Energy and Power Market Research Reports & Consulting - The report captures in-depth strategic insights on crucial topics which helps our clients make their informed decisions

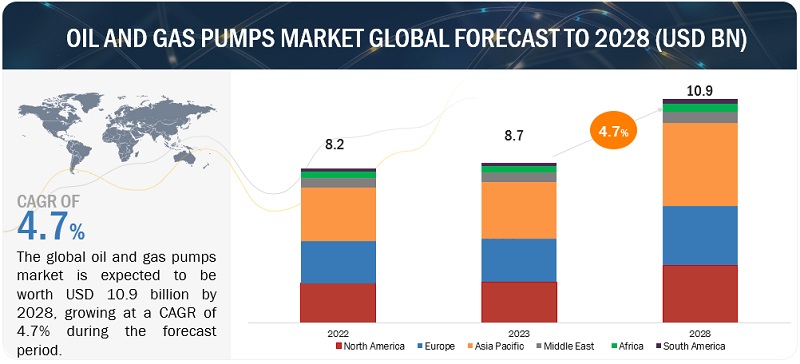

The global oil and gas pumps market is projected to reach USD 10.9 billion by 2028 from an estimated USD 8.7 billion in 2023, at a CAGR of 4.7% during the forecast period. Pumps have a critical role in the oil & gas industry. They are used in upstream drilling sites, crude oil pipelines, and LNG export terminals to transport fluids from one process or location to another. In the past, pumps were operated with fixed-speed electric motors. However, variable-speed electric motors have replaced them nowadays. Pumps that are driven by variable-speed drive systems reduce the likelihood of equipment failure by minimizing electrical and mechanical stresses, thereby reducing downtime. Oil and gas pumps are used in upstream, midstream, and downstream applications. The market for oil and gas pumps includes revenues generated by global companies from pump sales. The current study focuses on major pump types such as centrifugal pumps, positive displacement pumps, and cryogenic pumps. The increasing global demand for oil is likely to propel the demand for oil and gas pumps. Moreover, discoveries of new oilfield, will boost the demand for oil and gas pumps.

The centrifugal pumps, by pump type, is expected to grow at the highest CAGR during the forecast period.

Based on pump type, the oil and gas pumps market has been split into into Centrifugal Pumps, Positive Displacement Pumps and Cryogenic Pumps. Centrifugal pumps are expected to grow at the highest CAGR during the forecasted period. Centrifugal pumps are preferred for managing fluids with low viscosity and high flow rates, especially in environments free from air, vapor, or excessive solids. They hold significant importance in upstream operations, particularly in scenarios involving multiple phases. Different variants of these pumps are tailored to meet diverse application needs. Take, for instance, electrical submersible pumps that excel in efficiently separating water and oil. This functionality permits the reintroduction of water into reservoirs without necessitating surface lifting. The adaptability of centrifugal pumps underscores their continual expansion and acceptance across various industrial applications.

The submersible pumps segment, by type, is expected to grow at the highest CAGR during the forecast period.

This report segments the oil and gas pumps market based on type into two segments: submersible pumps and non-submersible pumps. The submersible pumps segment is expected to grow at the highest CAGR during the forecasted period. Submersible pumps, as their name suggests, are designed to operate while fully immersed in tanks, wells, or other fluid-containing containers. Tailored for complete submersion, these pumps are particularly suitable for pumping fluids like crude oil or water. Their efficiency shines in applications such as oil wells or storage tanks, where they prove adept at seamlessly lifting substantial volumes of fluids to the surface.

North America is expected to be the largest region in the oil and gas pumps market.

North America is expected to be the largest oil and gas pumps market during the forecast period. The North America region comprises major economies such as US, Canada and Mexico. As per the report from the US Energy Information Administration, the United States claimed the title of the largest global crude oil producer in 2022, representing 14% of the world's total crude oil production. Similarly, Canada contributed to approximately 5.6% of the world's crude oil production in the same period. The expansion of the oil and gas pumps market is propelled by the increasing exploitation of unconventional resources in both the US and Canada. Additionally, the demand emanating from onshore and offshore fields in the Gulf of Mexico is anticipated to be a significant factor fostering market growth throughout the forecast period. Projections indicate that North America is poised to experience the initiation of 594 operational projects between 2023 and 2027.

Some of the major players in the oil and gas pumps market are including Atlas Copco AB (Sweden); Flowserve Corporation (US); Sulzer Ltd (Switzerland); KSB SE & Co. KGaA (Germany); Nikkiso Co., Ltd. (Japan). The major strategies adopted by these players include contracts, agreements, partnership, collaborations, and expansions.

According to a research report "Hydrogen Market - Global Forecast to 2030", the hydrogen market is projected to reach USD 410.6 billion by 2030 from an estimated USD 242.7 billion in 2023, at a CAGR of 7.8% during the forecast period.

Hydrogen is the lightest and most abundant element in the universe. Hydrogen gas has an excellent energy carrying capacity. It can be produced in large quantities and supplied to large-scale industries for various operations. It can be produced as a principal and by-product from various primary energy sources (such as wind, solar, coal, natural gas, and nuclear). Currently, hydrogen is produced in bulk for many value-added uses and chemical substances. It delivers power for various applications, including fuel cells and combined heat and power technologies. global push to reduce carbon emissions and combat climate change has led to an increased focus on clean and sustainable energy sources and drive the demand for hydrogen market.

The generation type segment, by sector, is expected to have the largest market during the forecast period.

