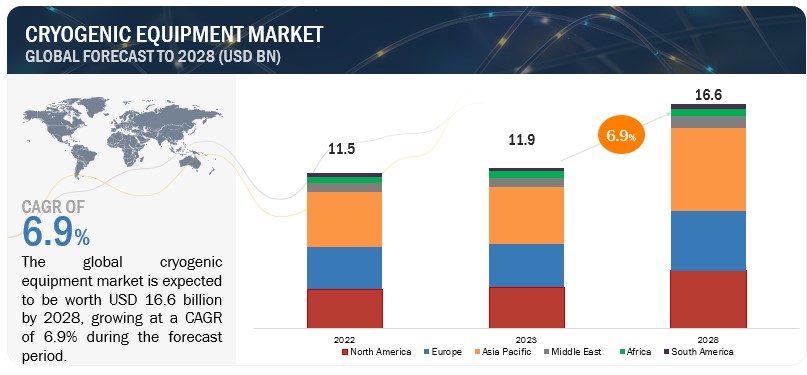

According to a research report "Cryogenic Equipment Market by Equipment (Tanks, Valves, Vaporizers, Pumps), Cryogen (Nitrogen, Argon, Oxygen, LNG, Hydrogen), End-user Industry (Energy & Power, Chemical, Metallurgy, Transportation), System Type, Application & Region - Forecast to 2028", the global cryogenic equipment market is projected to reach USD 16.6 billion by 2028 from an estimated USD 11.9 billion in 2023, at a CAGR of 6.9% during the forecast period. A cryogenic equipment is any storage or transportation apparatus that helps handle cryogenic fluids (liquefied industrial gases at temperatures below -150ºC). Typical equipment in this category include tanks, pumps, vaporizers, heat exchangers, valves, pressure regulators, and pipes. They are used in various applications, such as the production, storage, and transportation of LNG; preservation of biological materials including human tissues, sperms, and embryos; long-term storage of biological samples such as stem cells, cord blood, and tissues; development of hydrogen fuel systems, particularly for the automotive and transportation industries; as well as cooling scientific instruments on space telescopes and maintaining extremely low temperatures for space probes and vehicles, satellite launch facilities, and air separation units. The cryogenic equipment market is heavily dependent on the consumption of industrial gases that are liquefied for high-volume storage purposes. oxygen, nitrogen, argon, and hydrogen, wherein oxygen and nitrogen are such major industrial gases used across end-user industries for numerous applications. The increasing use of these industrial gases in industries such as energy & power, metallurgy, electronics, chemicals, and transportation is likely to propel the demand for cryogenic equipment. Moreover, growing popularity of liquefied natural gas as source of clean and efficient energy, will boost the demand for cryogenic equipment for the transportation and storage at LNG liquefaction and regasification terminals.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=735

The Tanks, by equipment, is expected to grow at the highest CAGR during the forecast period.

Based on equipment, the cryogenic equipment market has been split into tanks, valves, vaporizers, pumps and other equipments such as pipes, regulators, freezers, dewars, strainers, samplers, heat exchangers, leak detection equipment, dispensers, and accessories (manifolds, fittings, vacuum-jacketed/-insulated piping, hoses, connections). Tanks are expected to grow at the highest CAGR during the forecasted period. The increasing global demand for LNG tanks and microbulk tanks will be the major reason for the leading position of the tanks segment in this market in the coming years.

The nitrogen segment, by cryogen, is expected to be the largest segment during the forecast period.

This report segments the cryogenic equipment market based on cryogen into six segments: nitrogen, argon, oxygen, liquified natural gas (LNG), hydrogen, and other cryogens (helium, nitrous oxide, ethylene, and carbon dioxide). The nitrogen segment is expected to be the largest segment during the forecast period owing to its high availability in the atmosphere and its inert nature. Nitrogen is widely used in industrial and medical applications, nitrogen is also used in the energy & power industry to enhance oil recovery. It is used in fertilizers and chemical industries as well.

Asia Pacific is expected to be the largest region in the cryogenic equipment market.

Asia Pacific is expected to be the largest cryogenic equipment market during the forecast period. The Asia Pacific region comprises major economies such as China, India, Australia, Japan, Malaysia, and Rest of Asia Pacific. Rest of Asia Pacific primarily includes Thailand, the Philippines, Singapore, Indonesia, and Myanmar. . The high growth rate and market share of the Asia Pacific region can be attributed to constant LNG infrastructure developments in China, investments in the aerospace industry in India, and increasing investments in gas production and LNG imports in Australia and Japan, respectively. The significant demand for cryogenic equipment in the region is witnessed by end-user industries such as healthcare, metallurgy, energy & power, and electronics.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=735

Key market players

Some of the major players in the cryogenic equipment market are including Linde plc (Ireland); Air Liquide (France); Air Products and Chemicals, Inc. (US); Chart Industries (US); Parker Hannifin Corp. (US); Flowserve Corporation (US); Nikkiso Co., Ltd. (Japan); and INOX India Limited (India). The major strategies adopted by these players include contracts, agreements, partnership, collaborations, and expansions.

Browse Related Reports

Cryogenic Pump Market by Orientation, Design (Submersible, Non-Submersible), Type, Cryogen (Nitrogen, Argon, Oxygen, LNG, Helium, Hydrogen), End User (Energy & Power, Chemicals, Metallurgy, Healthcare & Pharmaceuticals) & Region - Global forecast to 2027

About MarketsandMarkets™

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Contact:

Mr. Aashish Mehra

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

newsletter@marketsandmarkets.com