Energy and Power Market Research Reports & Consulting - The report captures in-depth strategic insights on crucial topics which helps our clients make their informed decisions

The global heat pump water heater market is projected to reach USD 10.2 billion by 2028 from an estimated USD 5.2 billion in 2023, at a CAGR of 14.4% during the forecast period. Governments worldwide are enacting policies and initiatives to encourage the uptake of energy-efficient technologies like heat pump water heaters. These regulations and incentives for leveraging renewable energy sources across various applications are pivotal in propelling the expansion of the heat pump water heater market. Furthermore, consumers benefit from federal tax credits and regional utility-driven incentives, such as rebates, fostering a heightened adoption of heat pump water heaters. The amalgamation of these systems with renewable energy contributes to their increased demand, aligning with global efforts to diminish reliance on fossil fuels and minimize carbon footprints. A noteworthy catalyst for market growth is the integration of Internet of Things (IoT) technology in heat pump water heaters. This innovation facilitates remote control and monitoring, empowering users to detect anomalies and mitigate system failures.

The Air-to-air heat pump water heater, by type, is expected to be the largest segment during the forecast period.

Based on type, the heat pump water heater market is categorized into five categories: air-to-air heat pump water heater, air-to-water heat pump water heater, water source heat pump water heater, ground source (geothermal) heat pump water heater, and hybrid heat pump water heater. The air-to-air heat pump water heater is expected to be the largest segment as it holds low operating costs. Air-to-air heat pumps offer versatility for both heating and cooling, making them an attractive year-round temperature control solution for homeowners. Efficiently absorbing heat from the outside air, they are well-suited for diverse climates, particularly excelling in warmer regions where conventional air-source heat pumps thrive. The rising popularity of air source heat pumps stems from a collective effort to reduce carbon footprints and lessen reliance on traditional fossil fuel-based home heating methods. In delivering space heating, air-to-air heat pumps distribute warmed air through air handling units in designated rooms or throughout a home via duct systems.

The up to 10 kw segment, by rated capacity, is expected to grow at the highest CAGR during the forecast period.

Based on the rated capacity segment, the heat pump water heater market is segmented into six categories: up to 10 kw, 10–20 kw, 20–30 kw, 30–100 kw, 100–150 kw, and above 150 kw. Up to 10kw is expected to be the fastest growing segment during the forecast period. Heat pump water heaters up to 10 kW are commonly used for water heating due to their suitability for residential and light commercial applications. These heat pumps are efficient and can meet the hot water demands of typical households and small businesses. Additionally, they are often well-suited for integration with standard electrical systems, making them a practical choice for many water heating applications.

Europe is expected to be the fastest-growing region in the heat pump water heater market.

Europe is expected to be the fastest-growing region in the heat pump water heater market during the forecast period. The European region comprises major economies such as Germany, Italy, France and others. The surging demand for energy-efficient solutions in both commercial and residential sectors, coupled with a strategic shift towards replacing existing heating systems to curb carbon emissions, has significantly boosted the growth of the industry in Europe. The diverse climatic conditions prevalent across European countries, influenced by escalating pollution levels and the impact of global warming, have driven an increased need for advanced technological systems. Given Europe's varied climate, heat pump water heaters have emerged as a practical and favored choice for numerous households and businesses. European governments actively promote the adoption of heat pump water heaters through diverse support mechanisms and incentives. Notably, France's "My Electricity" program provides grants of up to €1,060 for air-source heat and domestic hot water heat pumps when integrated with a PV system. In Ireland, incentives include €3,500 for air-to-air heat pumps across all house types and €4,500 for air-to-water and ground-source heat pumps.

Some of the major players in the heat pump water heater market are Panasonic Corporation (Japan), LG Electronics (South Korea), Johnson Controls–Hitachi Air Conditioning (Japan), Mitsubishi Electric Corporation (Japan), Trane Technologies plc (Ireland). The major strategies adopted by these players include new product launches, acquisitions, contracts, agreements, partnerships, joint ventures, collaborations, investments, and expansions.