Based on sector, the hydrogen market has been segmented into generation type, storage, and transportation. The generation type segment is expected to hold largest share during the forecast period. Governments and businesses are looking at low-carbon and zero-emission options as a result of the pressing need to slow down climate change and cut greenhouse gas emissions. Since it generates no carbon dioxide when used, green hydrogen generation offers a workable answer to the problem of decarbonization. Additionally, hydrogen is used as a feedstock or process fuel by many sectors, including chemical manufacture, refineries, and the production of steel. The demand for low-carbon and green hydrogen is rising as industry work to minimize their carbon footprint.

The mobility segment, by application, is expected to be the fastest growing during the forecast period

This report segments the hydrogen market based on application into three segments: energy, mobility, and chemical & refinery. The mobility segment is expected to be the fastest growing during the forecast period. Owing to the rising adaption of the fuel cell electric vehicles and hydrogen fueling station. Due to the hydrogen fuel cell's electrochemical reaction only producing water vapor as a byproduct, FCEVs have zero emissions. Due to this feature, FCEVs are a desirable alternative for both consumers and governments aiming to reduce air pollution and battle climate change.

North America is expected to be the largest region in the hydrogen market

North America is expected to be the largest hydrogen market during the forecast period. The North America region, comprising of US, Canada, and Mexico. Governments are dedicated to combating climate change and lowering greenhouse gas emissions. One important clean energy carrier that can aid in achieving carbon neutrality and promoting sustainable development is hydrogen, especially green hydrogen produced from renewable sources.

Some of the major players in the hydrogen market are Linde plc (Ireland), Air products and Chemicals, Inc. (US), Air Liquide (France), Worthington Industries (US), Cryolor (France), Hexagon Purus (Norway), and NPROXX (Netherlands). The major strategies these players adopt include merger & acquisitions, contracts, agreements, partnerships, and investments & expansions.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

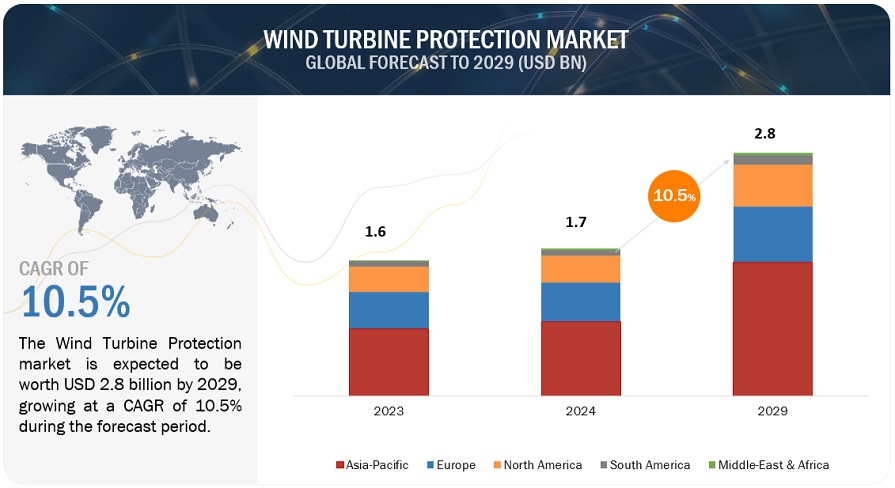

According to a research report "Wind Turbine Protection Market by Equipment (Blades, Nacelles, Towers), Protection Type (Coatings (Epoxy, Polyurethane) and Tapes & Films), End User (Onshore and Offshore), & Region (North America, Europe, APAC, MEA) - Global Forecast to 2029" published by MarketsandMarkets, the Wind turbine protection market is forecast to reach USD 2.8 billion by 2029 from an estimated USD 1.7 billion in 2024, at a CAGR of 10.5% during the forecast period (2024-2029).

Wind turbine protection is essential because they face numerous environmental challenges, including rain, hail, blowing sand, and salt spray, which can cause significant leading-edge erosion on the blades. This erosion can be severely affecting the integrity and efficiency of the blades. wind turbine protection is essential to safeguard the blades, nacelle, and internal components, maintain aerodynamic efficiency, prevent damage and downtime, and extend the operational lifespans of wind turbines.

The Nacelle, by equipment, is expected to grow as the Second largest segment during the forecast period.

Based on equipment, the wind turbine protection market has been split into Nacelle, Blades, Tower and others. The Nacelle segment in the wind turbine protection market is anticipated to be the second largest because the nacelle, houses critical components like the generator and gearbox which demands robust protection against weather elements and thermal stress to maintain operational integrity. The nacelle is a vital component that protects the turbine machinery, enables safe maintenance, optimizes airflow, and withstands wind forces.

Onshore, by End user, is expected to grow as the largest segment during the forecast period.

Based on End user, the wind turbine protection market has been split into Onshore and Offshore. The Onshore segment in the wind turbine protection market is anticipated to be the largest because the onshore wind farms are generally less expensive compared to offshore projects. The onshore segment experienced rapid growth because of the cost advantages, technological advancements and better infrastructure.

Coatings, by protection type, are expected to grow as the largest segment during the forecast period.

This report segments the wind turbine protection market based on offering into Various protection types: Coatings, Tapes & Films. The coatings segment in the wind turbine protection market is anticipated to be the largest because the coatings include protection against corrosion, particularly in harsh offshore environments, and resistance to erosion caused by rain, sand, and dust, which is vital for maintaining the aerodynamic efficiency of the blades. The benefits of applying these coatings are extended the operational lifespan of wind turbines by preventing corrosion and wear, which in turn reduces the frequency and costs associated with maintenance.

Europe is expected to be the Second largest region in the wind turbine protection market

Europe is expected to be the Second largest region in the wind turbine protection market during the forecast period. The region's increasing focus on wind turbine protection is due to the presence of major wind turbine manufacturers, including Vestas, Siemens Gamesa, and Nordex. Europe is leading the global expansion of offshore wind, with countries like the UK, Germany, and the Netherlands investing heavily in offshore wind projects.

