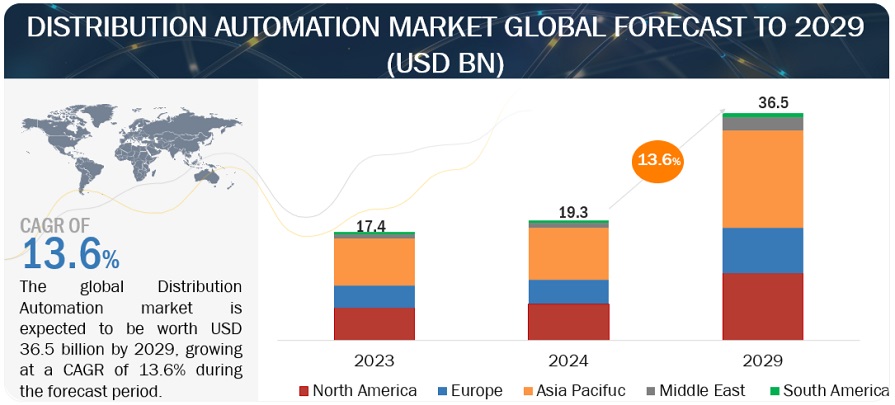

According to a research report "Distribution Automation Market by Offering (Field Devices, Software, Services), Communication Technology (Wired (Fiber Optic, Ethernet, Powerline Carrier, IP), Wireless), Utility (Public Utilities, Private Utilities) and Region - Global Forecast to 2029" published by MarketsandMarkets, the global distribution automation market is estimated to be valued at USD 19.3 billion in 2024 and is projected to reach USD 36.5 billion by 2029; growing at a CAGR of 13.6% during the forecast period. Distribution automation (DA) refers to a collection of technologies, strategies, and practices used by electric utilities to improve the efficiency, reliability, and safety of their power distribution networks. It essentially involves automating various tasks and processes within the distribution system.

The distribution automation market has promising growth potential due to the factors such as increase in need to optimize power distribution, reduce energy waste and improve system performance & increase in need for the integration of renewable energy sources.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=65029172

Field Devices segment expected to dominate distribution automation market, by offering, during the forecast period

The distribution automation market, by offerings, are divided into field devices, software & services. With respect to the distribution automation market, the field devices sector is the largest. The benefits it provides is the ability to remotely monitor distribution power grids to shorten the length of power outages, are responsible for its significant market dominance. Equipped with digital controls, switches, and sensors, they automate various electricity delivery functions.

Wireless to witness fastest growth rate in distribution automation market, by communication technology, during forecast period

The distribution automation market, by communication technology, is divided into wired and wireless. Wireless is the fastest-growing segment in Electricity Distribution Automation by communication technology, owing to rising need for real-time data interchange and data-driven decisions. Wireless communication technology also allows information to be transferred over long distances without the use of electrical lines or conductors, providing secure transmission while being cost-effective.

Private utilities to witness fastest growth rate in distribution automation market, by utility, during forecast period

The distribution automation market, by utility, is divided into private utilities and public utilities, wherein public segment accounts for the largest share. Private is fastest growing segment during the forecast period, the growth is attributed to private companies investing in advanced metering infrastructure, artificial intelligence, and smart grid infrastructure to improve reliability, faster complaint resolution, and real-time energy consumption. With increasing demand and technical developments, the government is looking to private partners to help with power distribution. Private players are viewed as valuable contributions to the sector due to their increased efficiency and experience. Private businesses may greatly contribute to the country's energy infrastructure by collaborating with the government on the Public-Private Partnership model, making distribution more cost-effective and accessible to all.

Middle East & Africa to be fastest-growing distribution automation market during forecast period

In this report, the distribution automation market has been analyzed for five regions, namely, Asia Pacific, North America, Europe, South America and Middle East & Africa. The Middle East and Africa emerge as the most rapidly advancing region in the market, projected to achieve a CAGR of 20.9% during the forecast period from 2024 to 2029. This growth is attributed to several factors, including the expansion of the industrial sector, initiatives to electrify smart cities like NEOM, government efforts to develop smart grid infrastructure, and projects focusing on electrifying rural and remote areas. Moreover, key players such as ABB, Schneider Electric, and Siemens are actively investing in the region to bolster their market presence and capitalize on the rising demand for distribution automation technologies.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=65029172

Some of the major players in the distribution automation market are ABB (Switzerland), Schneider Electric (France), Siemens (Germany), Eaton (Ireland), and General Electric Company (US). Other major players include S&C Electric Company (US), Toshiba (Japan), Landis+Gyr (Switzerland), Itron Inc (US), Hubbell (US), Xylem (US), Schweitzer Engineering Laboratories, Inc. (US) and G&W Electric (US). The major strategies adopted by these players include new product launches, contracts, agreements, partnerships, and expansions.

Browse Related Reports:

Distributed Energy Resource Management System Market by Application (Solar PV, Wind, Energy Storage, CHP, EV Charging), Software (Analytics, Management & Control, VPP), End User (Industrial, Commercial, Residential), and Region - Global Forecast to 2026

About MarketsandMarkets™

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the ’GIVE Growth’ principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact:

Mr. Aashish Mehra

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

newsletter@marketsandmarkets.com