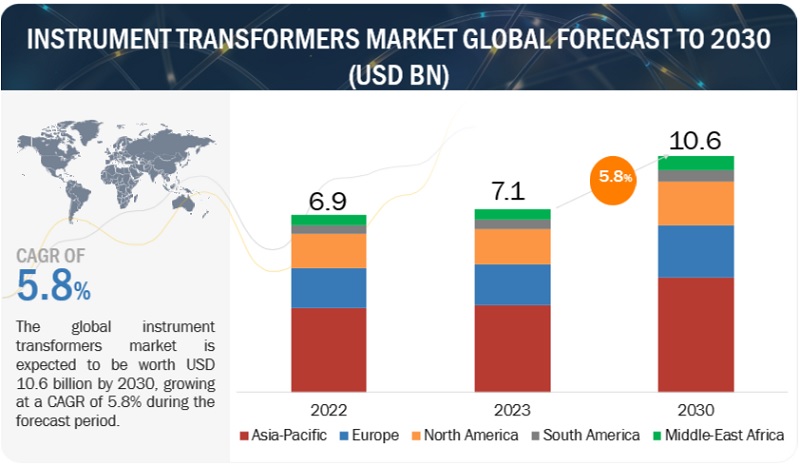

The global Instrument Transformers Marketis expected to reach USD 10.6 billion by 2030 from USD 7.1 billion in 2023 at a CAGR of 5.8% during the 2023–2030 period according to a new report by MarketsandMarkets™. The Instrument Transformers Market is poised for substantial growth during this period, primarily due to the development of power distribution infrastructure in response to the growing demand for electricity. Furthermore, the expansion of renewable energy-based capacity, increased investments in industrial production, and government initiatives for grid modernization are likely to drive the demand for instrument transformers.

Current transformers segment, by type, to occupy the majority of instrument transformers market share.

Current transformers occupy 48.7% of the market share for the year 2023. Current transformers are widely used in a variety of industries, including electricity utilities and commercial facilities. Their adaptability makes them ideal for measuring and monitoring electrical currents in a variety of environments. Current transformers are critical components of power systems for monitoring and controlling the grid. They precisely monitor current flow, giving critical information for analyzing the health and operation of the electrical grid. This skill is critical for keeping the grid stable and avoiding interruptions. Current transformers improve power quality by monitoring and adjusting current levels. Maintaining the quality of electrical power is critical for the efficient and dependable functioning of electrical systems. These are the potential reasons that are propelling the growth of current transformers in the market.

Outdoor segment, by enclosure type, to be the largest market.

Outdoor transformers are built to survive severe temperatures, humidity, and exposure to the weather. Because of their robustness, they can be deployed outside without reducing performance. These transformers are easier to construct than indoor transformers since they don't require specific interior infrastructure. This simplicity of installation helps to faster deployment and less downtime throughout the installation process. The external enclosure style allows for greater flexibility in grid layout and extension. These transformers are strategically deployed around the system to improve scalability and responsiveness to changing power distribution needs.

Asia Pacific to emerge as the largest instrument transformers market.

Ongoing enhancements in instrument transformer technologies improve their performance, reliability, and efficiency, drawing acceptance in the Asia Pacific market for updated power infrastructure. The growing use of renewable energy sources demands the use of modern instrument transformers to handle the various and intermittent nature of renewable power generation. China is the largest market for Asia-Pacific transformers, followed by India and Japan, due to increased power consumption and the construction and connection of renewable energy sources to the country's grid.

Key players in the global instrument transformers market include ABB (Switzerland), General Electric (US), Siemens (Germany), Schneider Electric (France), and Mitsubishi Electric (Japan).

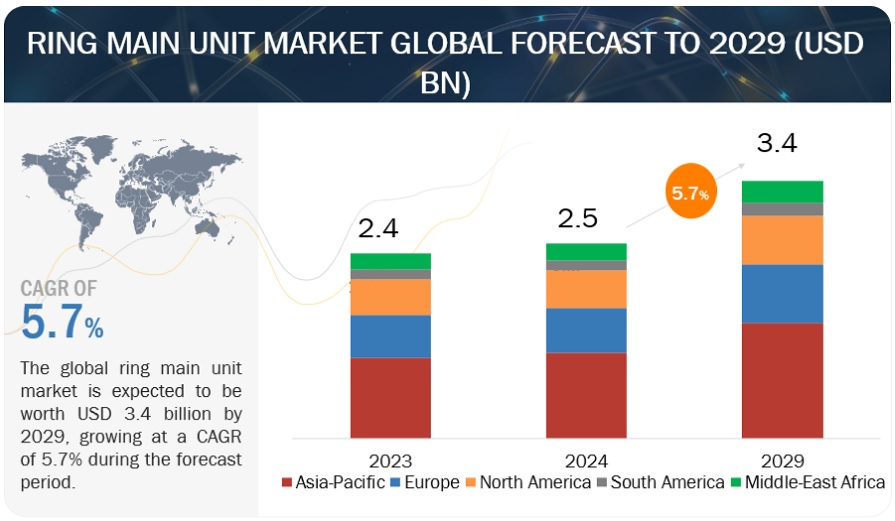

According to a research report "Ring Main Unit Market by Insulation Type (Gas-insulated, Air-insulated, Oil-insulated, Solid Dielectric), Voltage Rating (Up to 15 kV, 16-25 kV, Above 25 kV), Installation (Indoor, Outdoor), Structure, Application, Region - Global Forecast to 2029" published by MarketsandMarkets, The market for ring main units is anticipated to grow significantly; estimates place it at USD 2.5 billion in 2024 and predict it will reach USD 3.4 billion by 2029, a Compound Annual Growth Rate (CAGR) of 5.7%. The growth of the market can be primarily attributed to the expanding capacity of renewable energy sources and the ongoing efforts to enhance distribution networks, coupled with the modernization initiatives aimed at upgrading existing power infrastructure. As countries worldwide intensify their focus on sustainable energy solutions, there is a notable surge in the installation of renewable energy capacity, such as solar and wind power. This trend necessitates the integration of advanced technologies like ring main units (RMUs) to facilitate the seamless integration of renewable energy into the grid. Furthermore, the increasing complexity of distribution networks and the aging of existing power infrastructure prompt utilities to invest in modernization projects. These initiatives involve the deployment of state-of-the-art equipment like RMUs, which offer enhanced reliability, efficiency, and flexibility in managing electricity distribution.

