slowed the growth of the portable generator market, as countries were forced to implement lockdowns during the first half of 2020. Strict guidelines were issued by governments and local authorities, and all non-essential operations were halted. This adversely affected the portable generator market owing to the suspension of activities of end users.

In addition, production and supply chain delays were also witnessed during the second quarter which poised a challenge to the portable generator market, since end-user industries were still not operating at their full capacity.

Asia Pacific is expected to grow at the highest CAGR during the forecast period. Asia Pacific region has been segmented, by country, into China, India, Japan, South Korea, Australia, and Rest of Asia Pacific. Rest of Asia Pacific includes Indonesia, Singapore, Malaysia, Taiwan, and Thailand. The region is the most populated region in the world and is expected to become the largest energy-consuming region globally. It comprises many developing countries and requires more energy for its development. According to the Asian Development Bank (ADB), the region’s share of global energy consumption is expected to increase to 56% by 2035 from 34% in 2010. The industrial sector in China contributed more than 37% of its GDP in 2020. The growth of the industrial sector has tremendously increased power production and consumption in China. These factors have made China one of the most lucrative markets for the power industry. Thus, increase in demand for power is likely to offer growth opportunities for portable generator market during he forecast period.

The portable generator market, by application, is segmented into emergency and prime/continuous. The emergency segment, by application, is projected to hold the highest market share during the forecast period. The growth of this segment is driven by increasing weather-related power outages and aging power generation & distribution networks. Furthermore, the usage of portable generators during emergency backup can prevent food from spoiling, keep lights on, and help in other day-to-day requirements.

The report segments the portable generator market, by fuel, into gasoline (petrol), diesel, natural gas, and others. Others includes LPG, propane, and biodiesel. The market for gasoline (petrol) is expected to hold the highest market share during the forecast period. It is majorly used for temporary, intermittent, or low-load applications. Gasoline is a common source of fuel and the easiest to obtain. It is mostly used for running portable generators for a shorter period of time, which is likely to increase their demand in the portable generator market globally.

On the basis of power rating, below 5 kW, 5–10 kW, and 10–20 kW. The market for gasoline (petrol) is expected to hold the highest market share during the forecast period. The 5–10-kW portable generator, by power rating, is projected to hold the highest market share during 2021–2026. The market for these generators is projected to grow because of the increase in awareness of in-house power backup and demand for portable powering systems in outdoor recreational activities.

The portable generator market, by end user, into residential, commercial, and industrial. The residential segment is expected to hold the highest market share during the forecast period. The increasing number of frequent blackouts and insufficient power supply in some parts of Africa and South America are expected to boost the demand for residential portable generators.

Asia Pacific Generator Sales Market by Fuel Type (Diesel, Gas), Power Rating (<100kVA, 100-350kVA, 350-1000-2500kVA, 2500-5000kVA, >5000kVA), Application (Standby, Continuous, Peak Shaving), End-User, Country - Forecast to 2025

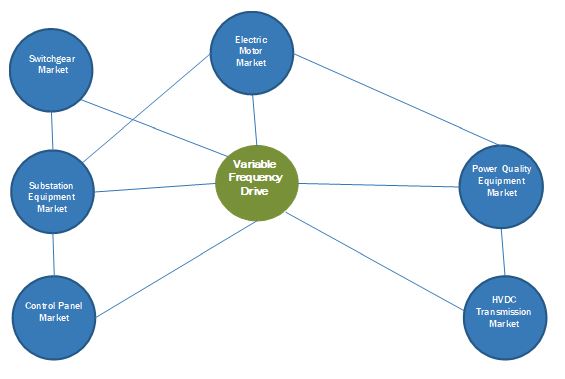

The global variable frequency drive market

is estimated USD 19.2 billion in 2020 and is projected to reach USD

24.3 billion by 2025, at a CAGR of 4.8% during the forecast period. This

growth can be attributed to factors such as the growth of supportive

regulatory environment towards effective and efficient energy

utilization, the upgradation and modernization of aging infrastructure

for safe & secure electrical distribution systems, and rapid

industrialization and urbanization across the globe. However, the

stagnant growth of the oil & gas industry coupled with the decrease

in the exploration & production activities are hindering the growth

of the variable frequency drive market.

