Energy and Power Market Research Reports & Consulting - The report captures in-depth strategic insights on crucial topics which helps our clients make their informed decisions

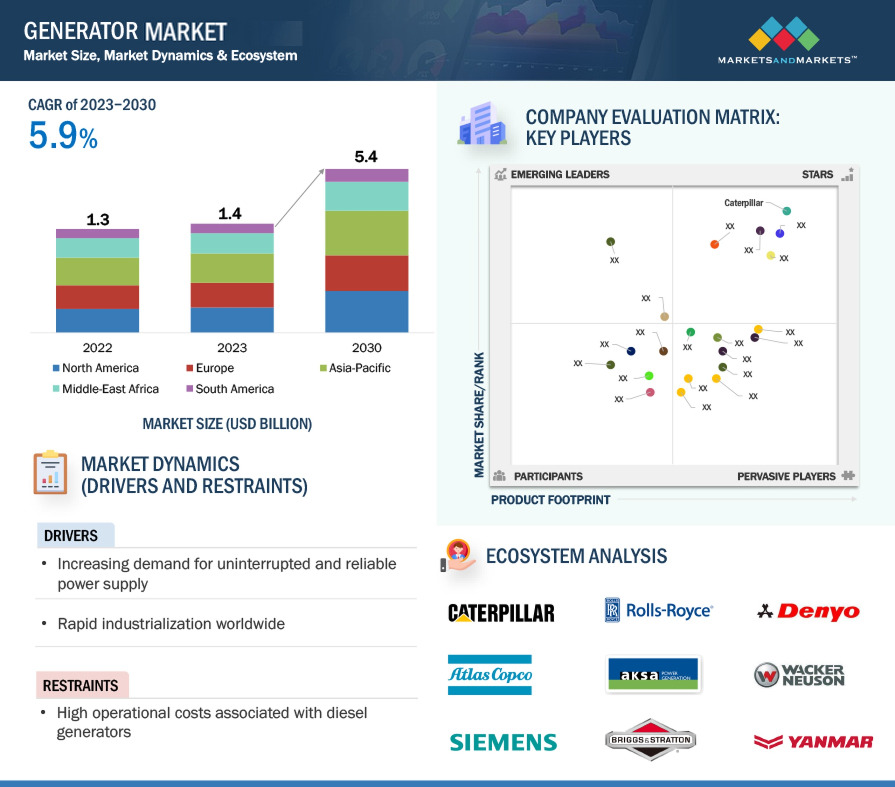

According to a research report "Generator Market by Fuel Type (Diesel, Gas, LPG, biofuels), Power Rating (Up to 50 kW, 51–280 kW, 281-500 kW, 501-2000 kW, 2001-3500 kW, Above 3500 kW), Application, End-User Industry, Design, Sales Channel, Region - Global Forecast to 2030" published by MarketsandMarkets, the global generator market is projected to reach USD 34.5 billion by 2030 from an estimated USD 23.1 billion in 2023, at a CAGR of 5.9% during the forecast period.

Generators are devices that convert mechanical energy into electrical energy. They consist of an engine or motor that drives a rotor, which creates a rotating magnetic field. This field induces an electric current in the stator windings, producing usable electrical power for various applications, such as providing backup power during outages.

Commercial, by end-user industry, is expected be the largest market during the forecast period.

Based on end-user industry, the generator market has been split into commercial, residential, industrial. Commercial end users include IT & telecom, healthcare, data centers, and others. Other commercial end users include hotels, shopping complexes, malls, and public infrastructure. Blackouts in commercial premises can lead to huge financial losses and safety issues. Also, it is challenging for IT and other commercial end users to conduct smooth operations during peak hours and in remote locations using power grids. Generators indirectly protect business interests and revenues by running operations smoothly and avoiding losses. These benefits is driving the market for commercial segment.

The direct segment, by sales channel is expected to be the fastest segment during the forecast period

Companies offering generators directly to end users or EPC contractors in different regions are considered under the direct sales segment. This mode eliminates the intermediaries involved in product distribution and helps avoid expensive overheads and reduce advertising costs. This advantage is driving the segment to the fastest market.

North America is expected to be the second largest region in the Generator market

North America is expected to be the second largest generator market during the forecast period. Extensive LNG projects and growing investments in manufacturing and chemicals & petrochemicals industries are the primary drivers of the market in this region. Due to its large-scale industrial sector and the world’s highest per capita energy consumption, the region has tremendous energy requirements. This is creating demand for the generators in the market.

Some of the major players in the generator market are Caterpillar Inc. (US), Cummins Inc. (US), Rolls-Royce Holdings plc (UK), Generac Holdings Inc. (US), Mitsubishi Heavy Industries, Ltd. (Japan). The major strategies adopted by these players include acquisitions, sales contracts, product launches, partnerships, and expansions.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