The non-extensible segment, by structure type, is expected to be the most significant ring main unit segment during the forecast period.

The non-extensible segment is projected to emerge as the most significant segment in the ring main unit (RMU) market during the forecast period due to several factors. Non-extensible RMUs offer fixed configurations that are well-suited for specific applications and environments, providing reliability and stability in power distribution systems. These units are favored for their simplicity and robustness, requiring minimal maintenance and offering long-term operational efficiency. Additionally, non-extensible RMUs are often preferred for critical infrastructure applications where customization and flexibility are less prioritized compared to reliability and durability. As a result, the demand for non-extensible RMUs is expected to remain strong across various industries and utility networks, driving the segment's prominence in the RMU market.

The commercial building segment is anticipated to be the second-largest ring main unit segment, by application, during the forecast period.

The commercial building segment is poised to become the second-largest segment in the ring main unit (RMU) market by application during the forecast period due to several key factors. Firstly, commercial buildings, including office complexes, shopping malls, hotels, and educational institutions, require reliable and uninterrupted electricity supply to support their operations effectively. RMUs play a crucial role in ensuring the stability and resilience of power distribution within these facilities, especially during peak demand periods. Additionally, as commercial buildings increasingly adopt energy-efficient technologies and integrate renewable energy sources, the need for advanced electrical infrastructure, including RMUs, becomes paramount. RMUs enable efficient management of electricity distribution, optimizing energy usage and reducing operational costs for commercial building owners and operators. Moreover, the growing emphasis on building automation and smart technologies in commercial real estate drives the demand for RMUs with integrated smart grid capabilities, allowing for remote monitoring and control of electrical systems. As urbanization and economic development continue to drive the construction of commercial buildings globally, the demand for RMUs in this segment is expected to witness significant growth, contributing to its prominence in the RMU market landscape.

The air-insulated segment is anticipated to be the fastest-growing ring main unit segment, by insulation type, during the forecast period.

The air-insulated segment is poised to emerge as the fastest-growing segment in the ring main unit (RMU) market by insulation type, primarily due to several key advantages it offers. Firstly, air-insulated RMUs are renowned for their simplicity and reliability, as they do not rely on specialized insulating gases like SF6, making them more environmentally friendly and cost-effective. Additionally, air-insulated RMUs require minimal maintenance compared to gas-insulated counterparts, reducing operational expenses and downtime for utilities. Moreover, the modular design of air-insulated RMUs allows for easy expansion and scalability, making them well-suited for evolving distribution networks and urban environments where space constraints may be a concern. Furthermore, advancements in insulation materials and design technologies have enhanced the performance and reliability of air-insulated RMUs, further driving their adoption. As utilities increasingly prioritize sustainability, efficiency, and cost-effectiveness in their distribution networks, the air-insulated segment is expected to witness accelerated growth, cementing its position as a dominant force in the RMU market.

Asia Pacific is expected to be the fastest-growing segment in the global ring main unit market, by region, during the forecast period.

Asia Pacific is poised to emerge as the fastest-growing segment in the global ring main unit (RMU) market during the forecast period due to several compelling factors. Firstly, the region is witnessing rapid economic growth and industrialization, leading to a surge in electricity demand across various sectors such as manufacturing, infrastructure development, and commercial establishments. This escalating demand necessitates the expansion and modernization of power distribution networks, wherein RMUs play a pivotal role in ensuring efficient and reliable electricity supply. Moreover, governments in Asia Pacific are increasingly investing in infrastructure development projects, including the enhancement of electrical grids, to support economic growth and meet the needs of growing populations. Additionally, the region's commitment to renewable energy adoption, driven by environmental concerns and energy security, fuels the demand for RMUs for integrating renewable energy sources into the grid. Furthermore, initiatives aimed at rural electrification and improving energy access contribute significantly to the growing deployment of RMUs across diverse geographical and socioeconomic landscapes in the region. The convergence of these factors positions Asia Pacific as a key market for RMUs, with substantial growth opportunities both in terms of market size and expansion rate in the coming years.

