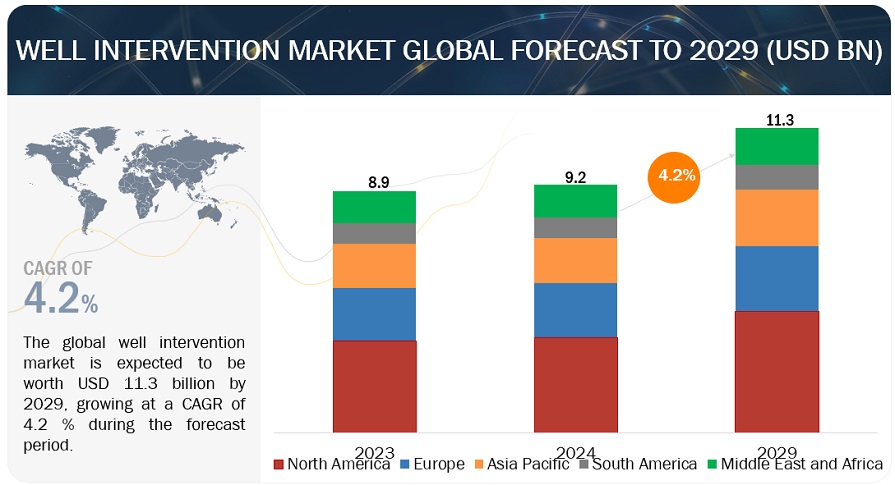

The global Well Intervention market is expected to grow from an estimated USD 9.2 billion in 2024 to USD 11.3 billion by 2029, at a CAGR of 4.2% during the forecast period, according to a new report by MarketsandMarkets™.

Well intervention is essential to maintain and optimize the productivity of oil and gas wells throughout their operational life. It encompasses various operations to alter the well's state, enhance production, mitigate issues, and extend the well lifespan. Properly targeted interventions can increase production rates, improve reservoir performance, and maximize oil and gas recovery. Ultimately, it ensures efficient resource extraction, cost-effectiveness, and safety in oil and gas operations.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1099

Medium Intervention, by intervention type, is expected to be the fastest growing segment during the forecast period.

Based on end users, the Well Intervention market has been split into light intervention, medium intervention and heavy intervention. The medium intervention sub-segment is poised for rapid growth due to its increasing application in enhancing subsea well quality. This segment addresses crucial intervention needs in subsea environments, where maintenance and optimization are vital for efficient oil and gas extraction as the industry focuses more on subsea operations, demand for medium intervention services rises, driving market growth. Additionally, advancements in technology and methodologies tailored for subsea interventions further propel the medium intervention sub-segment's expansion, making it the fastest-growing segment in the well intervention market.

The logging and bottomhole survey segment, by service segment, is expected to be the largest market during the forecast period.

This report segments the Well Intervention market based on services into logging and bottomhole survey, tubing/packer failure & repair, stimulation, remedial cementing, zonal isolation, sand control services, artificial lift, fishing, re-perforation, and others. The logging and bottomhole survey segment is critical in assessing well conditions and optimizing production. As it offers insights into reservoir characteristics and well integrity, its demand increases alongside rising exploration activities and the need for enhanced recovery techniques. Additionally, the surge in the number of active rigs globally further boosts the significance of this sub-segment, positioning it as the largest within the well intervention market.

North America is expected to be the largest region in the well-intervention market.

North America dominates the well intervention market due to its extensive oil and gas reserves, particularly in regions like Texas and New Mexico. As the largest market, the US experiences substantial growth driven by unconventional resource exploration. Rising exploration and production activities, coupled with technological advancements, contribute to the region's market dominance, projected to continue leading the industry during the forecast period. Additionally, supportive regulatory frameworks and investments in infrastructure further fuel market expansion in North America.

Request FREE Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1099

Some of the major players in the Well Intervention market are Halliburton (US), SLB (US), Baker Hughes (US), Weatherford (US), Forum Energy Technologies, Inc. (US), Archer (US), Expro Group (US), Trican (Canada), Patterson -UTI (US), and Interventek Subsea Engineering (UK) . The major strategies adopted by these players include sales contracts and agreements.

Get access to the latest updates on Well Intervention Companies and Well Intervention Industry Growth