The low voltage segment is expected to hold the largest share

of the variable frequency drive market, by voltage type, during the

forecast period

The low voltage segment segment, by voltage, is estimated to account

for the largest share during the forecast period. Low voltage variable

frequency drives are used across a wide range of applications including

pumps, fan, belt conveyor, centrifugal pumps, and centrifugal

compressors. These drives are designed for industrial applications,

especially in process industries such as pulp & paper, power, water

& wastewater, and oil & gas. Thus, the increasing use of low

voltage drives in a wide range of applications is expected to boost the

growth for this segment

The low power drive segment, by power rating, is expected account for the largest share during the forecast period

The low power drive segment is expected to hold the largest market

share and is projected to grow with the highest CAGR during the forecast

period. Low power drives, due to higher energy savings at low capital

costs and better process control with increased motor control, offer a

quick payback period. Variable frequency drives with a 6–40 kW power

range are used across various industries such as building, automation,

oil & gas, food & beverage, and pulp & paper. Therefore, the

growing need for energy efficiency in the respective industries is

expected to drive the growth of the segment.

Asia Pacific: The leading variable frequency drive market

The Asia Pacific region is estimated to be the largest and fastest

growing variable frequency drive market during the forecast period. The

growth of this region is primarily driven by countries such as China,

South Korea, India and Japan, which are considered as the main

manufacturing hubs for variable frequency drives. Countries in Asia

Pacific are focused towards energy efficiency and variable frequency

drives are expected to play an important role in helping these countries

to meet their energy efficiency targets, as the primary function of

these drivers is to save energy. Thus, The rapid industrialization due

to growing automation in manufacturing sector and increased investments

in renewables sector are driving the growth of the variable frequency

drive market in the Asia Pacific region.

The growth in industrialization is driving a continuous need for

electric motors, which consume one-third of the total electricity

produced globally. The factors such as limited conventional power

generation and the continuous rise in electricity prices, has encouraged

companies to invest in energy-efficient equipment to increase energy

efficiency. Industries such as oil & gas, metals & mining, pulp

& paper, cement, and water & wastewater, which are considered to

be energy intensive industries, are using variable frequency drives to

reduce energy consumption and CO2 emissions. Therefore, the increasing

need for energy efficiency is expected to drive the growth of the

variable frequency drives market.

The global variable frequency drive market is dominated by a few

major players such as ABB (Switzerland), Siemens (Germany), Schneider

Electric (France), Danfoss (Denmark), Rockwell Automation (US). These

players have a wide regional presence.

New product launches, investments & expansions, mergers &

acquisitions, contracts & agreements, partnerships, alliances, joint

ventures, and collaborations are few of the key strategies adopted by

the players of the variable frequency drive market. From January 2017 to

December 2020, new product launches was the most commonly adopted

strategy, followed by adoption of mergers & acquisitions as a major

strategy during that period.

ABB is among the leading companies in the automation and power

technologies businesses offering a wide range of products, solutions,

services, and systems to customers in the utility, industrial, and

infrastructure & transportation verticals. The company operates

through 4 business segments, namely, Electrification, Robotics &

Discrete Automation, Industrial Automation, and Motion. Variable

frequency drives are offered through the Motion segment to utilities and

industries. The Motion business segment provides products, services,

and solutions that increase industrial productivity and energy

efficiency. This business segment also offers products such as motors

and generators for a wide range of industrial applications. ABB has its

research centers in 7 countries, namely, China, Germany, India, Poland,

Sweden, Switzerland, and the US. The company currently owns and operates

300 manufacturing plants and has established its operational presence

in over 100 countries. The company marks a global presence—Europe, the

Americas, Asia Pacific, the Middle East, and Africa. ABB has adopted

both organic and inorganic business strategy to enhance its growth in

the variable frequency market. For instance, in January 2019, ABB

launched a series of ACS880 industrial drives and ACH580 Ultra-Low

Harmonic (ULH) HVAC drives, which are used in many industries and

applications to tackle harmonic issues

Siemens is a major technology company with core business activities

in the field of electrification, automation, and digitalization. The

company operates through 6 business segments, namely, Digital

Industries, Siemens Healthineers, Smart Infrastructure, Mobility,

Portfolio Companies, and Financial Services. The company offers variable

frequency drives through the Portfolio Companies business segment. The

other products offered under this business segment are motors,

synchronous condensers, integrated automation systems, electric motors,

converters, generators, gear units, and couplings. The variable

frequency drives offered by the company find applications in the oil

& gas and power industries. Siemens has its operational presence in

Europe, North America, South America, the Middle East, and Asia Pacific.

