According to a research report, the market size for synchronous generator is estimated to be USD 4.7 billion by 2023 and is projected to reach USD 5.9 billion by 2028, at a CAGR of 4.6%. A synchronous generator, also called an AC generator or alternator, is an electromechanical energy conversion device that converts mechanical energy from sources such as engines and turbines into electrical energy in the form of alternating current (AC). It is called an alternator as it produces alternating current electricity, and a synchronous generator because it is necessarily driven at synchronous speed to generate electricity at the desired frequency.

Key market players

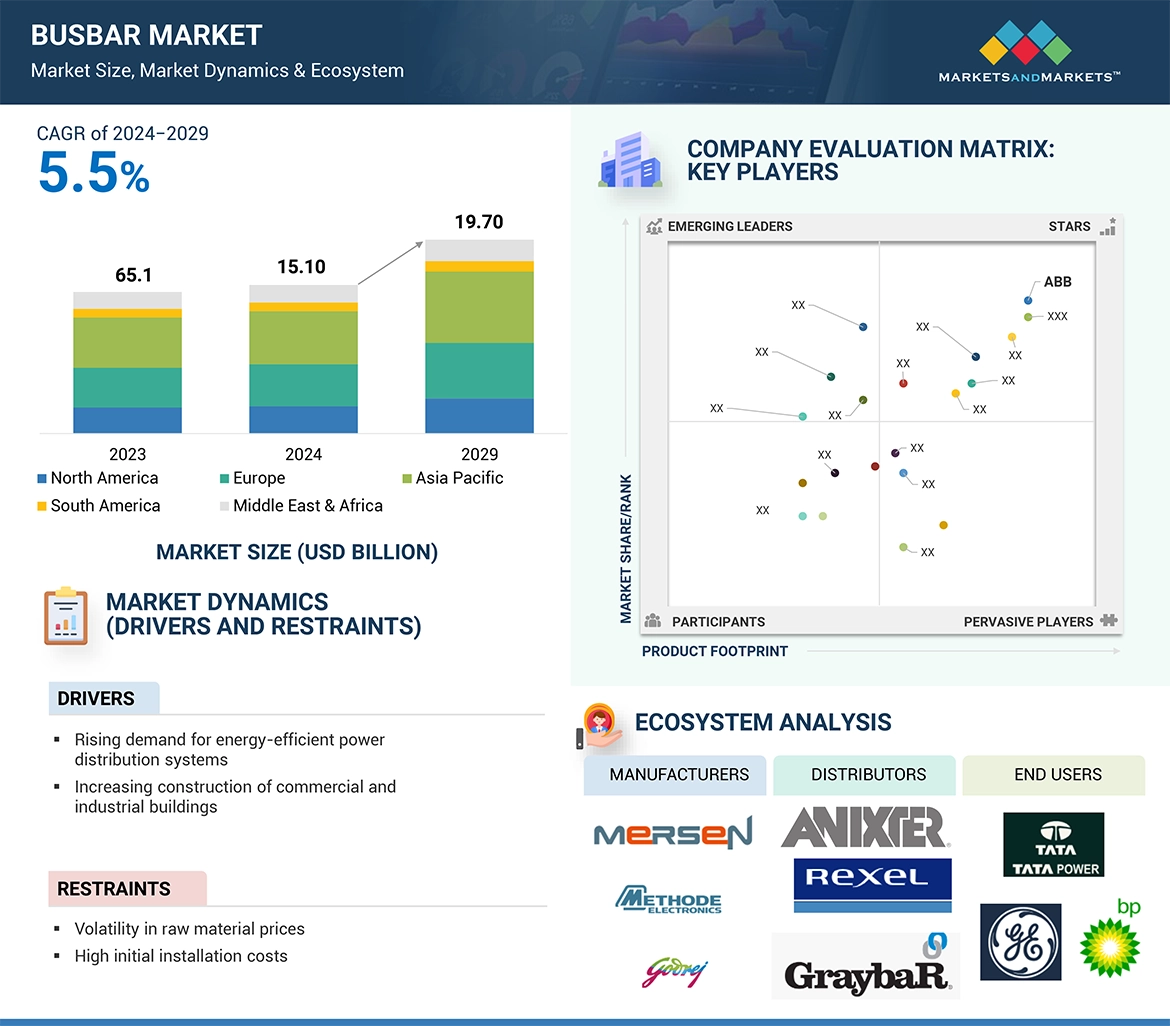

Prominent companies in this market include ABB (Switzerland), WEG (Brazil), Siemens Energy (Germany), Meidensha Corporation (Japan), and Andritz (Austria).

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=183822134

2-5 MVA segment by power rating is expected to result in the segment occupying the least market share of the synchronous generator

The 2-5 MVA segment accounted for a share of 6.2% of the synchronous generator market in 2022. synchronous generators are medium to high power rating generators that generate electrical power in the range of 2 to 5 megavolt-amperes. These generators can effectively meet the power requirements of industrial facilities, commercial establishments, and medium-sized communities. 2–5 MVA synchronous generators are designed with maintenance and serviceability in mind, ensuring convenient upkeep, and are equipped with user-friendly access points that facilitate inspections, repairs, and component replacements, minimizing downtime and maximizing generator performance.

Gas turbines are estimated to be the fastest growing market

Based on the prime mover segment of synchronous generator systems, gas turbine synchronous generators have fast start-up time than other generators, enabling them to respond rapidly to fluctuations in power demand. They can run on different fuels such as natural gas, diesel, and kerosene, hence providing flexibility in fuel choice. Due to their compact and lightweight design, gas turbine generators are well-suited for applications where space is limited.

Key Stakeholders

· Government Utility Providers

· Independent Power Producers

· Synchronous Generator manufacturers

· Power equipment and garden tool manufacturers

· Consulting companies in the energy & power sector

· Generation utilities

· Government and research organizations

· Organizations, forums, and associations

· Raw material suppliers

· State and national regulatory authorities

· Synchronous Generator manufacturers, distributors, and suppliers

· Synchronous Generator original equipment manufacturers (OEMs)

Request sample pages @

https://www.marketsandmarkets.com/requestsampleNew.asp?id=183822134

Asia Pacific likely to emerge as the largest synchronous generator market

Asia Pacific accounted for a 44.4% share with a market size worth USD 2,037.2 million in 2022. The Asia Pacific synchronous generator market, by country, has been segmented into the China, India, Japan, Australia, South Korea, and and Rest of Asia Pacific. In the region, Natural gas is being used as one of the primary energy source as it is much cleaner for environment, and thus power generation is experiencing significant development opportunities for gas turbines synchronous generator. Natural gas plants are likely to dominate this market’s growth during the forecast period due to increased usage of natural gas for power generation across the region, especially in India and China. A new thermal plant is under study, which uses thorium as the primary fuel. The progress in this field can lead to a renaissance in thermal power plants as thorium creates much less waste, is cheaper, and is more abundant than uranium. This, in turn, is expected to create significant opportunities for synchronous generator manufacturers to tap into this new market.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Contact:

Mr. Rohan Salgarkar

MarketsandMarkets Inc.

1615 South Congress Ave.

Suite 103, Delray Beach, FL 33445

USA: +1-888-600-6441

Email: newsletter@marketsandmarkets.com