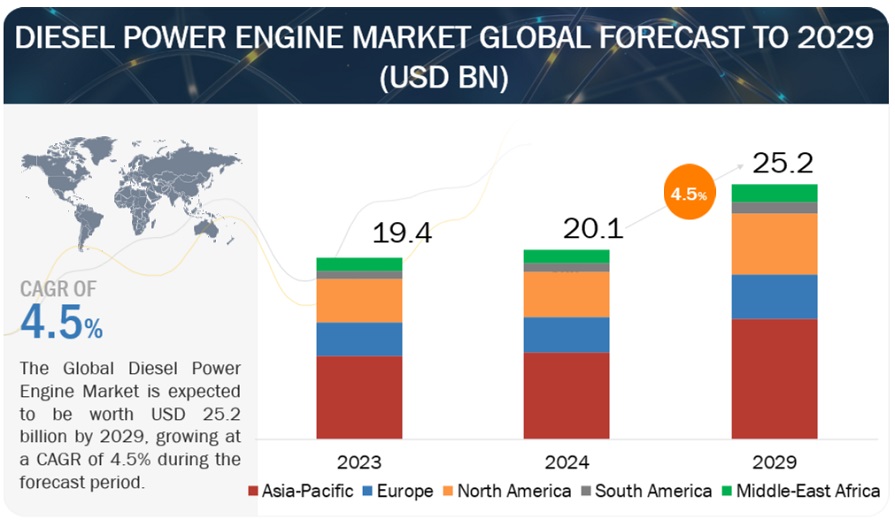

According to a research report "Diesel Power Engine Market by Operation (Standby, Prime, Peak Shaving), Power Rating (Below 0.5 MW, 0.5–1 MW, 1–2 MW, 2–5 MW, and Above 5 MW), End User (Power Utilities, Industrial, Commercial, and Residential), Speed, & Region - Global Forecast to 2029" published by MarketsandMarkets, the market size for diesel power engine is projected to reach approximately USD 25.2 billion by the year 2029, as compared to the estimated value of USD 20.1 billion in 2024, at a Compound Annual Growth Rate (CAGR) of 4.5% over the forecast period. The global diesel power engine market is driven by a confluence of factors that influence demand and shape its future trajectory. Rapid economic growth in regions like Asia Pacific, Africa, and South America fuels the need for reliable power sources. Diesel engines play a crucial role, particularly in areas with limited grid infrastructure or frequent outages. They provide primary or backup power for businesses, industries, and communities, enabling uninterrupted operations and fostering economic development. As economies expand, industrial activity and urbanization accelerate. These sectors heavily rely on diesel engines for power generation, both for primary use and backup during grid disruptions. Reliable power ensures smooth operation of factories, construction sites, and commercial facilities. Governments worldwide are implementing stricter emission regulations to combat air pollution. This drives advancements in cleaner burning diesel engine technologies.

Manufacturers are developing engines with lower NOx and particulate matter emissions, ensuring compliance with regulations and reducing environmental impact. The market is exploring alternative fuel options like biodiesel or biofuels derived from renewable sources. This allows diesel engines to contribute to a more sustainable energy mix while maintaining their reliability and power output. The integration of renewable energy sources like solar and wind power into the grid is increasing. However, these sources are intermittent. Diesel engines can act as a balancing mechanism, providing backup power during periods of low renewable energy generation and stabilizing grid frequency. Combining diesel engines with renewable energy sources in hybrid power plants offers a promising solution. Renewable energy provides primary power when available, while diesel engines take over during peak demand periods or outages, ensuring a reliable and efficient power supply. These drivers, along with factors like fluctuating fuel prices and advancements in alternative energy technologies, will continue to shape the global diesel power engine market. Manufacturers that prioritize cleaner technologies, efficient engines, and adaptability to changing energy landscapes will be well-positioned to capitalize on future growth opportunities.

Commercial segment, by End User, to hold the third-largest market in diesel power engine market.

The commercial segment secures the third-largest market share within the diesel power engine market by end user segment, driven by several key factors. Modern businesses rely heavily on electricity for various functions like lighting, communication systems, data processing, and security. Outages can cause significant disruptions and revenue losses. The commercial segment utilizes diesel generators as a reliable backup power source to ensure business continuity during grid disruptions. Hospitals, data centers, airports, and other critical infrastructure require uninterrupted power supply. Commercial-grade diesel generators provide a reliable backup solution for these facilities, protecting essential services from outages. Businesses located in areas with unreliable grid infrastructure or those seeking greater energy independence might invest in microgrids powered by diesel generators. These microgrids provide a reliable and localized power source, offering greater control and potentially lower energy costs. The construction industry relies on temporary power solutions like diesel generators to power equipment and facilities at remote job sites. Similarly, businesses with off-grid operations, like telecom towers or mining sites, utilize diesel engines for primary power generation. Hotels, shopping malls, and other commercial establishments utilize diesel generators to ensure continued operations during power outages. Maintaining comfortable temperatures, lighting, and electronic systems is crucial for customer satisfaction and security. Warehouses and cold storage facilities require consistent temperature control to ensure product quality. Diesel generators provide backup power to maintain refrigeration systems and prevent spoilage during outages. While renewable energy solutions like solar panels are gaining traction, they often require a higher initial investment. For businesses with tight budgets, diesel generators offer a more cost-effective option for backup or temporary power needs. Diesel generators can be deployed quickly and scaled to meet specific power requirements. This flexibility is crucial for businesses requiring temporary power or those with fluctuating power demands.

2-5 MW segment, by Power Rating, to be the third-largest market segment.

The 2-5 MW segment by power rating holds the third-largest market share in the global diesel power engine market due to its ideal capacity to bridge the gap between smaller-scale applications and large-scale industrial needs. This segment is highly valued for its versatility, efficiency, and ability to meet a diverse range of power requirements across various sectors. One of the primary reasons for the prominence of the 2-5 MW power rating segment is its suitability for medium to large-scale power generation applications. These diesel engines are commonly used in industries such as manufacturing, commercial facilities, hospitals, and data centers, where there is a need for reliable and continuous power supply. The 2-5 MW engines provide sufficient power to support critical operations and ensure operational continuity during power outages or in areas with unreliable grid power. Their ability to deliver a stable and robust power output makes them an essential component for prime and standby power generation solutions. In addition to their application in power generation, the 2-5 MW diesel engines are extensively utilized in the oil and gas industry. In this sector, they are often deployed for drilling operations, offshore platforms, and other energy-intensive processes that require dependable power sources. The harsh and remote environments associated with oil and gas exploration and production necessitate power solutions that are both robust and efficient. Diesel engines in the 2-5 MW range are well-suited for these conditions, providing the necessary power while maintaining operational reliability.