ABB Ltd. (Switzerland), Siemens (Germany), Eaton (Ireland), Schneider Electric (France), and LS Electric Co., Ltd. (South Korea), Lucy Electric (UK), CG power & industrial solutions (India), Tiepco (Saudi Arabia), Orecco (China), Entec Electric & Electronics (South Korea) are major competitors in the global ring main unit market.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

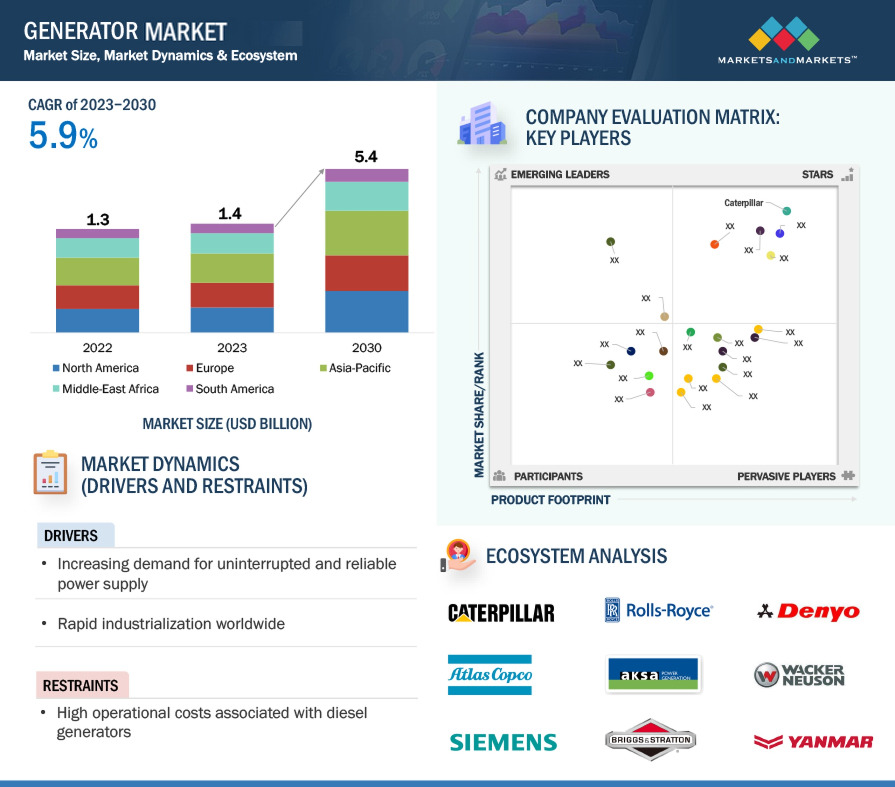

According to a research report "Generator Market by Fuel Type (Diesel, Gas, LPG, biofuels), Power Rating (Up to 50 kW, 51–280 kW, 281-500 kW, 501-2000 kW, 2001-3500 kW, Above 3500 kW), Application, End-User Industry, Design, Sales Channel, Region - Global Forecast to 2030" published by MarketsandMarkets, the global generator market is projected to reach USD 34.5 billion by 2030 from an estimated USD 23.1 billion in 2023, at a CAGR of 5.9% during the forecast period.

Generators are devices that convert mechanical energy into electrical energy. They consist of an engine or motor that drives a rotor, which creates a rotating magnetic field. This field induces an electric current in the stator windings, producing usable electrical power for various applications, such as providing backup power during outages.

Commercial, by end-user industry, is expected be the largest market during the forecast period.

Based on end-user industry, the generator market has been split into commercial, residential, industrial. Commercial end users include IT & telecom, healthcare, data centers, and others. Other commercial end users include hotels, shopping complexes, malls, and public infrastructure. Blackouts in commercial premises can lead to huge financial losses and safety issues. Also, it is challenging for IT and other commercial end users to conduct smooth operations during peak hours and in remote locations using power grids. Generators indirectly protect business interests and revenues by running operations smoothly and avoiding losses. These benefits is driving the market for commercial segment.

The direct segment, by sales channel is expected to be the fastest segment during the forecast period

Companies offering generators directly to end users or EPC contractors in different regions are considered under the direct sales segment. This mode eliminates the intermediaries involved in product distribution and helps avoid expensive overheads and reduce advertising costs. This advantage is driving the segment to the fastest market.

North America is expected to be the second largest region in the Generator market

North America is expected to be the second largest generator market during the forecast period. Extensive LNG projects and growing investments in manufacturing and chemicals & petrochemicals industries are the primary drivers of the market in this region. Due to its large-scale industrial sector and the world’s highest per capita energy consumption, the region has tremendous energy requirements. This is creating demand for the generators in the market.

