According to the new market research report "Variable Frequency Drive (VFD) Market by Type (AC, DC, and Servo), End-Users (Industrial, Infrastructure, Oil & Gas, and Power Generation), Application (Pumps, Fans, Compressors, and Conveyors), Power Range, Voltage, and Region – Global Forecast to 2025", published by MarketsandMarkets™, the global Variable Frequency Drive Market is projected to reach USD 24.3 billion by 2025 from an estimated USD 19.2 billion in 2020, at a CAGR of 4.8% during the forecast period. This growth can be attributed to factors such as growing regulations towards energy efficiency, upgradation & modernization of aging infrastructure for safe & secure electrical distribution systems, and increasing rate of industrialization and urbanization. However, stagnant growth of the oil & gas industry and decrease in the exploration & production activity is hindering the growth of the Variable Frequency Drive Market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=878

The low voltage segment is expected to hold the largest share of the Variable Frequency Drive Market, by voltage type, during the forecast period

The low voltage segment, by voltage, is estimated to account for the largest share during the forecast period. Low voltage variable frequency drives are used in a wide range of applications such as pumps, fan, belt conveyor, centrifugal pumps, and centrifugal compressors. Low voltage variable frequency drives are designed for industrial applications, especially in process industries such as pulp & paper, power, water & wastewater, and oil & gas. Thus, the growing use of low voltage drives in a wide range of applications is expected to boost the growth for this segment

Browse in-depth TOC on "Variable Frequency Drive Market"

104 – Tables

66 – Figures

202 – Pages

View Detailed Table of Content Here: https://www.marketsandmarkets.com/Market-Reports/variable-frequency-drive-market-878.html

The low power drive segment, by power rating, is expected account for the largest share during the forecast period

The low power drive segment is expected to hold the largest market share and grow at a CAGR of 4.0% during the forecast period. Low power drives offer a quick payback period due to higher energy savings at low capital costs and better process control with increased motor control. Variable frequency drives with a 6–40 kW power range are used in different industries such as building, automation, oil & gas, food & beverage, and pulp & paper. Thus, the growing need for energy efficiency in these industries is expected to drive the growth of the segment.

Asia Pacific: The leading Variable Frequency Drive Market

The Asia Pacific region is projected to be the largest Variable Frequency Drive Market by 2025. Countries such as China, India, Japan, and South Korea are among the major countries considered as the main manufacturing hubs for variable frequency drives. Countries in Asia Pacific are focused towards energy efficiency and variable frequency drives are expected to play an important role in helping these countries to meet their energy efficiency targets, as the primary function of these drivers is to save energy. Thus, massive investments in the manufacturing industry are driving the growth of the Variable Frequency Drive Market in the Asia Pacific region

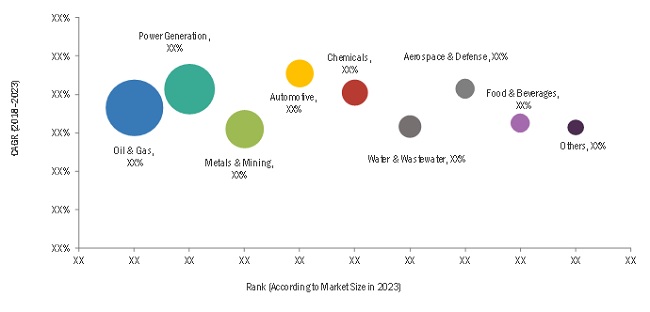

The growth in industrialization is driving a continuous need for electric motors, which consume one-third of the total electricity produced globally. Limited conventional power generation, coupled with a continuous rise in electricity prices, has encouraged companies to invest in energy-efficient equipment to increase energy efficiency. Energy-intensive industries such as oil & gas, metals & mining, pulp & paper, cement, and water & wastewater are using variable frequency drives to reduce energy consumption and CO2 emissions. Therefore, the increasing need for energy efficiency is expected to drive the growth of the variable frequency drives market.

Inquiry Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=878

To enable an in-depth understanding of the competitive landscape, the report includes the profiles of some of the top players in the Variable Frequency Drive Market. Some of the key players are ABB (Switzerland), Siemens (Germany), Schneider Electric (France), Danfoss (Denmark), Rockwell Automation (US). The leading players are adopting various strategies to increase their share in the Variable Frequency Drive Market.

Browse Adjacent Markets: Energy and Power Market Research Reports & Consulting

Browse Related Reports:

Europe VFDs Market by Application (Pump, Fan, Compressor, Conveyor, Extruder), Power Rating (0–0.5, 0.5–20, 20–50, 50–200, >200kW), Voltage (Low and Medium) And Countries (Germany, Russia, UK, France, Italy, Spain) - Global Forecast to 2024

https://www.marketsandmarkets.com/Market-Reports/europe-vfd-market-220609858.html

Marine VFD Market by Type (AC Drive, DC Drive), Voltage (Low Voltage (Up to 1 kV), Medium Voltage (Above 1 kV)), Application (Pump, Fan, Compressor, Propulsion / Thruster, Crane & Hoist) and Region - Global Forecast to 2024

https://www.marketsandmarkets.com/Market-Reports/marine-vfd-market-85395523.html

About MarketsandMarkets™

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth niche opportunities/threats which will impact 70% to 80% of worldwide companies' revenues. Currently servicing 7500 customers worldwide including 80% of global Fortune 1000 companies as clients. Almost 75,000 top officers across eight industries worldwide approach MarketsandMarkets™ for their painpoints around revenues decisions.

Our 850 fulltime analyst and SMEs at MarketsandMarkets™ are tracking global high growth markets following the "Growth Engagement Model – GEM". The GEM aims at proactive collaboration with the clients to identify new opportunities, identify most important customers, write "Attack, avoid and defend" strategies, identify sources of incremental revenues for both the company and its competitors. MarketsandMarkets™ now coming up with 1,500 MicroQuadrants (Positioning top players across leaders, emerging companies, innovators, strategic players) annually in high growth emerging segments. MarketsandMarkets™ is determined to benefit more than 10,000 companies this year for their revenue planning and help them take their innovations/disruptions early to the market by providing them research ahead of the curve.

MarketsandMarkets's flagship competitive intelligence and market research platform, "Knowledge Store" connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets.

Contact:

Mr. Aashish Mehra

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA: +1-888-600-6441

Email: sales@marketsandmarkets.com

Research Insight: https://www.marketsandmarkets.com/ResearchInsight/variable-frequency-drive-market.asp

Visit Our Web Site: https://www.marketsandmarkets.com

Content Source: https://www.marketsandmarkets.com/PressReleases/variable-frequency-drive.asp

/image%2F4763514%2F20210127%2Fob_47e87b_chp-market.jpg)