The 2-5 MW segment is favored for its balance between cost and performance. These engines offer a cost-effective solution for applications that require more power than smaller engines can provide but do not necessitate the higher capital and operational expenditures associated with larger engines. This cost-effectiveness extends to fuel consumption as well, where engines in this power rating range are designed to optimize fuel efficiency, resulting in lower operating costs over time. This makes them an attractive option for businesses looking to manage their energy expenses without compromising on power availability. The construction and infrastructure sectors also drive the demand for 2-5 MW diesel engines. Construction sites often require mobile and reliable power sources to operate heavy machinery, lighting, and other essential equipment. Diesel generators in this power rating are portable enough to be transported to different sites while powerful enough to meet the high energy demands of large construction projects. Their ability to provide consistent power in off-grid and remote locations makes them indispensable for large-scale construction and infrastructure development. Additionally, advancements in diesel engine technology have bolstered the market position of the 2-5 MW segment. Manufacturers are continually innovating to enhance the performance, emissions control, and efficiency of these engines. Modern engines in this power rating range feature advanced fuel injection systems, improved combustion processes, and sophisticated control mechanisms that reduce emissions and comply with stringent environmental regulations. These technological improvements not only increase the attractiveness of 2-5 MW diesel engines but also ensure their competitiveness in a market that increasingly values sustainability and environmental responsibility.

Middle East & Africa to emerge as the third-largest diesel power engine market.

The Middle East & Africa region holds the fourth-largest market share in the global diesel power engine market due to a combination of factors that drive demand across various sectors, including energy, construction, mining, and manufacturing. Firstly, the Middle East's robust oil and gas industry is a significant contributor to the demand for diesel power engines. Countries like Saudi Arabia, the UAE, and Kuwait rely heavily on diesel engines to power drilling rigs, pump stations, and other critical infrastructure in remote locations where access to the grid is limited. The need for reliable and continuous power in these operations ensures a steady demand for diesel power engines, particularly in mid-to-large power ratings. In Africa, the widespread lack of reliable grid infrastructure drives the demand for diesel power engines as primary and backup power sources. Many African countries face frequent power outages and have limited access to consistent electricity supply. Diesel generators provide an essential solution for businesses, hospitals, and residential areas to ensure uninterrupted power. This is particularly crucial for sectors like healthcare and telecommunications, where power reliability is paramount. The construction boom in the Middle East, driven by massive infrastructure projects and urban development initiatives, also fuels the demand for diesel power engines. Major cities like Dubai and Riyadh are continuously expanding, requiring substantial power for construction machinery, site lighting, and other temporary power needs. Diesel engines are favored in these scenarios due to their portability, robustness, and ability to deliver high power output in varying environmental conditions.

Mining activities across Africa, particularly in countries such as South Africa, Nigeria, and Ghana, further boost the market for diesel power engines. The mining industry operates in remote areas with little to no access to grid power, making diesel engines indispensable for powering mining equipment, ventilation systems, and processing plants. The reliability and durability of diesel engines make them the preferred choice in the harsh operating conditions typical of mining sites. Moreover, the region's ongoing industrialization and urbanization trends are key drivers of diesel engine demand. As Middle Eastern and African countries continue to develop their industrial base, the need for reliable power solutions increases. Diesel engines play a critical role in supporting manufacturing operations, logistics, and agricultural activities by providing a dependable source of power, especially in areas where the electrical grid is underdeveloped or unstable. Government initiatives aimed at improving energy access and infrastructure also play a role in sustaining demand for diesel power engines. Many countries in the region are investing in expanding their energy infrastructure, including the deployment of diesel generators as a stopgap solution while longer-term projects like renewable energy installations are developed. Lastly, the adaptability of diesel engines to operate in diverse climatic conditions found across the Middle East and Africa, from the arid deserts of the Middle East to the tropical regions of Sub-Saharan Africa, underscores their utility and widespread adoption. Manufacturers in the region have also been focusing on developing engines that comply with stringent emission standards, enhancing their market appeal by addressing environmental concerns.

Key players in the global diesel power engine market include Caterpillar (US), Cummins Inc. (US), WEICHAI POWER CO.,LTD (China), MAN (Germany), Rolls-Royce plc (UK), MITSUBISHI HEAVY INDUSTRIES, LTD. (Japan), HD HYUNDAI INFRACORE (South Korea), DAIHATSU DIESEL MFG. CO., LTD. (Japan), YANMAR HOLDINGS CO., LTD. (Japan), KUBOTA Corporation (Japan), Kohler Energy (US), AB Volvo Penta (Sweden), DEUTZ AG (Germany), Mahindra&Mahindra Ltd. (India), IHI Power Systems Co.,Ltd (Japan), Guangzhou diesel engine factory Limited (China), and Wabtec Corporation (US).

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

The global hydrogen energy storage market is projected to reach USD 196.8 billion by 2028 from an estimated USD 11.4 billion in 2023, at a CAGR of 76.8% during the forecast period. The growing emphasis on environmental sustainability, rising adoption of fuel cell vehicles, intermittent renewable energy integration accelerates the growth of the hydrogen energy storage market.

Key Market Players

Linde plc (Ireland), ENGIE (France), Plug Power Inc. (US), Fuelcell Energy, Inc. (US), Iwatani Corporation (Japan), Hydro X (Israel), LAVO System (Australia), HYDROGEN IN MOTION (Canada), Mahytec (France), GKN Hydrogen (Italy), HPS Home Power Solutions AG (Germany), HDF ENERGY (France), Energy Vault, Inc. (Switzerland), BALU FORGE INDUSTRIES LIMITED (India), storelectric LTD (UK), H2GO Power (UK), Powertech Labs Inc. (Canada), Beijing SinoHy Energy Co., Ltd. (China), Hydrogenious LOHC Technologies (Germany), Ergenics Corp. (US), Power to hydrogen (US)