Through the operation of an accomplished global network of regional

offices, warehouses, R&D facilities, and sales offices, the company

has established its presence in more than 100 countries across the

globe. The company owns and operates factories in Sacramento,

Louisville, Indiana, New Castle, Pittsburgh, Portland, and Georgia,

among many other locations in the US. The company has adopted organic

business strategy for its growth in variable frequency market. For

instance, in April 2018, to extend the performance spectrum of the

synchronous reluctance drive system, Siemens has expanded its product

portfolio of Simotics synchronous-reluctance motors by including two new

shaft heights, AH90 and AH225. These motors are available in a power

range of 0.55–45 kilowatts (kW) and at a speed of 1,500 and 3,000

revolutions.

Browse Related Reports:

Marine VFD Market by

Type (AC Drive, DC Drive), Voltage (Low Voltage (Up to 1 kV), Medium

Voltage (Above 1 kV)), Application (Pump, Fan, Compressor, Propulsion /

Thruster, Crane & Hoist) and Region – Global Forecast to 2024

Switchgear Market to Hit $88.5 Billion by 2025; Rising Investment in Rrenewable Energy Worldwide to Augment Growth

Servo Motors and Drives Market

by Offering (Hardware, Software and Services), Product Type (Servo

Motors, Servo Drives), System, Voltage, Communication Protocol, Brake

Technology, Material of Construction, Industry, and Region – Global

Forecast to 2025

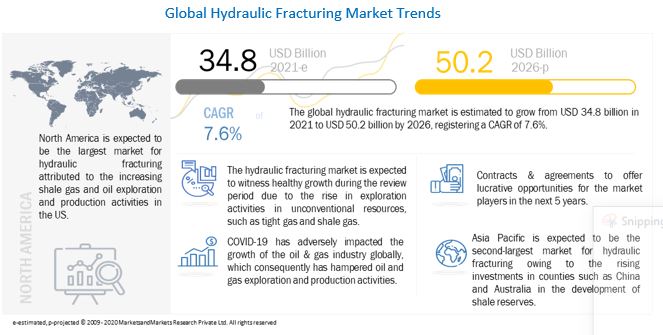

According to the new market research report "Hydraulic Fracturing Market by Well Type (Horizontal Well, and Vertical Well), Technology (Plug and Perf, and Sliding Sleeve), Application (Shale gas, Tight Oil, and Tight gas), and Region - Global Trends and Forecast to 2026" The hydraulic fracturing market is projected to reach USD 50.2 billion by 2026. The hydraulic fracturing market size will grow to USD 50.2 billion by 2026 from USD 34.8 billion in 2021, at a CAGR of 7.6% during the forecast period. The rising primary energy demand and increasing shale gas exploration & production activities in US is the driving factors for the hydraulic fracturing market, globally.

Browse 218 market data Tables and 61 Figures spread through 230 Pages and in-depth TOC on "Hydraulic Fracturing Market - Global Trends and Forecast to 2026"

The horizontal segment is expected to dominate the hydraulic fracturing market, by well type, during the forecast period.

A horizontal well requires a multi-directional drilling technique, which generally drills with an inclination of greater than 80° to enhance reservoir performance. According to the EIA, 70.0% of shale reserves are drilled horizontally in North America. Hydraulic fracturing, along with horizontal drilling, helps to increase crude oil and natural gas production. This is expected to drive the horizontal segment market during the forecast period.

The shale gas segment is expected to be the fastest-growing hydraulic fracturing market, by application, during the forecast period.