Some of the major players in the generator market are Caterpillar Inc. (US), Cummins Inc. (US), Rolls-Royce Holdings plc (UK), Generac Holdings Inc. (US), Mitsubishi Heavy Industries, Ltd. (Japan). The major strategies adopted by these players include acquisitions, sales contracts, product launches, partnerships, and expansions.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

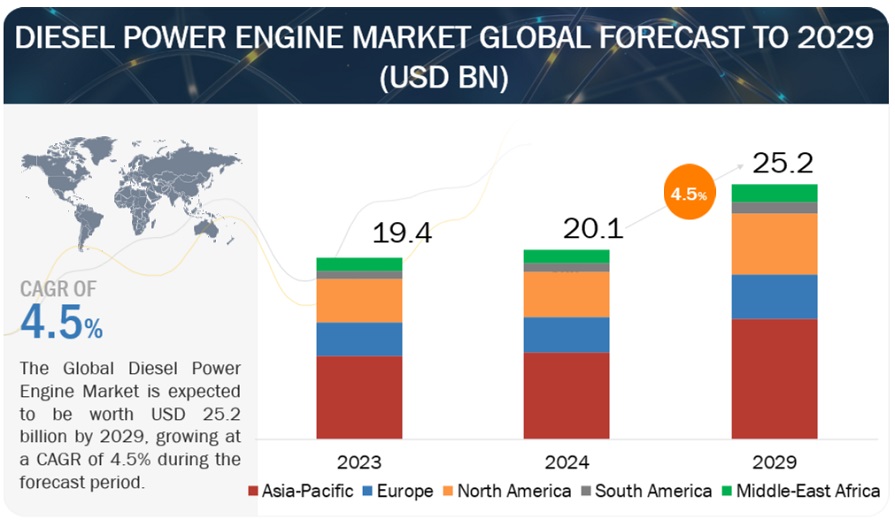

According to a research report "Diesel Power Engine Market by Operation (Standby, Prime, Peak Shaving), Power Rating (Below 0.5 MW, 0.5–1 MW, 1–2 MW, 2–5 MW, and Above 5 MW), End User (Power Utilities, Industrial, Commercial, and Residential), Speed, & Region - Global Forecast to 2029" published by MarketsandMarkets, the market size for diesel power engine is projected to reach approximately USD 25.2 billion by the year 2029, as compared to the estimated value of USD 20.1 billion in 2024, at a Compound Annual Growth Rate (CAGR) of 4.5% over the forecast period. The global diesel power engine market is driven by a confluence of factors that influence demand and shape its future trajectory. Rapid economic growth in regions like Asia Pacific, Africa, and South America fuels the need for reliable power sources. Diesel engines play a crucial role, particularly in areas with limited grid infrastructure or frequent outages. They provide primary or backup power for businesses, industries, and communities, enabling uninterrupted operations and fostering economic development. As economies expand, industrial activity and urbanization accelerate. These sectors heavily rely on diesel engines for power generation, both for primary use and backup during grid disruptions. Reliable power ensures smooth operation of factories, construction sites, and commercial facilities. Governments worldwide are implementing stricter emission regulations to combat air pollution. This drives advancements in cleaner burning diesel engine technologies.

Manufacturers are developing engines with lower NOx and particulate matter emissions, ensuring compliance with regulations and reducing environmental impact. The market is exploring alternative fuel options like biodiesel or biofuels derived from renewable sources. This allows diesel engines to contribute to a more sustainable energy mix while maintaining their reliability and power output. The integration of renewable energy sources like solar and wind power into the grid is increasing. However, these sources are intermittent. Diesel engines can act as a balancing mechanism, providing backup power during periods of low renewable energy generation and stabilizing grid frequency. Combining diesel engines with renewable energy sources in hybrid power plants offers a promising solution. Renewable energy provides primary power when available, while diesel engines take over during peak demand periods or outages, ensuring a reliable and efficient power supply. These drivers, along with factors like fluctuating fuel prices and advancements in alternative energy technologies, will continue to shape the global diesel power engine market. Manufacturers that prioritize cleaner technologies, efficient engines, and adaptability to changing energy landscapes will be well-positioned to capitalize on future growth opportunities.

Commercial segment, by End User, to hold the third-largest market in diesel power engine market.

The commercial segment secures the third-largest market share within the diesel power engine market by end user segment, driven by several key factors. Modern businesses rely heavily on electricity for various functions like lighting, communication systems, data processing, and security. Outages can cause significant disruptions and revenue losses. The commercial segment utilizes diesel generators as a reliable backup power source to ensure business continuity during grid disruptions. Hospitals, data centers, airports, and other critical infrastructure require uninterrupted power supply. Commercial-grade diesel generators provide a reliable backup solution for these facilities, protecting essential services from outages. Businesses located in areas with unreliable grid infrastructure or those seeking greater energy independence might invest in microgrids powered by diesel generators. These microgrids provide a reliable and localized power source, offering greater control and potentially lower energy costs. The construction industry relies on temporary power solutions like diesel generators to power equipment and facilities at remote job sites. Similarly, businesses with off-grid operations, like telecom towers or mining sites, utilize diesel engines for primary power generation. Hotels, shopping malls, and other commercial establishments utilize diesel generators to ensure continued operations during power outages. Maintaining comfortable temperatures, lighting, and electronic systems is crucial for customer satisfaction and security. Warehouses and cold storage facilities require consistent temperature control to ensure product quality. Diesel generators provide backup power to maintain refrigeration systems and prevent spoilage during outages. While renewable energy solutions like solar panels are gaining traction, they often require a higher initial investment. For businesses with tight budgets, diesel generators offer a more cost-effective option for backup or temporary power needs. Diesel generators can be deployed quickly and scaled to meet specific power requirements. This flexibility is crucial for businesses requiring temporary power or those with fluctuating power demands.