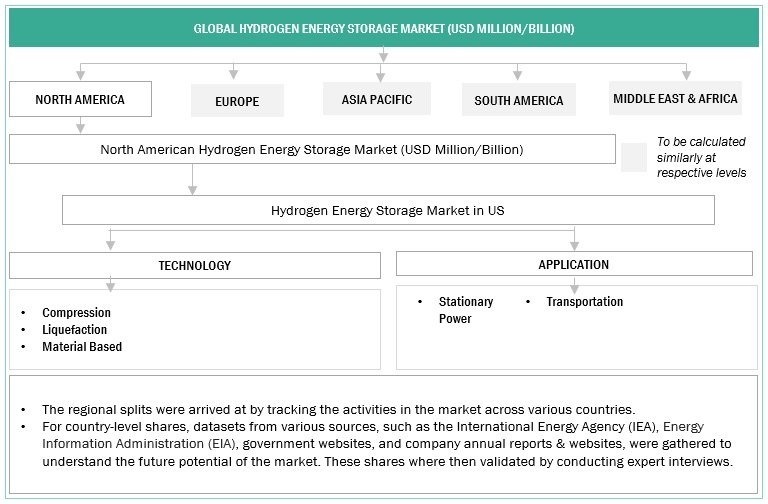

This report segments the hydrogen energy storage market based on application into three categories: electric utilities, industrial, and commercial. Electric Utilities is expected to hold the largest market share in the hydrogen energy storage market during the forecast period. The demand for hydrogen energy storage is increasing in electric utilities applications due to integration of renewable energy and grid stability and reliability. Hydrogen energy storage can provide backup power during grid outages and can be used to balance supply and demand on the grid by storing excess electricity during times of low demand are the factors that are expected to drive the growth of the electric utilities segment during the forecast period.

Based on the Storage form, the hydrogen energy storage market is segmented into solid, liquid and gas. The gas segment is expected to dominate the market during the forecast period as gas form is more efficient and can easily be transported. Hydrogen energy storage as gas results in fewer energy losses during the storage process and there is already established infrastructure for transporting and distributing gaseous hydrogen energy.

Based on the technology, the hydrogen energy storage market is segmented into compression, liquefaction and material-based. The compression segment is expected to be the fastest growing market during the forecast period owing to the low energy losses compared to other methods and high energy density per unit volume. Compression technology is cost effective as compared to other storage technologies, which is expected to drive the growth of the medium voltage segment in the forecasted period.

This report segments the hydrogen energy storage market based on application into stationary power and transportation. During the forecast period, the stationary power segment holds the largest market share due to its higher efficiency, safety, and ability to provide a steady energy supply for grid integration and industrial processes. The Stationary systems are well-suited for critical facilities, sustainability goals, and avoiding transportation challenges.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

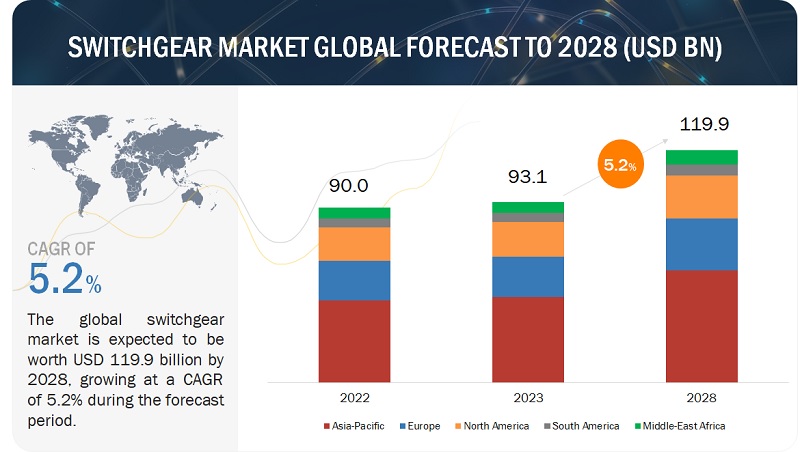

According to a research report "Switchgear Market by Insulation (Gas-insulated, Air-insulated), Installation (Indoor, Outdoor), Current (AC, DC), Voltage (Low (up to 1 kV), Medium (2-36 kV), High (Above 36 kV), End User and Region - Global Forecast to 2028" published by MarketsandMarkets, the market size for switchgear is projected to reach approximately USD 119.9 billion by the year 2028, as compared to the estimated value of USD 93.1 billion in 2023, at a Compound Annual Growth Rate (CAGR) of 5.2% over the forecast period.

The switchgear market is poised for substantial growth during this period, primarily due to the development of power distribution infrastructure in response to the growing demand for electricity. Furthermore, the expansion of renewable energy-based capacity and increased investments in industrial production are likely to drive the demand for switchgear.

High voltage segment, by voltage, to occupy majority of switchgear market share.

During the forecast period, the high voltage segment, categorized by voltage, is expected to secure a dominant market share. High-voltage switchgears, operating above 36 kV, are crucial in transmission, heavy industries, mining, railways, and commercial infrastructures. The main component, a high-voltage circuit breaker, is integral. Gas-insulated switchgears are prevalent in these applications. Typically placed outdoors due to space requirements, they consist of circuit breakers, isolators, transformers, and bus bars. Faulty tripping is rare, and these switchgears often remain ON for extended periods. They play a vital role in renewable power transmission and medium-voltage substations. As electrification and renewable integration rise, the demand for high-voltage switchgear, especially automated and smart ones for smart grids, is expected to surge in the forecasted period.

Commercial & residential segment, by end user, to be third-largest and third-fastest market.

Urbanization, particularly in regions like Asia Pacific, South America, and Africa, is driving a surge in commercial and residential constructions. As urban centers grow due to economic opportunities, the need for housing and commercial buildings escalates. Switchgear plays a vital role in supplying, safeguarding, and regulating power for various equipment in these constructions. Additionally, contemporary switchgears are engineered to handle earth leakage current faults, enhancing their safety features. Consequently, the demand for switchgear in commercial and residential applications is anticipated to rise significantly in the coming years.

North America to emerge as the third-largest switchgear market.

