The global fuel cell industry is projected to reach USD 8.7 billion by 2028 from an estimated USD 3.3 billion in 2023, at a CAGR of 21.7% during the forecast period.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=348

The small scale, by size, is expected to be the largest segment during the forecast period.

This report segments the fuel cell market based on size into two segments: small scale (up to 200 kW) and large scale (above 200 kW). The small-scale (up to 200 kw) segment is expected to be the largest segment during the forecast year. Fuel cells with power capacities up to 200 kW find applicability in residential and small-scale commercial settings, serving diverse purposes. These versatile systems are well-suited for deployment in backup power systems, where they ensure a reliable and continuous energy supply during outages. Additionally, they prove valuable in combined heat and power (CHP) units, simultaneously generating electricity and useful heat for enhanced efficiency in heating applications. Moreover, these fuel cells contribute to the development of microgrid installations, providing localized and decentralized energy solutions that enhance energy resilience and sustainability at a community level.

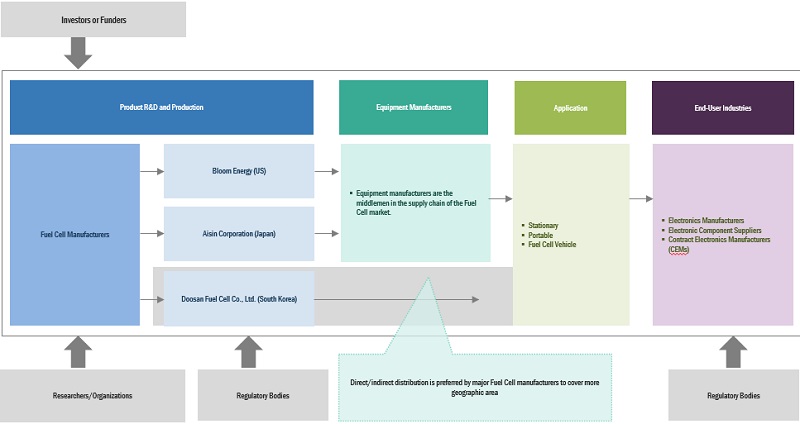

Fuel Cell Industry Ecosystem

The balance of plant, by component, is expected to be the largest segment during the forecast period.

This report segments the fuel cell market based on components into two segments: stack and balance of plants. The balance of the plant segment is expected to be the largest segment during the forecast year. The balance of plant components is crucial for the operations and efficiency of fuel cells. The enhancements in the balance of plant components are pivotal for elevating the holistic performance, robustness, and cost efficiency of fuel cell vehicles. Notably, breakthroughs in the design and functionality of air and fuel supply systems have emerged as key catalysts in augmenting the efficiency of fuel cell stacks, thereby contributing substantially to the overall efficacy of these vehicles.

Hydrogen, by fuel, is expected to be the largest segment during the forecast period.

This report segments the fuel cell industry based on fuel into five segments: hydrogen, ammonia, methanol, ethanol and hydrocarbon. The hydrogen segment is expected to be the largest segment during the forecast year. Hydrogen fuel cells generate electricity by means of the electrochemical interaction between hydrogen and oxygen, resulting in water as the sole emission. This method is eco-friendly, as it involves no release of greenhouse gases or pollutants during its operational phase. Hydrogen fuel cells find application in diverse industries for stationary power generation, serving as a dependable and effective electricity source. Commonly employed in remote areas or as backup power systems, they contribute to a stable and efficient energy supply.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=348

Asia Pacific is expected to be the largest region in the fuel cell industry.

Asia Pacific is expected to be the largest fuel cell industry during the forecast period. Governments in countries like Japan, South Korea, and China are proactively championing the advancement and integration of fuel cell technology as a pivotal component of their strategies to mitigate carbon emissions and foster the adoption of sustainable energy solutions particularly in Japan and South Korea have made substantial investments in fuel cell technology, directing their efforts towards diverse applications such as transportation and stationary power generation.

Contact:

Mr. Rohan Salgarkar

MarketsandMarkets Inc.

1615 South Congress Ave.

Suite 103, Delray Beach, FL 33445

USA: +1-888-600-6441

Email: newsletter@marketsandmarkets.com