The shale gas segment, by application, is estimated to grow at the fastest rate during the forecast period. Shales are fine-grained sedimentary rocks that can be rich sources of petroleum and natural gas. Hydraulic fracturing is the process used to extract shale gas. Deep holes are drilled into the shale rock, followed by horizontal drilling, as shale reserves are distributed horizontally rather than vertically. The increasing demand for natural gas is expected to drive the growth of the hydraulic fracturing market for shale gas applications. The demand in 2021 was 4.021 tcm, up from 3.91 tcm in 2020. Furthermore, the consumption of natural gas in the power sector of the US is expected to reach 12.1 tcf by 2050, up from 0.4 tcf (4%) recorded in 2020. Such factors propel the growth of shale gas segment in the hydraulic fracturing market.

North America likely to emerge as the largest hydraulic fracturing market

In this report, the hydraulic fracturing market has been analyzed for six regions, namely, North America, Latin America, Europe, Asia Pacific, Middle East & Africa. According to the IEA, the US is determined to become the net exporter of energy by 2021 and to fulfill this objective; oil production is being increased across the nation. Moreover, the US is the top explorer and producer of shale oil and gas. The old oil & gas fields in the Permian Basin and Bakken Ford require the hydraulic fracturing operations to enhance the productivity of the wells. Thus, North America dominated the hydraulic fracturing market during the forecasted period.

To enable an in-depth understanding of the competitive landscape, the report includes the profiles of some of the top players in the hydraulic fracturing market.

Some of the key players are Halliburton (US), Schlumberger (US), Baker Hughes Company (US) NexTier Oilfield Solutions (US), and Calfrac Well Services (Canada). The leading players are adopting various strategies to increase their share in the hydraulic fracturing market.

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth niche opportunities/threats which will impact 70% to 80% of worldwide companies’ revenues. Currently servicing 7500 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Our 850 fulltime analyst and SMEs at MarketsandMarkets™ are tracking global high growth markets following the "Growth Engagement Model – GEM". The GEM aims at proactive collaboration with the clients to identify new opportunities, identify most important customers, write "Attack, avoid and defend" strategies, identify sources of incremental revenues for both the company and its competitors. MarketsandMarkets™ now coming up with 1,500 MicroQuadrants (Positioning top players across leaders, emerging companies, innovators, strategic players) annually in high growth emerging segments. MarketsandMarkets™ is determined to benefit more than 10,000 companies this year for their revenue planning and help them take their innovations/disruptions early to the market by providing them research ahead of the curve.

MarketsandMarkets’s flagship competitive intelligence and market research platform, "Knowledgestore" connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : 1-888-600-6441 newsletter@marketsandmarkets.com

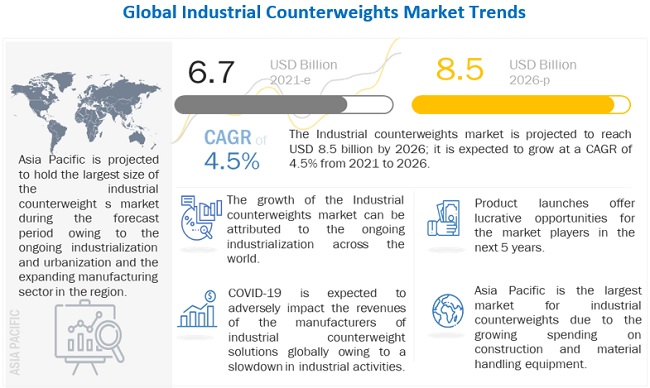

According to the new market research report "Industrial Counterweights Market by Type (Swing Counterweight, Fixed Counterweight), Material (Steel & Iron, Concrete), Application (Elevators, Cranes, Forklift, Excavators, Lifts, Grinding Wheels), End User, and Region-Global forecast to 2026", size will grow to USD 8.5 billion by 2026 (forecast year) from USD 6.7 billion in 2021 (estimated year), at a CAGR of 4.5% during the forecast period. The purpose of a counterweight is to make lifting the load faster and more efficient, which saves energy and is less taxing on the lifting machine. Counterweights are used to counterbalance the weight and maintain stability and are required to complete various operations in industries such as industrial manufacturing, marine, renewables, construction, mining, and agriculture. Increasing demand from the construction industry in the industrial environment to offer lucrative opportunities for the industrial counterweights market during the forecast period.

Browse 191 market data Tables and 45 Figures spread through 222 Pages and in-depth TOC on "Industrial Counterweights Market -Global forecast to 2026"

The fixed counterweights segment is expected to dominate the industrial market, by type, during the forecast period.