During the forecast period, North America is anticipated to hold the third-largest market share in the global switchgear market. Encompassing the US, Canada, and Mexico, the region boasts extensive trade ties and significant foreign investments, with the US and Canada jointly contributing around 93.8% to North America's switchgear market. With a combined population of nearly 530 million and an economy representing over one-quarter of the world's GDP, the region faces substantial power demands, leading to increased investments in fortifying and modernizing its transmission and distribution utilities. Notably, energy consumption per capita in North America saw a 4% rise, according to the BP Statistical Review of World Energy 2022.

The region is undergoing a transformative phase in its utilities sector, marked by a shift towards digital operational strategies focusing on decentralization, digitization, and decarbonization of power systems. Aging power infrastructures, constituting nearly 72% of the US power infrastructure beyond 25 years of service, pose a blackout risk, prompting active government initiatives to upgrade and replace these structures for enhanced grid reliability.

Key players in the global switchgear market include ABB (Switzerland), General Electric (US), Siemens (Germany), Schneider Electric (France), and Eaton (Ireland).

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

According to a new market research report, the residential energy storage market is anticipated to reach a value of USD 898 million in 2023 and is expected to expand to USD 2,081 million by 2028, exhibiting a CAGR of 18.3%. The market growth is propelled by the decreasing costs of lithium-ion batteries and significant government investments, which contribute to the market's positive trajectory.

By technology, the residential energy storage market is divided into two segments: lithium-ion and lead-acid. The segment expected to witness the highest growth rate during the forecast period is lithium-ion. This growth can be attributed to factors such as the cost effectiveness of lithium-ion technology and the increasing number of manufacturing sites established by various companies, including Tesla (US) and BYD Company Ltd (China).

By operation type, the residential energy storage market is segmented into standalone systems and solar and storage systems. Among these, the solar and storage systems segment holds the largest market share and is projected to grow at the highest rate during the forecast period. This growth can be attributed to the increased installations of solar PV systems, which drive the demand for combined solar and storage solutions.

By ownership type, the residential energy storage market is segmented into customer-owned, utility-owned, and third-party-owned. Among these segments, the utility-owned segment is expected to witness the second-highest growth rate in the forecast period. This growth can be attributed to the expiration of feed-in-tariff contracts, which incentivize utilities to invest in and own residential energy storage systems.

The report is divided into sections for the 3-6 kw, 6-10 kw, and 10-20 kW power ratings in the residential energy storage market. Due to the demand for emergency backup power during natural disasters and prolonged power outages, 3-6 kW is anticipated to grow at the second highest rate during the forecast period.

According to connectivity, the report divides the residential energy storage market into on-grid and off-grid categories. Due to lower upfront costs and frequent power outages, the on-grid segment, which accounted for the largest market share, was anticipated to experience the fastest growth.

During the forecast period, Asia-Pacific is anticipated to have the residential energy storage market with the fastest growth. China, India, Japan, Australia, South Korea, and the Rest of Asia Pacific, which includes the Philippines, Indonesia, and Thailand, are the countries into which the region has been divided. The dominance of the Asia Pacific region is due to the rapidly declining cost of batteries and growing demands for improved grid infrastructure and dependability.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

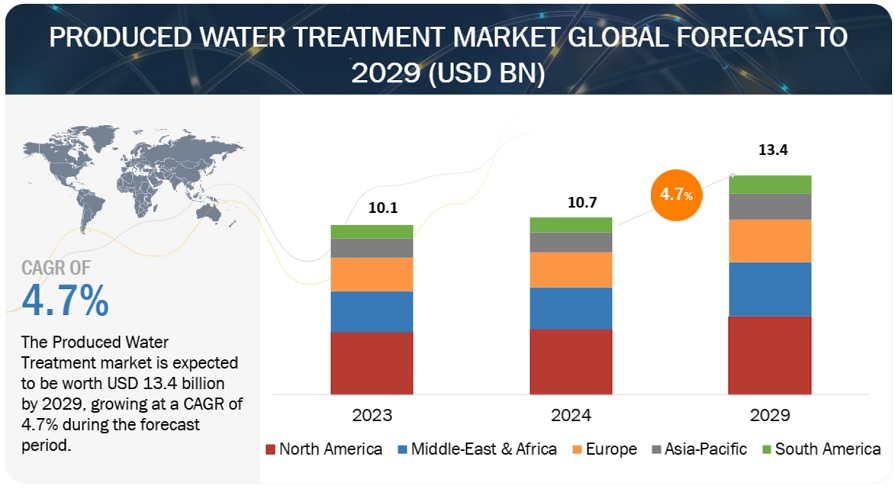

According to a research report "Produced Water Treatment Market by Application (Onshore, Offshore), Source (Conventional, Unconventional), Treatment (Primary treatment, Secondary treatment, Tertiary treatment) and Region - Global Forecast to 2029" published by MarketsandMarkets, the produced water treatment market is forecast to reach USD 13.4 billion by 2029 from an estimated USD 10.7 billion in 2024, at a CAGR of 4.7% during the forecast period (2024-2029).

Produced water, which is a byproduct of oil and gas exploration process, requires active treatment to meet environmental regulations and helps in reuse or safe disposal. This produced water is a mixture of injected water, Natural formation water, and any other chemicals used in the exploration and drilling process.

By Source, the Conventional segment is estimated to be the largest segment during the forecast period.

Based on source, the produced water treatment market has been split into Conventional and Unconventional. The Conventional segment in the produced water treatment market is anticipated to be the largest because it is experiencing rapid growth due to the increasing exploration and production activities. The conventional segment for produced water treatment is growing due to the increase in established oil and gas fields that require constant maintenance to remain effective.

By Application, Onshore segment is expected to remain largest during the forecast period.

Based on Application, the produced water treatment market has been split into Onshore and Offshore. The Onshore segment in the produced water treatment market is anticipated to be the largest because the onshore drilling operations are generally less expensive compared to offshore projects. The onshore segment experienced considerable growth due to the cost advantages, technological advancements, better infrastructure, and increased exploration and production activities.

By treatment type, Tertiary treatment is expected to grow fastest during the forecast period.