Some of the major players in the wind turbine protection market are BASF SE (Germany), 3M (US), Akzo Nobel N.V. (Netherlands), Trelleborg AB (Sweden), Hempel A/S (Denmark). The major strategies adopted by these players include sales contracts, product launches, investments, collaborations, partnerships, and expansions.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

The global small modular reactor market size is estimated to be USD 5.8 billion in 2023 and is projected to reach USD 6.8 billion by 2030, at a CAGR of 2.3% during the forecast period. Factors such as the versatile nature of nuclear power and the relative advantages of SMRs such as modularization and factory construction are enabling the growth of the market.

"Small modular reactors (SMRS) are defined as nuclear reactors generally 300 MWe equivalent or less, designed with modular technology using module factory fabrication, pursuing economies of series production and short construction times," according to the World Nuclear Association. The ability of SMRS to meet the requirements of flexible power generation for a wide range of applications, such as power generation, process heating, desalination, hydrogen production, industrial applications, and replacing ageing fossil fuel fired power plants, has increased demand for them.

In 2022, the Asia Pacific dominated the global small modular reactor market, followed by Europe and Americas. The region, by country, has been segmented into the China, Japan, India, South Korea, and the Rest of Asia Pacific. Due to the enormous number of SMR projects in China, Asia Pacific is a big contributor to the small modular reactor industry in the current environment. SMRs have the potential to replace coal- and other fossil-fuel-fired power stations in the region for power production and process heat applications, which will likely promote the expansion of the regional small modular reactor market.

The upto 100 MW segment by power rating is expected to be the third-largest growing segment of the small modular reactor market. The reactor unit can be built in a factory and delivered to the site of installation. Because of the modular construction, many SMR units can be deployed together to satisfy varied energy demands. A 100 MW SMR's major use is electricity generating. It may function as a stand-alone power plant, supplying clean and dependable electricity to cities, industries, and isolated regions. The excess heat generated by a 100 MW SMR can be used for district heating, which involves distributing thermal energy to surrounding residential, commercial, and institutional buildings for space heating and water heating.

The gases segment by coolant is projected to be the fastest growing segment of the small modular reactor market. During operation, the gas-cooled reactor uses helium as a coolant medium, allowing it to be easily pressurized and maintain a stable high temperature, allowing for greater operational efficiency. Using gas as a medium in the reactor can prevent corrosion on the reactor's surfaces, reducing the need for maintenance. These operational advantages are propelling the gases segment forward. Graphite is used as a neutron moderator in gas-cooled reactors, and carbon dioxide gas is used as a coolant.

The light-water reactors segment by type is projected to be the fastest growing segment of the small modular reactor market. In 2022, the light water reactor category accounted for 40.6% of the small modular reactor market. These reactors, which use common water as a coolant, are the most widely used since they pose the fewest technological dangers. SMR designs based on LWR technology are similar to large-scale LWRs in use today. Such SMRS employ well-tested technologies and products with small and integrated components and higher passive safety measures over current big scale LWRS. Light-water SMRS have a better level of technological readiness than other SMB designs. Because traditional LWR technology is well-developed, these reactors provide fewer hurdles to present licencing processes. Most regulators are familiar with the technology, resulting in a relatively short learning curve for both regulatory bodies and designers in light water reactors. In the case of a Pressurised Water Reactor (PWR), this is done after the safety rods have been lowered and unlatched.

Europe is expected to grow at the second-highest CAGR during the forecast period. Russia, the United Kingdom, France, and the rest of Europe are all considered in the European small modular reactor market. Italy, Luxembourg, Denmark, the Czech Republic, Sweden, Ukraine, Finland, Estonia, Poland, and Romania are included in the rest of Europe. Nuclear energy accounts for around 28.4% of the region's electricity generation mix, according to the BP Statistical Review of World Energy 2022. The region was responsible for 30.2% of global nuclear power usage. Investments in SMRS development, as well as a trend towards the usage of clean energy to address climate change, are expanding the potential for SMRS deployment in this region. For instance, the government dedicated USD 298 million to SMRS in 2021 as part of the UK Research and Innovation (UKRI) Low-Cost Nuclear (LCN) programme in November 2020. UKRI offered an initial match financing of USD 23 million to the UK SMR consortium lead by Rolls-Royce in November 2019 for the development of a conceptual SMR design. Rosatom (Russia) announced intentions to invest USD 7 billion in new nuclear technology by 2030 in June 2021.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