2-5 MW segment, by Power Rating, to be the third-largest market segment.

The 2-5 MW segment by power rating holds the third-largest market share in the global diesel power engine market due to its ideal capacity to bridge the gap between smaller-scale applications and large-scale industrial needs. This segment is highly valued for its versatility, efficiency, and ability to meet a diverse range of power requirements across various sectors. One of the primary reasons for the prominence of the 2-5 MW power rating segment is its suitability for medium to large-scale power generation applications. These diesel engines are commonly used in industries such as manufacturing, commercial facilities, hospitals, and data centers, where there is a need for reliable and continuous power supply. The 2-5 MW engines provide sufficient power to support critical operations and ensure operational continuity during power outages or in areas with unreliable grid power. Their ability to deliver a stable and robust power output makes them an essential component for prime and standby power generation solutions. In addition to their application in power generation, the 2-5 MW diesel engines are extensively utilized in the oil and gas industry. In this sector, they are often deployed for drilling operations, offshore platforms, and other energy-intensive processes that require dependable power sources. The harsh and remote environments associated with oil and gas exploration and production necessitate power solutions that are both robust and efficient. Diesel engines in the 2-5 MW range are well-suited for these conditions, providing the necessary power while maintaining operational reliability.

The 2-5 MW segment is favored for its balance between cost and performance. These engines offer a cost-effective solution for applications that require more power than smaller engines can provide but do not necessitate the higher capital and operational expenditures associated with larger engines. This cost-effectiveness extends to fuel consumption as well, where engines in this power rating range are designed to optimize fuel efficiency, resulting in lower operating costs over time. This makes them an attractive option for businesses looking to manage their energy expenses without compromising on power availability. The construction and infrastructure sectors also drive the demand for 2-5 MW diesel engines. Construction sites often require mobile and reliable power sources to operate heavy machinery, lighting, and other essential equipment. Diesel generators in this power rating are portable enough to be transported to different sites while powerful enough to meet the high energy demands of large construction projects. Their ability to provide consistent power in off-grid and remote locations makes them indispensable for large-scale construction and infrastructure development. Additionally, advancements in diesel engine technology have bolstered the market position of the 2-5 MW segment. Manufacturers are continually innovating to enhance the performance, emissions control, and efficiency of these engines. Modern engines in this power rating range feature advanced fuel injection systems, improved combustion processes, and sophisticated control mechanisms that reduce emissions and comply with stringent environmental regulations. These technological improvements not only increase the attractiveness of 2-5 MW diesel engines but also ensure their competitiveness in a market that increasingly values sustainability and environmental responsibility.

Middle East & Africa to emerge as the third-largest diesel power engine market.

The Middle East & Africa region holds the fourth-largest market share in the global diesel power engine market due to a combination of factors that drive demand across various sectors, including energy, construction, mining, and manufacturing. Firstly, the Middle East's robust oil and gas industry is a significant contributor to the demand for diesel power engines. Countries like Saudi Arabia, the UAE, and Kuwait rely heavily on diesel engines to power drilling rigs, pump stations, and other critical infrastructure in remote locations where access to the grid is limited. The need for reliable and continuous power in these operations ensures a steady demand for diesel power engines, particularly in mid-to-large power ratings. In Africa, the widespread lack of reliable grid infrastructure drives the demand for diesel power engines as primary and backup power sources. Many African countries face frequent power outages and have limited access to consistent electricity supply. Diesel generators provide an essential solution for businesses, hospitals, and residential areas to ensure uninterrupted power. This is particularly crucial for sectors like healthcare and telecommunications, where power reliability is paramount. The construction boom in the Middle East, driven by massive infrastructure projects and urban development initiatives, also fuels the demand for diesel power engines. Major cities like Dubai and Riyadh are continuously expanding, requiring substantial power for construction machinery, site lighting, and other temporary power needs. Diesel engines are favored in these scenarios due to their portability, robustness, and ability to deliver high power output in varying environmental conditions.

Mining activities across Africa, particularly in countries such as South Africa, Nigeria, and Ghana, further boost the market for diesel power engines. The mining industry operates in remote areas with little to no access to grid power, making diesel engines indispensable for powering mining equipment, ventilation systems, and processing plants. The reliability and durability of diesel engines make them the preferred choice in the harsh operating conditions typical of mining sites. Moreover, the region's ongoing industrialization and urbanization trends are key drivers of diesel engine demand. As Middle Eastern and African countries continue to develop their industrial base, the need for reliable power solutions increases. Diesel engines play a critical role in supporting manufacturing operations, logistics, and agricultural activities by providing a dependable source of power, especially in areas where the electrical grid is underdeveloped or unstable. Government initiatives aimed at improving energy access and infrastructure also play a role in sustaining demand for diesel power engines. Many countries in the region are investing in expanding their energy infrastructure, including the deployment of diesel generators as a stopgap solution while longer-term projects like renewable energy installations are developed. Lastly, the adaptability of diesel engines to operate in diverse climatic conditions found across the Middle East and Africa, from the arid deserts of the Middle East to the tropical regions of Sub-Saharan Africa, underscores their utility and widespread adoption. Manufacturers in the region have also been focusing on developing engines that comply with stringent emission standards, enhancing their market appeal by addressing environmental concerns.