This report segments the produced water treatment market based on various treatment methods: Primary treatment, secondary treatment, and tertiary treatment. Tertiary treatment is expected to be the fastest growing segment during the forecast period due to the usage of advanced methods such as reverse osmosis and advanced oxidation. These processes provide high levels of impurities removal to make the treated water suitable for reuse as portable water as well as in industrial applications.

Middle East & Africa is expected to be the Second fastest region in the produced water treatment market.

Middle East & Africa is expected to be the second fastest growing region after Asia-Pacific in the produced water treatment market during the forecast period. The region's increasing focus on produced water treatment is due to the Geopolitical stability, Abundant oil and gas reserves, and expanding Exploration & Production activities. The MEA region is home to some of the world's largest oil and gas reserves, particularly in countries like Saudi Arabia, Iran, Iraq, Kuwait, and the United Arab Emirates. The MEA region has significant offshore oil and gas reserves, particularly in the Persian Gulf, Red Sea, and offshore West Africa.

Some of the major players in the produced water treatment market are SLB (US), Baker Hughes Company (US), Siemens Energy (Germany), Veolia Environnement SA (France), TechnipFMC (UK). The major strategies adopted by these players include sales contracts, product launches, investments, collaborations, partnerships, and expansions.

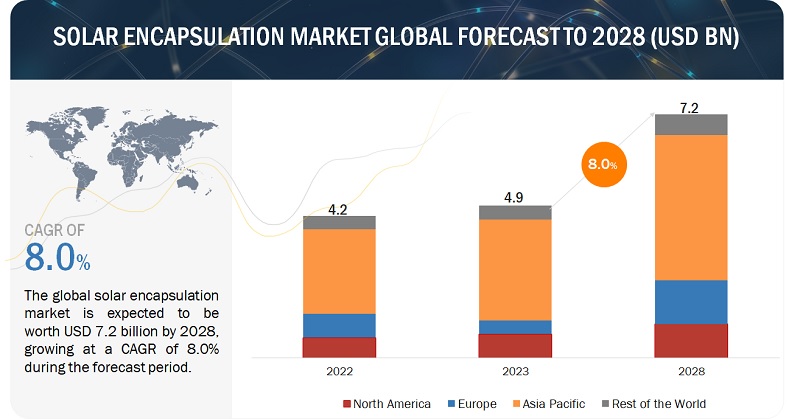

According to a latest research, the solar encapsulation market is projected to reach USD 7.2 billion by 2028 from an estimated USD 4.9 billion in 2023, at a CAGR of 8.0% during the forecast period. Solar encapsulation is the technique of sealing and protecting solar cells with a layer of materials, most often polymers such as ethylene-vinyl acetate (EVA) or polyolefins (POE). This protective layer is important to the longevity, durability, and efficiency of solar panels. Encapsulants of excellent grade are highly transparent, allowing maximum sunlight to enter the cells and improve their power generation. They can also improve light trapping within the cell and reduce optical losses. Rising growth in the demand for solar energy along with increasing adoption of photovoltaics technology solutions are the factors expected to drive the demand for the solar encapsulation market.

Key Market Players

Some of the major players in the solar encapsulation market are Mitsui Chemicals, Inc. (Japan), Elkem ASA (Norway), Dow (US), 3M (US), and DuPont (US). The major strategies these players adopt include new product launches, contracts, agreements, partnerships, and investments & expansions.

The Thermoplastic polyurethane (TPU) segment, by materials, is expected to grow at the highest CAGR during the forecast period.

Based on materials, the solar encapsulation market has been segmented into Ethylene-vinyl Acetate (EVA), Polyvinyl Butyral (PVB), Polydimethylsiloxane (PDMS), Ionomer, Polyolefin, Thermoplastic Polyurethane (TPU). The Thermoplastic polyurethane (TPU) segment is expected to be the fastest growing segment during the forecast period. TPU boasts excellent mechanical properties like abrasion resistance, high elasticity, and good low-temperature performance. Compared to EVA, TPU shows less yellowing and degradation under UV exposure, potentially leading to a longer lifespan for the solar panel. Currently, TPU is more expensive than EVA, making it less commercially viable for large-scale solar module production.

The Crystalline Silicon, by technology, is expected to be the largest segment during the forecast period.

This report segments the solar encapsulation market based on technology into crystalline silicon and thin-film solar technology. The crystalline silicon technology segment is further sub-segmented into mono crystalline and polycrystalline silicon solar technology. The thin-film solar technology segment is sub-segmented into Cadmium telluride (CdTe), Copper-Indium-gallanium-selenide (CIGS) and Amorphous Silicone. The crystalline silicon of the solar encapsulation market based on technology is expected to be the largest segment during the forecast period. Crystalline silicon has a reasonably high energy conversion efficiency, reaching up to 25% in laboratory settings and ranging from 18% to 22% in commercially available modules. This means that it produces more electricity per unit area of sunlight than many other technologies. Ongoing R&D efforts continue to push the efficiency limitations of crystalline silicon, making it a viable option even against newer technologies.

This research report categorizes the solar encapsulation market based on materials, technology, application, and region.

On the basis of materials:

Ethylene Vinyl Acetate (EVA)

Thermoplastic Polyurethane (TPU)

Polyvinyl Butyral (PVB)

Polydimethylsiloxane (PDMS)

Ionomer

Polyolefin

On the basis of technology:

Crystalline Silicon Solar

Thin-Film Solar

On the basis of application:

Ground-mounted

Building-integrated photovoltaic

Floating photovoltaic

Others (Automotive, Construction, and Electronics)

Based on region:

Europe

Asia Pacific

North America

Rest of the World

The Ground-mounted, by application, is expected to be the largest segment during the forecast period.