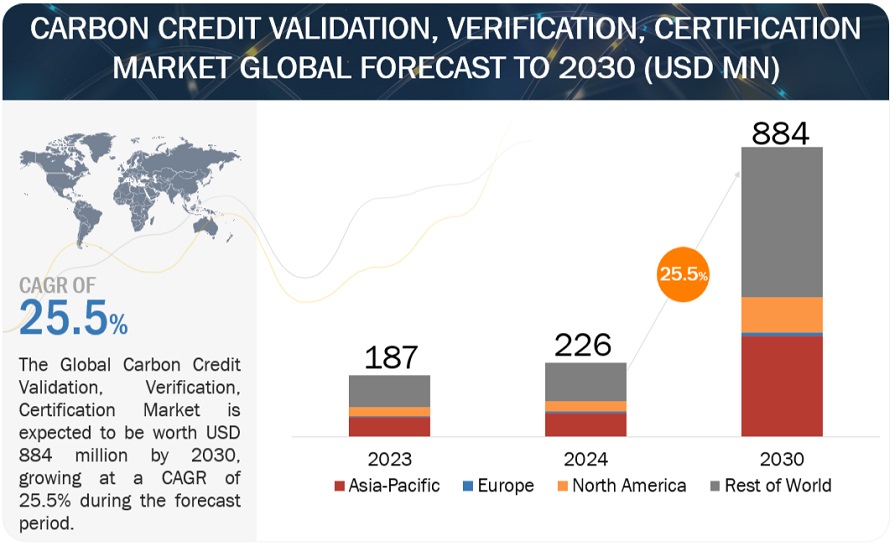

The market size for global carbon credit validation, verification, certification is projected to reach approximately USD 884 million by the year 2030, as compared to the estimated value of USD 226 million in 2024, at a Compound Annual Growth Rate (CAGR) of 25.5% over the forecast period. The global carbon credit validation, verification, and certification market is driven by several key factors. Governments worldwide are implementing stringent environmental regulations and carbon pricing mechanisms to curb greenhouse gas emissions. These policies, such as the European Union Emissions Trading System (EU ETS) and California's Cap-and-Trade Program, necessitate the validation, verification, and certification of carbon credits, ensuring that organizations meet their compliance obligations. Increasingly, corporations are adopting sustainability strategies to enhance their environmental credentials and meet stakeholder expectations. Companies are voluntarily purchasing carbon credits to offset their carbon footprints, driving demand for rigorous validation and verification processes to guarantee the credibility and impact of their investments in carbon reduction projects.

Investors are increasingly prioritizing environmental, social, and governance (ESG) criteria in their investment decisions. This trend is propelling businesses to demonstrate their commitment to reducing carbon emissions through verified carbon credits. The emphasis on ESG performance fuels the demand for robust certification standards to ensure transparency and accountability. Innovations in technology, such as blockchain, remote sensing, and Geographic Information Systems (GIS), are enhancing the efficiency and accuracy of carbon credit validation and verification processes. These technologies facilitate real-time monitoring and reporting, making it easier to track emissions reductions and verify the authenticity of carbon credits, thereby boosting market confidence and adoption. International agreements like the Paris Agreement have set ambitious global targets for reducing greenhouse gas emissions. These agreements encourage countries to adopt carbon pricing mechanisms and promote the use of carbon credits as a tool for achieving national and international climate goals. This global commitment to climate action drives the need for reliable validation, verification, and certification systems to ensure the effectiveness of carbon markets.

Agriculture & Forestry segment, by Sector, to hold the second largest market in carbon credit validation, verification, certification.

Agriculture and forestry occupy a prominent position in the global carbon credit validation, verification, and certification market due to their substantial carbon sequestration capabilities and the increasing adoption of sustainable practices. These sectors are pivotal in absorbing carbon dioxide through activities like reforestation, afforestation, and soil carbon enhancement in agriculture. Governments and international initiatives like REDD+ incentivize these practices, driving demand for validation and verification services. Corporations and investors also see these sectors as crucial for offsetting carbon footprints and integrating environmental goals into their strategies. Technological advancements in remote sensing and blockchain enhance the accuracy and transparency of carbon credit monitoring, further bolstering confidence in these sectors' contributions to the market.

North America to emerge as the second-largest carbon credit validation, verification, certificationmarket.

North America holds the second largest market share in the global carbon credit validation, verification, and certification market primarily due to robust regulatory frameworks promoting emissions reductions and carbon trading. The region's commitment to climate action, supported by policies like the California Cap-and-Trade Program and initiatives in Canada, stimulates demand for verification and certification services. Additionally, a mature financial market and significant corporate interest in sustainability drive the adoption of carbon credits as a tool for achieving environmental goals. North American companies and organizations actively engage in offset projects across various sectors, contributing to the region's substantial market presence in carbon credit validation and certification.

Key players in the global carbon credit validation, verification and certification market include VERRA (US), Gold Standard (Switzerland), DNV GL (Norway), TÜV SÜD (Germany), SGS Société Générale de Surveillance SA. (Switzerland), Intertek Group plc (UK), Bureau Veritas (France), The ERM International Group Limited (UK), SCS Global Services (US), ACR (American Carbon Registry) (US), Climate Action Reserve (US), RINA S.p. A. (Italy), Aenor (Spain), SustainCERT (Luxembourg), Aster Global Environmental Solutions, Inc. (US), Carbon Check (India), Ancer Climate, LLC (US), Carbon trust (UK), First Environment Inc. (US), CRS (US), Cotecna (Switzerland), and Carbon credit Capital (US).