The fixed counterweights segment accounted for the largest share of the industrial counterweights market, by type, in 2020. The fixed counterweights segment of industrial fixed counterweights is further classified into two types—fixed frames and floating frames. As the name suggests, the position of the counterweight is stable in the fixed frame, whereas it is rotating in the floating frame.

The iron & steel segment is expected to dominate the industrial market, by material, during the forecast period.

The iron & steel counterweights segment accounted for the largest share of the industrial counterweights market, by type, in 2020. Iron and steel materials are widely used to make counterweights, owing to various desirable properties aligned with them such as high strength, ductility, and tensile strength. Iron and steel are used widely in the construction of roads, railways, buildings, etc. Equipment such as bridge weights, cylindrical weights placed on poles near railway tracks, cranes, and forklifts; modern structures, such as stadiums, skyscrapers, bridges, and airports, are supported by a steel skeleton. Iron and steel counterweights are required for the construction of all the aforementioned equipment and structures.

The cranes segment is expected to dominate the industrial counterweights market, by application, during the forecast period.

The cranes counterweights segment accounted for the largest share of the industrial counterweights market, by application, in 2020. A crane is a lifting or lowering machine equipped with a hoist rope, wire ropes or chains, and sheaves. It is mainly used for lifting heavy objects and transporting them to other places. Industrial counterweights for cranes are widely used in the construction industry. Cranes are of various types, such as tower cranes, mobile cranes, overhead cranes, and loader cranes. Depending on the location of counterweights in cranes, they can be categorized as swinging type or fixed type.

The construction in industry is expected to dominate the industrial counterweights market, by end -user, during the forecast period.

The construction industry accounted for the largest share of the industrial counterweights market, by end-user industry, in 2020. Construction equipment are being enhanced to manage complex tasks and sustain in critical environments. With rising construction activities across the world and increasing budgets pertaining to construction, the demand for different types of cranes, especially tower cranes for the construction of tall buildings, will increase in emerging countries such as China, India, Brazil, and Middle Eastern countries.

Asia Pacific is expected to lead the industrial counterweights market

In this report, the industrial counterweights market has been analyzed with respect to 5 regions, namely, Asia Pacific, North America, Europe, South America, and the Middle East & Africa. Asia Pacific is expected to lead the industrial counterweights market, by region, during the forecast period. Asia Pacific consists of developing countries such as China and Japan. The growing industrial sectors in these countries is expected to be the main driver. Also, the growth of the construction and automotive sectors in China, India, Australia and South Korea has played a significant role in the growth of the industrial counterweights market in Asia Pacific. Nearly all the countries in the region are augmenting their construction capacity. China and Japan are investing heavily on their country’s infrastructural development. This has led to a rise in demand of industrial counterweights systems from construction sector, which is expected to drive the growth of the Asia Pacific industrial counterweights market.

To enable an in-depth understanding of the competitive landscape, the report includes the profiles of some of the top players in the industrial counterweights market.

The key players include FMGC, Farinia Group (France), Sic LAZARO (US), Crescent Foundry (India), Gallizo (Spain), Mars Metal (Canada). The leading players are adopting various strategies to increase their share in the industrial counterweights market.

About MarketsandMarkets™

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth niche opportunities/threats which will impact 70% to 80% of worldwide companies’ revenues. Currently servicing 7500 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Our 850 fulltime analyst and SMEs at MarketsandMarkets™ are tracking global high growth markets following the "Growth Engagement Model – GEM". The GEM aims at proactive collaboration with the clients to identify new opportunities, identify most important customers, write "Attack, avoid and defend" strategies, identify sources of incremental revenues for both the company and its competitors. MarketsandMarkets™ now coming up with 1,500 MicroQuadrants (Positioning top players across leaders, emerging companies, innovators, strategic players) annually in high growth emerging segments. MarketsandMarkets™ is determined to benefit more than 10,000 companies this year for their revenue planning and help them take their innovations/disruptions early to the market by providing them research ahead of the curve.

MarketsandMarkets’s flagship competitive intelligence and market research platform, "Knowledgestore" connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : 1-888-600-6441 newsletter@marketsandmarkets.com