This report segments the solar encapsulation market based on application into four segments: Ground-mounted, Building-integrated photovoltaics, Floating Photovoltaics and others. The Ground-mounted segment is expected to be the largest segment during the forecast year. The ground-mounted PV systems market is predicted to increase significantly during the forecast period, owing to an increasing number of utility-scale projects worldwide. According to the Solar Energy Industries Association (SEIA), solar installation has increased by over 33% globally, with ground-mounted systems accounting for the largest share. Additionally, Ground-mounted ones can be adjusted according to the season or support a solar tracker that follows the sun's path throughout the day. A ground-mounted system with a tracker can be 10% to 45% more efficient than a rooftop solar system.

Asia Pacific is expected to be the largest region in the solar encapsulation market.

Asia Pacific is expected to be the largest solar encapsulation market during the forecast period. Governments in Japan, South Korea, and China are actively actively promoting the advancement and integration of solar technology as a critical component of their strategies to reduce carbon emissions and encourage the adoption of sustainable energy solutions. In particular, Japan and South Korea have made significant investments in solar technology, directing their efforts toward diverse applications such as building-integrated photovoltaics.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

According to a research report "Inverter Market by Type (Solar Inverters, Vehicle Inverter), Output Power Rating (Upto 10 kW, 10-50 kW, 51-100 kW, above 100 kW), End User (PV Plants, Residential, Automotive), Connection, Voltage, Sales Channel & Region - Global Forecast to 2028" published by MarketsandMarkets, the Inverter market is projected to reach USD 39.6 billion by 2028 from USD 18.9 billion in 2023, at a CAGR of 16.0% during the forecast period.

The simplicity of installation for both string and micro inverters is the main factor propelling the global market's expansion. The industry has grown as a result of increased investment in the development of renewable power infrastructure and the rise in demand for electricity from diverse uses. It is projected that the renewable energy and rural electrification sectors would see a sharp increase in investment, which will present profitable prospects for industry participants. The business is growing globally as a result of the increased use of big-sized string inverters in the utility system and other commercial and industrial sectors. These inverters make it easier to install huge solar systems since they can link many solar panels.

Above 500 V, by output voltage, is expected to be the second fastest growing segment during the forecast period.

Based on output voltage, the Inverter market has been split into 100-300 V, 300-500 V, and above 500. The above 500 V is expanding mostly as a result of its use in utility-scale renewable energy projects and large-scale industrial applications. For the purpose of converting and controlling the significant power outputs of wind and solar farms, these high-voltage inverters are essential. The global adoption of large-scale renewable energy programmes and high-capacity industrial operations is driving up demand for inverters that operate above 500V. The expansion of this market is a result of the worldwide trend towards large-scale clean energy production and the requirement for strong, high-capacity inverters to enable these powerful and far-reaching applications.

The above 100 kw segment, by output power rating segment, is expected to be the fastest segment during the forecast period.

This report segments the Inverter market based on output power rating into below 10 kw, 10-50 kw, 50-100 kw, and above 100 kw . The above 100 kW output power rating segment in the inverter market is growing due to the escalating demand for high-capacity inverters in large-scale industrial and commercial applications. Industries and enterprises increasingly seek powerful inverters to handle substantial energy loads efficiently. This trend aligns with the expanding adoption of renewable energy solutions, where solar and wind projects demand inverters with capacities exceeding 100 kW to accommodate higher power outputs. As industries prioritize sustainable practices, the growth in this segment reflects the need for robust, high-power inverters to support large-scale clean energy initiatives.

North America is expected to be the second largest region in the Inverter market

Considering many of factors, North America is the second-largest region in the inverter industry. An expanding market for renewable energy, especially in the US and Canada, drives up demand for inverters for solar and wind power systems. The market for inverters is growing as a result of supportive government policies and incentives that encourage the use of renewable energy. Increased inverter deployment is also a result of the region's concentration on grid upgrading and the electrification of numerous sectors. Furthermore, the need for inverters is being driven by a shift towards clean energy and a greater awareness of sustainability, which is why North America is a major player in the worldwide inverter market.

Some of the major players in the Inverter market are Huawei Technologies Co., Ltd. (China), SUNGROW (China), SMA Solar Technology AG (Germany), Power Electronics S.L. (Spain), and Fimer Group (Italy).The major strategies adopted by these players include sales contracts and agreements.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

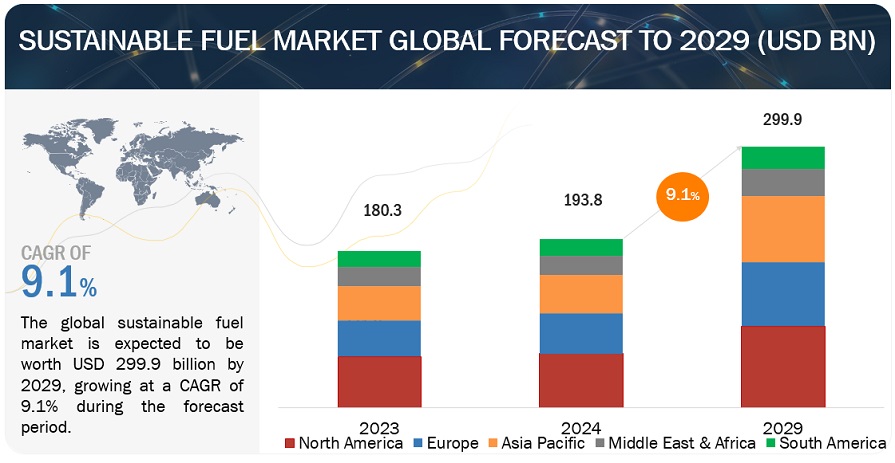

According to a research report "Sustainable Fuel Market by Type (Renewable Fuels, Low Carbon Fossil Fuels), Fuel Type (Biofuels, E-Fuels, Hydrogen, Biomethane, CNG), End User (Road transportation, Marine, Aviation), State (Liquid, Gas) and Region - Global Forecast to 2029" published by MarketsandMarkets, the global Sustainable Fuel Market is projected to reach USD 299.9 billion by 2029 from an estimated USD 193.8 billion in 2024, at a CAGR of 9.1% during the forecast period.