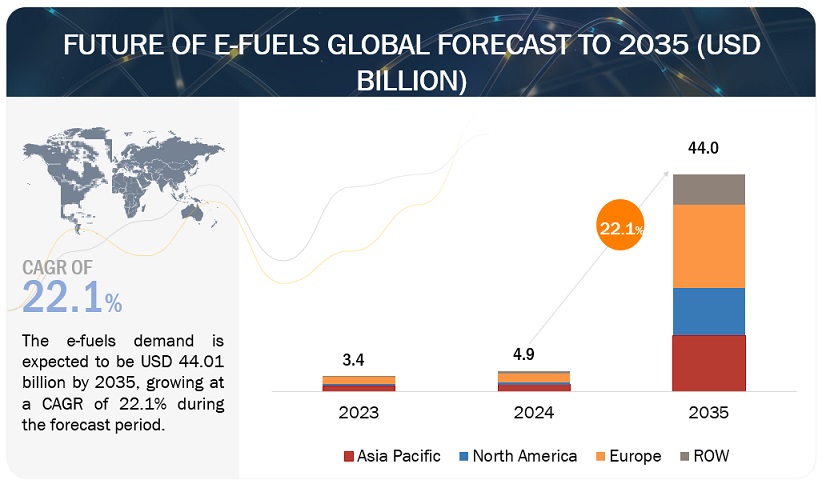

According to a research report "Future of E-fuels Market by Renewable Source (Solar, Winds), Fuel Type (E-Methane, E-Kerosene, E-methanol, E-Ammonia, E-Gasoline), State (Gaseous, Liquid), End-Use Application (Transportation, Power Generation) & Region - Global Forecast to 2035" published by MarketsandMarkets, the global e-fuel demand is expected to grow to USD 44.0 billion by 2035, up from USD 4.9 billion in 2024, at a CAGR of 22.1 % during the forecast period. Demand for e-fuels is increasing due to their ability to reduce carbon emissions and ease energy storage difficulties. E-fuels, or synthetic fuels created from renewable energy, offer a solution to decarbonize industries that rely heavily on liquid fuels, such as transportation and aviation. They may store excess renewable energy and offer a carbon-neutral solution for difficult-to-electrify applications such as heavy-duty vehicles, shipping, and industrial operations. Because of their adaptability, e-fuels are an important component of efforts to reduce greenhouse gas emissions and transition to more sustainable energy solutions, supporting their growing demand in sectors seeking carbon neutrality and energy security.

In addition to transportation and aviation, e-fuels are being utilized in power generation, heating, and as an energy carrier in remote or off-grid areas, which is driving market growth. The growing emphasis on sustainable energy sources, along with the need to decarbonize various sectors, is hastening e-fuel research, development, and adoption as a vital component in the worldwide transition to a greener, more ecologically responsible energy landscape.

“E-ammonia is expected to be the largest market in fuel type during the forecast period.”

E-ammonia is predicted to have the greatest CAGR throughout the forecasted period. The growing global need for E-ammonia may be used as an energy carrier, allowing for the transportation and storage of renewable energy, which is critical for grid stability and providing a steady energy supply. The e-ammonia is a promising new fuel with the potential to play a significant role in reducing greenhouse gas emissions and decarbonizing the global economy. Although e-ammonia is currently more expensive to produce than traditional fuels, the cost of production is expected to reduce with technological advances. The European Union is supporting the development and commercialization of e-ammonia through its Horizon 2020 research and innovation program. Such initiatives are expected to boost the market for e-ammonia in the coming years. Various developments happening around e-ammonia are also expected to drive the market. For example, in August 2023, a Norway-based company Yara announced its plan to build a new e-ammonia plant in Herøya, Norway. The plant is expected to produce 360,000 tonnes of e-ammonia per year, and it is scheduled to start production in 2026.

“Liquid segment will be the largest market by state during the forecast period.”

The report divides the e-fuels market by state into two segments: gas and liquid. The liquid segment is expected to be the largest and fastest-growing segment during the forecast period due to its wide range of applications, which include transportation, aviation, shipping, and industrial processes, making it a versatile solution for reducing carbon emissions in a variety of industries. Because liquid e-fuels work with existing combustion engines, fuel distribution systems, and storage infrastructure, they offer a viable and adaptable option for a wide range of applications.

“Europe is predicted to have the largest e-fuels market.”

Europe is predicted to be the largest e-fuel market throughout the forecast period. The European area includes significant economies such as Germany, Norway, the United Kingdom, Denmark, Sweden, and the rest of Europe. Italy, France, and Poland make up the majority of Asia Pacific's remaining countries. This is due to several causes, including the region's expanding population, greater urbanization, and rising energy consumption. As a result of these factors, carbon emissions have risen dramatically, posing a huge environmental threat to the region. European governments are increasingly supportive of e-fuels as a way to reduce carbon emissions and improve air quality. E-fuels are produced from renewable energy sources such as solar and wind power and may be used to power cars, generate electricity, and heat homes and businesses.

Saudi Arabian Oil Co. (Saudi Arabia), Audi AG (Germany), Siemens Energy (Germany), Sunfire Gmbh (Germany), Mitsubishi Corporation (Japan), Repsol (Spain), and Norsk E-Fuel (Norway) are among the leading peers in the e-fuels business.

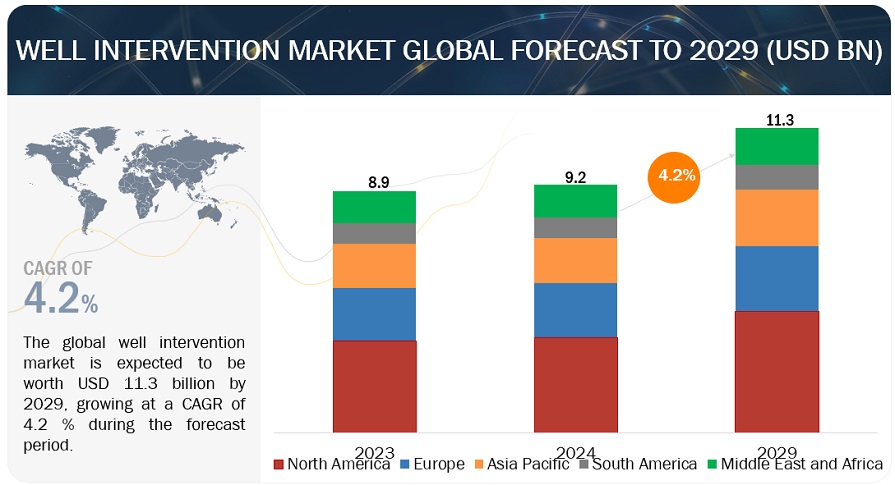

The global Well Intervention market is expected to grow from an estimated USD 9.2 billion in 2024 to USD 11.3 billion by 2029, at a CAGR of 4.2% during the forecast period, according to a new report by MarketsandMarkets™.