Key players in the global diesel power engine market include Caterpillar (US), Cummins Inc. (US), WEICHAI POWER CO.,LTD (China), MAN (Germany), Rolls-Royce plc (UK), MITSUBISHI HEAVY INDUSTRIES, LTD. (Japan), HD HYUNDAI INFRACORE (South Korea), DAIHATSU DIESEL MFG. CO., LTD. (Japan), YANMAR HOLDINGS CO., LTD. (Japan), KUBOTA Corporation (Japan), Kohler Energy (US), AB Volvo Penta (Sweden), DEUTZ AG (Germany), Mahindra&Mahindra Ltd. (India), IHI Power Systems Co.,Ltd (Japan), Guangzhou diesel engine factory Limited (China), and Wabtec Corporation (US).

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

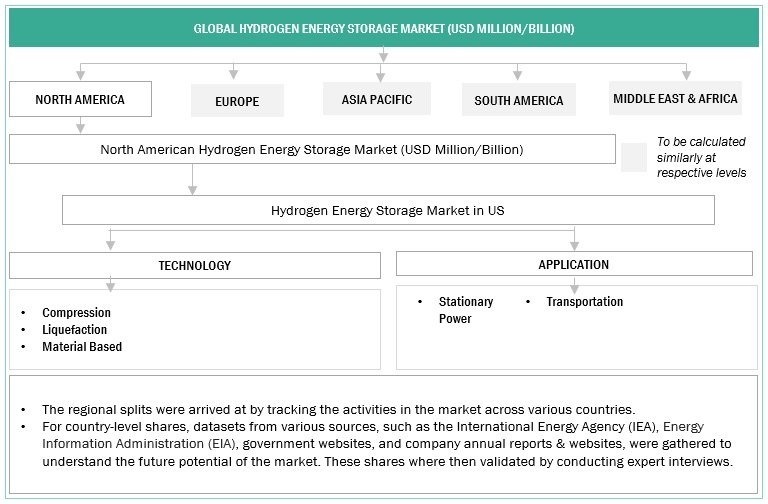

The global hydrogen energy storage market is projected to reach USD 196.8 billion by 2028 from an estimated USD 11.4 billion in 2023, at a CAGR of 76.8% during the forecast period. The growing emphasis on environmental sustainability, rising adoption of fuel cell vehicles, intermittent renewable energy integration accelerates the growth of the hydrogen energy storage market.

Key Market Players

Linde plc (Ireland), ENGIE (France), Plug Power Inc. (US), Fuelcell Energy, Inc. (US), Iwatani Corporation (Japan), Hydro X (Israel), LAVO System (Australia), HYDROGEN IN MOTION (Canada), Mahytec (France), GKN Hydrogen (Italy), HPS Home Power Solutions AG (Germany), HDF ENERGY (France), Energy Vault, Inc. (Switzerland), BALU FORGE INDUSTRIES LIMITED (India), storelectric LTD (UK), H2GO Power (UK), Powertech Labs Inc. (Canada), Beijing SinoHy Energy Co., Ltd. (China), Hydrogenious LOHC Technologies (Germany), Ergenics Corp. (US), Power to hydrogen (US)

This report segments the hydrogen energy storage market based on application into three categories: electric utilities, industrial, and commercial. Electric Utilities is expected to hold the largest market share in the hydrogen energy storage market during the forecast period. The demand for hydrogen energy storage is increasing in electric utilities applications due to integration of renewable energy and grid stability and reliability. Hydrogen energy storage can provide backup power during grid outages and can be used to balance supply and demand on the grid by storing excess electricity during times of low demand are the factors that are expected to drive the growth of the electric utilities segment during the forecast period.

Based on the Storage form, the hydrogen energy storage market is segmented into solid, liquid and gas. The gas segment is expected to dominate the market during the forecast period as gas form is more efficient and can easily be transported. Hydrogen energy storage as gas results in fewer energy losses during the storage process and there is already established infrastructure for transporting and distributing gaseous hydrogen energy.

Based on the technology, the hydrogen energy storage market is segmented into compression, liquefaction and material-based. The compression segment is expected to be the fastest growing market during the forecast period owing to the low energy losses compared to other methods and high energy density per unit volume. Compression technology is cost effective as compared to other storage technologies, which is expected to drive the growth of the medium voltage segment in the forecasted period.