Globally, stronger environmental regulations and policies need a reduction in carbon emissions. Governments enforce this through carbon price, emissions trading networks, and transportation-specific regulations. These approaches promote the use of sustainable fuels in order to satisfy regulatory responsibilities. Furthermore, governments throughout the world are establishing blending regulations, which mandate a certain percentage of sustainable fuels to be combined with traditional fuels. These regulations drive the market for sustainable fuels by assuring a steady demand. Furthermore, individuals are increasingly selecting environmentally friendly products and services. This shift in customer behavior puts pressure on businesses to adopt sustainable practices, such as the use of renewable energy.

E-fuels, by Fuel type, are expected to be the fastest-growing segment during the forecast period.

Advances in e-fuel production technology, such as more effective electrolysis and carbon capture systems, reduce production costs and improve the viability of large-scale e-fuel production, making it more appealing to investors and customers. E-fuels may be generated domestically using renewable resources, lowering reliance on imported fossil fuels and improving national energy security. This characteristic is especially enticing to countries seeking greater energy independence. Many businesses are implementing environmental initiatives to minimize their carbon footprints. Using e-fuels allows these firms to satisfy their sustainability goals and improve their environmental image, which supports market growth. As manufacturing methods develop and scale up, the cost of e-fuels falls, making them more competitive with conventional fossil fuels. This cost reduction fosters broader use throughout various Sectors.

Low Carbon Fossil Fuels, by type, is expected to be the fastest-growing segment during the forecast period.

The expansion of low-carbon fossil fuels is driven by rising consumer and industrial demand for greener energy sources. This demand stems from environmental awareness and a need for sustainable energy alternatives. Aside from that, when economies of scale are attained and manufacturing techniques grow more efficient, the cost of low-carbon fossil fuels falls, allowing them to compete with traditional fossil fuels. Significant investment and finance from both the public and private sectors support research, development, and infrastructure for low-carbon fossil fuel initiatives, promoting market innovation and growth. Furthermore, supportive government policies, such as subsidies, tax breaks, and renewable energy requirements, promote investment in low-carbon fossil fuel projects and drive market expansion.

Asia Pacific is expected to be the fastest-growing region during the forecast period.

Governments in the Asia Pacific are enacting legislation and regulations to promote the use of sustainable aviation fuels (SAF). These policies include incentives, subsidies, and requirements to use SAF, all of which encourage market growth. Consumers and companies are becoming more conscious of traditional aviation fuels' environmental effects. This knowledge pushes stakeholders to seek sustainable alternatives, resulting in the rapid rise of the SAF industry. Collaboration among governments, industrial businesses, research institutes, and other stakeholders promotes innovation and market expansion. These ties facilitate information sharing, technology transfer, and collaborative efforts to address challenges to SAF implementation. Investments in infrastructure for sustainable fuel production, delivery, and consumption are important for Asia Pacific's SAF market expansion. Developing good infrastructure makes SAF more accessible and inexpensive, encouraging greater usage.

Some of the major players in the sustainable fuel market are ADM (US), Shell plc (UK), Siemens Energy AG (Germany), Saudi Arabian Oil Co. (Saudi Arabia), and Chevron Corporation (US) among others. The major strategies adopted by these players include new product launches, acquisitions, contracts, agreements, partnerships, joint ventures, collaborations, investments, and expansions.

About MarketsandMarkets™

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the ’GIVE Growth’ principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA : 1-888-600-6441 newsletter@marketsandmarkets.com

The global biofuel market is projected to reach USD 225.9 billion by 2028 from an estimated USD 167.4 billion in 2023, at a CAGR of 6.2% during the forecast period. The demand for biofuels is expected to grow in developing countries due to certain key factors such as increased investments in to encourage the use of biofuels and implementation of national policies that support higher biofuel blends.

Key Market Players

Prominent companies in this market include ADM (US), Chevron (US), Valero (US), Neste (Finland), and Cargill, Incorporated (US).

This report segments the biofuel market based on fuel type into four categories: ethanol, biodiesel, renewable diesel, and biojets. Ethanol is expected to hold the largest market share in the biofuel market during the forecast period. Ethanol is often higher in demand owing to its long history of manufacturing and use and its versatility as a gasoline additive. Ethanol is produced from a variety of agricultural feedstocks, including corn and sugarcane. The widespread availability of these feedstocks, as well as established supply chains, contribute to the adoption of ethanol.

Based on the generation, the biofuel market is segmented into first-generation, second-generation, and third-generation. The second-generation segment is expected to be the fastest-growing market during the forecast period. Second-generation biofuels are produced from non-food biomass feedstocks, such as agricultural waste, forestry residues, and energy crops. They offer a number of advantages over first-generation biofuels, which are produced from food crops. Second-generation biofuels are more sustainable, as they do not compete with food production for land and water resources. Increasing global awareness of climate change and the need to reduce greenhouse gas emissions has driven interest in advanced biofuels.

Based on end use, the biofuel market is segmented into transportation, aviation, and others. The aviation segment is expected to be the fastest-growing market during the forecast period owing to the large-scale decarbonization activities in the aviation sector in North America and Europe. The US, Norway, the Netherlands, and the UK are contributing significantly to the long-term sustainability plans by funding the biojet fuel infrastructure. In addition, the production of bio jet fuel is expected to scale up rapidly in the coming decade due to growing research and developments in technological pathways to commercialize the use of alternative jet fuels.

Europe is expected to be the fastest growing region in the biofuel market during the forecast period. The European region comprises major economies such as France, UK, Germany, and Poland. The biofuel market in Europe is primarily fueled by the three main types of biofuels, namely ethanol, biodiesel, and renewable diesel. Europe has actively fostered the use of biofuel through various policies and initiatives. The European Union (EU) has established targets for member states to enhance the utilization of renewable energy in transportation, including biofuels like biofuel. The Renewable Energy Directive (RED) and its subsequent revisions have played a pivotal role in shaping biofuel production and consumption in Europe.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Aashish Mehra MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: sales@marketsandmarkets.com