Well intervention is essential to maintain and optimize the productivity of oil and gas wells throughout their operational life. It encompasses various operations to alter the well's state, enhance production, mitigate issues, and extend the well lifespan. Properly targeted interventions can increase production rates, improve reservoir performance, and maximize oil and gas recovery. Ultimately, it ensures efficient resource extraction, cost-effectiveness, and safety in oil and gas operations.

Medium Intervention, by intervention type, is expected to be the fastest growing segment during the forecast period.

Based on end users, the Well Intervention market has been split into light intervention, medium intervention and heavy intervention. The medium intervention sub-segment is poised for rapid growth due to its increasing application in enhancing subsea well quality. This segment addresses crucial intervention needs in subsea environments, where maintenance and optimization are vital for efficient oil and gas extraction as the industry focuses more on subsea operations, demand for medium intervention services rises, driving market growth. Additionally, advancements in technology and methodologies tailored for subsea interventions further propel the medium intervention sub-segment's expansion, making it the fastest-growing segment in the well intervention market.

The logging and bottomhole survey segment, by service segment, is expected to be the largest market during the forecast period.

This report segments the Well Intervention market based on services into logging and bottomhole survey, tubing/packer failure & repair, stimulation, remedial cementing, zonal isolation, sand control services, artificial lift, fishing, re-perforation, and others. The logging and bottomhole survey segment is critical in assessing well conditions and optimizing production. As it offers insights into reservoir characteristics and well integrity, its demand increases alongside rising exploration activities and the need for enhanced recovery techniques. Additionally, the surge in the number of active rigs globally further boosts the significance of this sub-segment, positioning it as the largest within the well intervention market.

North America is expected to be the largest region in the well-intervention market.

North America dominates the well intervention market due to its extensive oil and gas reserves, particularly in regions like Texas and New Mexico. As the largest market, the US experiences substantial growth driven by unconventional resource exploration. Rising exploration and production activities, coupled with technological advancements, contribute to the region's market dominance, projected to continue leading the industry during the forecast period. Additionally, supportive regulatory frameworks and investments in infrastructure further fuel market expansion in North America.

Some of the major players in the Well Intervention market are Halliburton (US), SLB (US), Baker Hughes (US), Weatherford (US), Forum Energy Technologies, Inc. (US), Archer (US), Expro Group (US), Trican (Canada), Patterson -UTI (US), and Interventek Subsea Engineering (UK) . The major strategies adopted by these players include sales contracts and agreements.

The global heat pump water heater market is projected to reach USD 10.2 billion by 2028 from an estimated USD 5.2 billion in 2023, at a CAGR of 14.4% during the forecast period. Governments worldwide are enacting policies and initiatives to encourage the uptake of energy-efficient technologies like heat pump water heaters. These regulations and incentives for leveraging renewable energy sources across various applications are pivotal in propelling the expansion of the heat pump water heater market. Furthermore, consumers benefit from federal tax credits and regional utility-driven incentives, such as rebates, fostering a heightened adoption of heat pump water heaters. The amalgamation of these systems with renewable energy contributes to their increased demand, aligning with global efforts to diminish reliance on fossil fuels and minimize carbon footprints. A noteworthy catalyst for market growth is the integration of Internet of Things (IoT) technology in heat pump water heaters. This innovation facilitates remote control and monitoring, empowering users to detect anomalies and mitigate system failures.

The Air-to-air heat pump water heater, by type, is expected to be the largest segment during the forecast period.

Based on type, the heat pump water heater market is categorized into five categories: air-to-air heat pump water heater, air-to-water heat pump water heater, water source heat pump water heater, ground source (geothermal) heat pump water heater, and hybrid heat pump water heater. The air-to-air heat pump water heater is expected to be the largest segment as it holds low operating costs. Air-to-air heat pumps offer versatility for both heating and cooling, making them an attractive year-round temperature control solution for homeowners. Efficiently absorbing heat from the outside air, they are well-suited for diverse climates, particularly excelling in warmer regions where conventional air-source heat pumps thrive. The rising popularity of air source heat pumps stems from a collective effort to reduce carbon footprints and lessen reliance on traditional fossil fuel-based home heating methods. In delivering space heating, air-to-air heat pumps distribute warmed air through air handling units in designated rooms or throughout a home via duct systems.

The up to 10 kw segment, by rated capacity, is expected to grow at the highest CAGR during the forecast period.

Based on the rated capacity segment, the heat pump water heater market is segmented into six categories: up to 10 kw, 10–20 kw, 20–30 kw, 30–100 kw, 100–150 kw, and above 150 kw. Up to 10kw is expected to be the fastest growing segment during the forecast period. Heat pump water heaters up to 10 kW are commonly used for water heating due to their suitability for residential and light commercial applications. These heat pumps are efficient and can meet the hot water demands of typical households and small businesses. Additionally, they are often well-suited for integration with standard electrical systems, making them a practical choice for many water heating applications.

Europe is expected to be the fastest-growing region in the heat pump water heater market.

Europe is expected to be the fastest-growing region in the heat pump water heater market during the forecast period. The European region comprises major economies such as Germany, Italy, France and others. The surging demand for energy-efficient solutions in both commercial and residential sectors, coupled with a strategic shift towards replacing existing heating systems to curb carbon emissions, has significantly boosted the growth of the industry in Europe. The diverse climatic conditions prevalent across European countries, influenced by escalating pollution levels and the impact of global warming, have driven an increased need for advanced technological systems. Given Europe's varied climate, heat pump water heaters have emerged as a practical and favored choice for numerous households and businesses. European governments actively promote the adoption of heat pump water heaters through diverse support mechanisms and incentives. Notably, France's "My Electricity" program provides grants of up to €1,060 for air-source heat and domestic hot water heat pumps when integrated with a PV system. In Ireland, incentives include €3,500 for air-to-air heat pumps across all house types and €4,500 for air-to-water and ground-source heat pumps.