This report segments the hydrogen energy storage market based on application into stationary power and transportation. During the forecast period, the stationary power segment holds the largest market share due to its higher efficiency, safety, and ability to provide a steady energy supply for grid integration and industrial processes. The Stationary systems are well-suited for critical facilities, sustainability goals, and avoiding transportation challenges.

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com

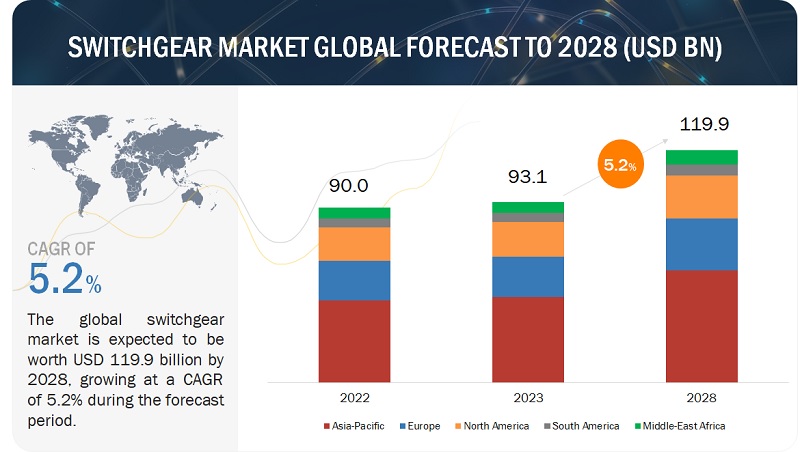

According to a research report "Switchgear Market by Insulation (Gas-insulated, Air-insulated), Installation (Indoor, Outdoor), Current (AC, DC), Voltage (Low (up to 1 kV), Medium (2-36 kV), High (Above 36 kV), End User and Region - Global Forecast to 2028" published by MarketsandMarkets, the market size for switchgear is projected to reach approximately USD 119.9 billion by the year 2028, as compared to the estimated value of USD 93.1 billion in 2023, at a Compound Annual Growth Rate (CAGR) of 5.2% over the forecast period.

The switchgear market is poised for substantial growth during this period, primarily due to the development of power distribution infrastructure in response to the growing demand for electricity. Furthermore, the expansion of renewable energy-based capacity and increased investments in industrial production are likely to drive the demand for switchgear.

High voltage segment, by voltage, to occupy majority of switchgear market share.

During the forecast period, the high voltage segment, categorized by voltage, is expected to secure a dominant market share. High-voltage switchgears, operating above 36 kV, are crucial in transmission, heavy industries, mining, railways, and commercial infrastructures. The main component, a high-voltage circuit breaker, is integral. Gas-insulated switchgears are prevalent in these applications. Typically placed outdoors due to space requirements, they consist of circuit breakers, isolators, transformers, and bus bars. Faulty tripping is rare, and these switchgears often remain ON for extended periods. They play a vital role in renewable power transmission and medium-voltage substations. As electrification and renewable integration rise, the demand for high-voltage switchgear, especially automated and smart ones for smart grids, is expected to surge in the forecasted period.

Commercial & residential segment, by end user, to be third-largest and third-fastest market.

Urbanization, particularly in regions like Asia Pacific, South America, and Africa, is driving a surge in commercial and residential constructions. As urban centers grow due to economic opportunities, the need for housing and commercial buildings escalates. Switchgear plays a vital role in supplying, safeguarding, and regulating power for various equipment in these constructions. Additionally, contemporary switchgears are engineered to handle earth leakage current faults, enhancing their safety features. Consequently, the demand for switchgear in commercial and residential applications is anticipated to rise significantly in the coming years.

North America to emerge as the third-largest switchgear market.

During the forecast period, North America is anticipated to hold the third-largest market share in the global switchgear market. Encompassing the US, Canada, and Mexico, the region boasts extensive trade ties and significant foreign investments, with the US and Canada jointly contributing around 93.8% to North America's switchgear market. With a combined population of nearly 530 million and an economy representing over one-quarter of the world's GDP, the region faces substantial power demands, leading to increased investments in fortifying and modernizing its transmission and distribution utilities. Notably, energy consumption per capita in North America saw a 4% rise, according to the BP Statistical Review of World Energy 2022.

The region is undergoing a transformative phase in its utilities sector, marked by a shift towards digital operational strategies focusing on decentralization, digitization, and decarbonization of power systems. Aging power infrastructures, constituting nearly 72% of the US power infrastructure beyond 25 years of service, pose a blackout risk, prompting active government initiatives to upgrade and replace these structures for enhanced grid reliability.

Key players in the global switchgear market include ABB (Switzerland), General Electric (US), Siemens (Germany), Schneider Electric (France), and Eaton (Ireland).

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America's best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines - TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the 'GIVE Growth' principle, we work with several Forbes Global 2000 B2B companies - helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Contact: Mr. Rohan Salgarkar MarketsandMarkets™ INC. 630 Dundee Road Suite 430 Northbrook, IL 60062 USA: +1-888-600-6441 Email: newsletter@marketsandmarkets.com