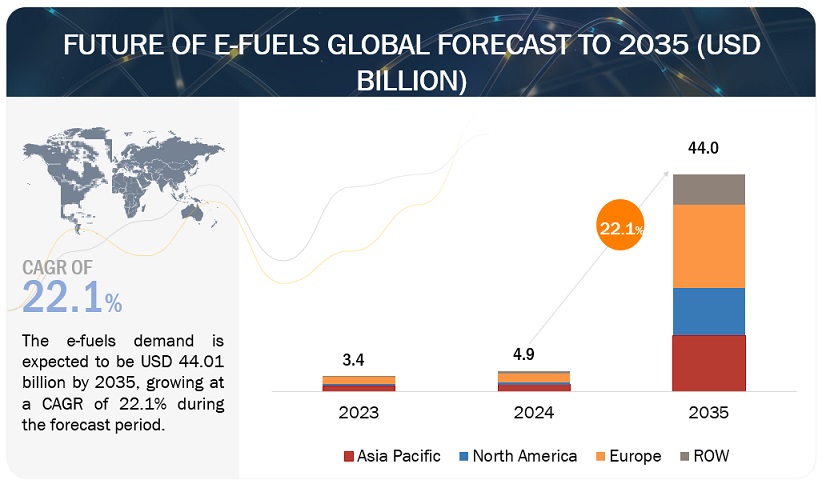

According to a research report "Future of E-fuels Market by Renewable Source (Solar, Winds), Fuel Type (E-Methane, E-Kerosene, E-methanol, E-Ammonia, E-Gasoline), State (Gaseous, Liquid), End-Use Application (Transportation, Power Generation) & Region - Global Forecast to 2035" published by MarketsandMarkets, the global e-fuel demand is expected to grow to USD 44.0 billion by 2035, up from USD 4.9 billion in 2024, at a CAGR of 22.1 % during the forecast period. Demand for e-fuels is increasing due to their ability to reduce carbon emissions and ease energy storage difficulties. E-fuels, or synthetic fuels created from renewable energy, offer a solution to decarbonize industries that rely heavily on liquid fuels, such as transportation and aviation. They may store excess renewable energy and offer a carbon-neutral solution for difficult-to-electrify applications such as heavy-duty vehicles, shipping, and industrial operations. Because of their adaptability, e-fuels are an important component of efforts to reduce greenhouse gas emissions and transition to more sustainable energy solutions, supporting their growing demand in sectors seeking carbon neutrality and energy security.

In addition to transportation and aviation, e-fuels are being utilized in power generation, heating, and as an energy carrier in remote or off-grid areas, which is driving market growth. The growing emphasis on sustainable energy sources, along with the need to decarbonize various sectors, is hastening e-fuel research, development, and adoption as a vital component in the worldwide transition to a greener, more ecologically responsible energy landscape.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=169488021

“E-ammonia is expected to be the largest market in fuel type during the forecast period.”

E-ammonia is predicted to have the greatest CAGR throughout the forecasted period. The growing global need for E-ammonia may be used as an energy carrier, allowing for the transportation and storage of renewable energy, which is critical for grid stability and providing a steady energy supply. The e-ammonia is a promising new fuel with the potential to play a significant role in reducing greenhouse gas emissions and decarbonizing the global economy. Although e-ammonia is currently more expensive to produce than traditional fuels, the cost of production is expected to reduce with technological advances. The European Union is supporting the development and commercialization of e-ammonia through its Horizon 2020 research and innovation program. Such initiatives are expected to boost the market for e-ammonia in the coming years. Various developments happening around e-ammonia are also expected to drive the market. For example, in August 2023, a Norway-based company Yara announced its plan to build a new e-ammonia plant in Herøya, Norway. The plant is expected to produce 360,000 tonnes of e-ammonia per year, and it is scheduled to start production in 2026.

“Liquid segment will be the largest market by state during the forecast period.”

The report divides the e-fuels market by state into two segments: gas and liquid. The liquid segment is expected to be the largest and fastest-growing segment during the forecast period due to its wide range of applications, which include transportation, aviation, shipping, and industrial processes, making it a versatile solution for reducing carbon emissions in a variety of industries. Because liquid e-fuels work with existing combustion engines, fuel distribution systems, and storage infrastructure, they offer a viable and adaptable option for a wide range of applications.

“Europe is predicted to have the largest e-fuels market.”

Europe is predicted to be the largest e-fuel market throughout the forecast period. The European area includes significant economies such as Germany, Norway, the United Kingdom, Denmark, Sweden, and the rest of Europe. Italy, France, and Poland make up the majority of Asia Pacific's remaining countries. This is due to several causes, including the region's expanding population, greater urbanization, and rising energy consumption. As a result of these factors, carbon emissions have risen dramatically, posing a huge environmental threat to the region. European governments are increasingly supportive of e-fuels as a way to reduce carbon emissions and improve air quality. E-fuels are produced from renewable energy sources such as solar and wind power and may be used to power cars, generate electricity, and heat homes and businesses.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=169488021

Key Players:

Saudi Arabian Oil Co. (Saudi Arabia), Audi AG (Germany), Siemens Energy (Germany), Sunfire Gmbh (Germany), Mitsubishi Corporation (Japan), Repsol (Spain), and Norsk E-Fuel (Norway) are among the leading peers in the e-fuels business.