Some of the major players in the heat pump water heater market are Panasonic Corporation (Japan), LG Electronics (South Korea), Johnson Controls–Hitachi Air Conditioning (Japan), Mitsubishi Electric Corporation (Japan), Trane Technologies plc (Ireland). The major strategies adopted by these players include new product launches, acquisitions, contracts, agreements, partnerships, joint ventures, collaborations, investments, and expansions.

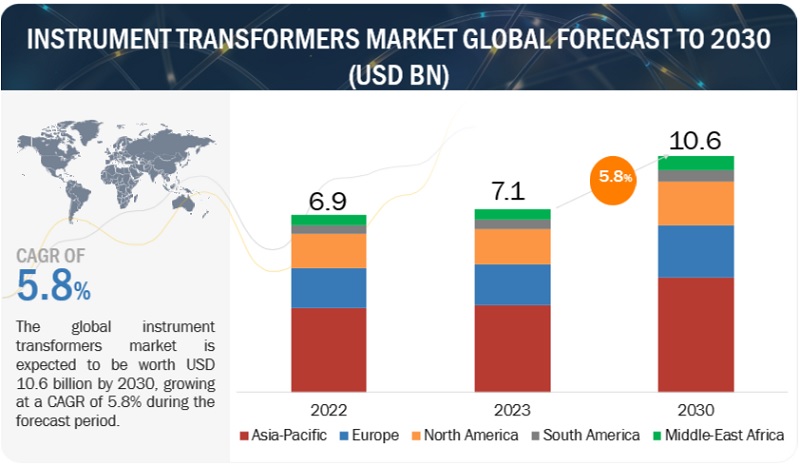

The global Instrument Transformers Marketis expected to reach USD 10.6 billion by 2030 from USD 7.1 billion in 2023 at a CAGR of 5.8% during the 2023–2030 period according to a new report by MarketsandMarkets™. The Instrument Transformers Market is poised for substantial growth during this period, primarily due to the development of power distribution infrastructure in response to the growing demand for electricity. Furthermore, the expansion of renewable energy-based capacity, increased investments in industrial production, and government initiatives for grid modernization are likely to drive the demand for instrument transformers.

Current transformers segment, by type, to occupy the majority of instrument transformers market share.

Current transformers occupy 48.7% of the market share for the year 2023. Current transformers are widely used in a variety of industries, including electricity utilities and commercial facilities. Their adaptability makes them ideal for measuring and monitoring electrical currents in a variety of environments. Current transformers are critical components of power systems for monitoring and controlling the grid. They precisely monitor current flow, giving critical information for analyzing the health and operation of the electrical grid. This skill is critical for keeping the grid stable and avoiding interruptions. Current transformers improve power quality by monitoring and adjusting current levels. Maintaining the quality of electrical power is critical for the efficient and dependable functioning of electrical systems. These are the potential reasons that are propelling the growth of current transformers in the market.

Outdoor segment, by enclosure type, to be the largest market.

Outdoor transformers are built to survive severe temperatures, humidity, and exposure to the weather. Because of their robustness, they can be deployed outside without reducing performance. These transformers are easier to construct than indoor transformers since they don't require specific interior infrastructure. This simplicity of installation helps to faster deployment and less downtime throughout the installation process. The external enclosure style allows for greater flexibility in grid layout and extension. These transformers are strategically deployed around the system to improve scalability and responsiveness to changing power distribution needs.

Asia Pacific to emerge as the largest instrument transformers market.

Ongoing enhancements in instrument transformer technologies improve their performance, reliability, and efficiency, drawing acceptance in the Asia Pacific market for updated power infrastructure. The growing use of renewable energy sources demands the use of modern instrument transformers to handle the various and intermittent nature of renewable power generation. China is the largest market for Asia-Pacific transformers, followed by India and Japan, due to increased power consumption and the construction and connection of renewable energy sources to the country's grid.

Key players in the global instrument transformers market include ABB (Switzerland), General Electric (US), Siemens (Germany), Schneider Electric (France), and Mitsubishi Electric (Japan).

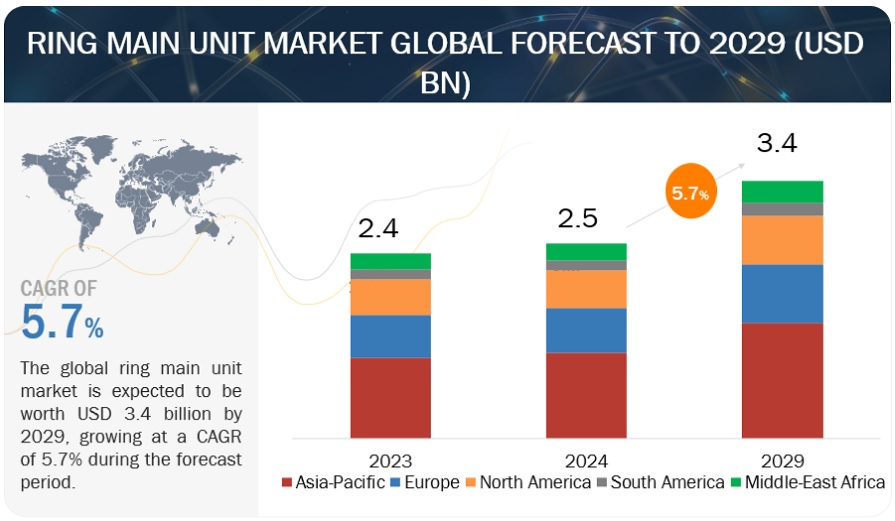

According to a research report "Ring Main Unit Market by Insulation Type (Gas-insulated, Air-insulated, Oil-insulated, Solid Dielectric), Voltage Rating (Up to 15 kV, 16-25 kV, Above 25 kV), Installation (Indoor, Outdoor), Structure, Application, Region - Global Forecast to 2029" published by MarketsandMarkets, The market for ring main units is anticipated to grow significantly; estimates place it at USD 2.5 billion in 2024 and predict it will reach USD 3.4 billion by 2029, a Compound Annual Growth Rate (CAGR) of 5.7%. The growth of the market can be primarily attributed to the expanding capacity of renewable energy sources and the ongoing efforts to enhance distribution networks, coupled with the modernization initiatives aimed at upgrading existing power infrastructure. As countries worldwide intensify their focus on sustainable energy solutions, there is a notable surge in the installation of renewable energy capacity, such as solar and wind power. This trend necessitates the integration of advanced technologies like ring main units (RMUs) to facilitate the seamless integration of renewable energy into the grid. Furthermore, the increasing complexity of distribution networks and the aging of existing power infrastructure prompt utilities to invest in modernization projects. These initiatives involve the deployment of state-of-the-art equipment like RMUs, which offer enhanced reliability, efficiency, and flexibility in managing electricity distribution.

The non-extensible segment, by structure type, is expected to be the most significant ring main unit segment during the forecast period.

The non-extensible segment is projected to emerge as the most significant segment in the ring main unit (RMU) market during the forecast period due to several factors. Non-extensible RMUs offer fixed configurations that are well-suited for specific applications and environments, providing reliability and stability in power distribution systems. These units are favored for their simplicity and robustness, requiring minimal maintenance and offering long-term operational efficiency. Additionally, non-extensible RMUs are often preferred for critical infrastructure applications where customization and flexibility are less prioritized compared to reliability and durability. As a result, the demand for non-extensible RMUs is expected to remain strong across various industries and utility networks, driving the segment's prominence in the RMU market.

The commercial building segment is anticipated to be the second-largest ring main unit segment, by application, during the forecast period.

The commercial building segment is poised to become the second-largest segment in the ring main unit (RMU) market by application during the forecast period due to several key factors. Firstly, commercial buildings, including office complexes, shopping malls, hotels, and educational institutions, require reliable and uninterrupted electricity supply to support their operations effectively. RMUs play a crucial role in ensuring the stability and resilience of power distribution within these facilities, especially during peak demand periods. Additionally, as commercial buildings increasingly adopt energy-efficient technologies and integrate renewable energy sources, the need for advanced electrical infrastructure, including RMUs, becomes paramount. RMUs enable efficient management of electricity distribution, optimizing energy usage and reducing operational costs for commercial building owners and operators. Moreover, the growing emphasis on building automation and smart technologies in commercial real estate drives the demand for RMUs with integrated smart grid capabilities, allowing for remote monitoring and control of electrical systems. As urbanization and economic development continue to drive the construction of commercial buildings globally, the demand for RMUs in this segment is expected to witness significant growth, contributing to its prominence in the RMU market landscape.

The air-insulated segment is anticipated to be the fastest-growing ring main unit segment, by insulation type, during the forecast period.

The air-insulated segment is poised to emerge as the fastest-growing segment in the ring main unit (RMU) market by insulation type, primarily due to several key advantages it offers. Firstly, air-insulated RMUs are renowned for their simplicity and reliability, as they do not rely on specialized insulating gases like SF6, making them more environmentally friendly and cost-effective. Additionally, air-insulated RMUs require minimal maintenance compared to gas-insulated counterparts, reducing operational expenses and downtime for utilities. Moreover, the modular design of air-insulated RMUs allows for easy expansion and scalability, making them well-suited for evolving distribution networks and urban environments where space constraints may be a concern. Furthermore, advancements in insulation materials and design technologies have enhanced the performance and reliability of air-insulated RMUs, further driving their adoption. As utilities increasingly prioritize sustainability, efficiency, and cost-effectiveness in their distribution networks, the air-insulated segment is expected to witness accelerated growth, cementing its position as a dominant force in the RMU market.

Asia Pacific is expected to be the fastest-growing segment in the global ring main unit market, by region, during the forecast period.

Asia Pacific is poised to emerge as the fastest-growing segment in the global ring main unit (RMU) market during the forecast period due to several compelling factors. Firstly, the region is witnessing rapid economic growth and industrialization, leading to a surge in electricity demand across various sectors such as manufacturing, infrastructure development, and commercial establishments. This escalating demand necessitates the expansion and modernization of power distribution networks, wherein RMUs play a pivotal role in ensuring efficient and reliable electricity supply. Moreover, governments in Asia Pacific are increasingly investing in infrastructure development projects, including the enhancement of electrical grids, to support economic growth and meet the needs of growing populations. Additionally, the region's commitment to renewable energy adoption, driven by environmental concerns and energy security, fuels the demand for RMUs for integrating renewable energy sources into the grid. Furthermore, initiatives aimed at rural electrification and improving energy access contribute significantly to the growing deployment of RMUs across diverse geographical and socioeconomic landscapes in the region. The convergence of these factors positions Asia Pacific as a key market for RMUs, with substantial growth opportunities both in terms of market size and expansion rate in the coming years.

ABB Ltd. (Switzerland), Siemens (Germany), Eaton (Ireland), Schneider Electric (France), and LS Electric Co., Ltd. (South Korea), Lucy Electric (UK), CG power & industrial solutions (India), Tiepco (Saudi Arabia), Orecco (China), Entec Electric & Electronics (South Korea) are major competitors in the global ring main unit market.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com