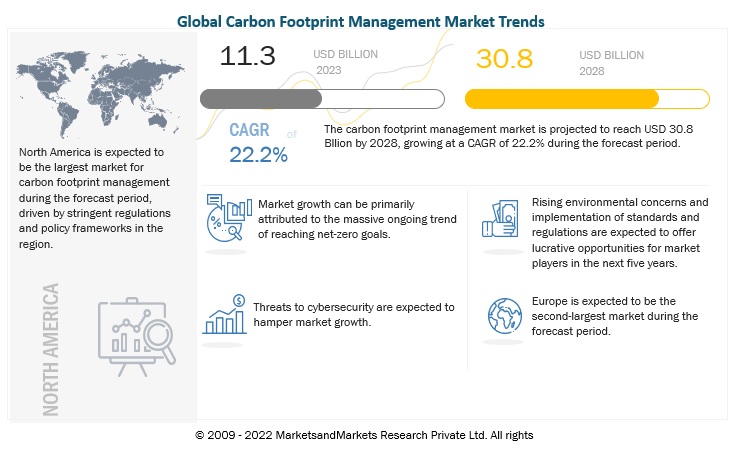

The global carbon footprint management market is projected to reach USD 30.8 Billion by 2028 from an estimated USD 11.3 Billion in 2023, at a CAGR of 22.2% during the forecast period. An environmental indicator, carbon footprint represents the total amount of greenhouse gas emissions caused by an individual, event, organization, service, place, or product. The global market for carbon footprint management is expanding as a result of rising demand for energy by industries, and increasing initiatives to reduce carbon emissions from the governments. Moreover, the stricter implementation of COP27 targets to limit global warming around the world i also boosting the demand for carbon footprint management software.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=136375712

The carbon footprint management market, by deployment mode, is segmented into on-premise and cloud. The market for carbon footprint management of deployment mode cloud is expected to be the largest during the forecast period. Implementing cloud technology has advantages such as lower operating expenses, security and better project management costs.

The carbon footprint management market, by component, is divided into solutions and services. The services segment of the carbon footprint management market is projected to register the highest growth rate during the forecast period. Services like consulting, integration and deployment, as well as support and maintenance are crucial segments in carbon footprint management. Technical expertise is often lacked by many firms and companies in the carbon footprint management and hence there is an increasing need for professional service providers.

By organization size, the carbon footprint management market is corporates/enterprises, mid-tier enterprises, and small businesses. The corporates/enterprises segment is expected to be the largest owing to the large sizes of company facilities and an increased pressure from stakeholders for emissions disclosure. Governments of various countries and environment protection bodies closely monitor carbon emissions of these enterprises and their compliance with norms, making it necessary for them to use tools like carbon footprint management software for accounting, disclosure, and mitigation of carbon emissions.

The carbon footprint management market, by vertical, is segmented into manufacturing, energy & utilities, residential & commercial buildings, transportation & logistics, IT & telecom, financial services, and government. The financial services segment is expected to be the fastest growing segment during the forecast period. The GHG emissions associated with financial institutions' investing, lending, and underwriting activities, i.e., their scope 3 emissions, are on average over 700 times higher than their direct emissions. Given the growing momentum of financial institutions announcing net zero targets, the sector is expected take further action to align portfolios with a net zero carbon economy.

Request Sample Pages of the Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=136375712

North America is estimated to be the largest regional market for carbon footprint management during the forecast period. North America includes US, Canada, and Mexico. Increasing pressure to achieve NDC target, federal/national laws on ESG disclosure, and emphasis on sector-specific measures for carbon reduction is expected to aid the fast growth of the carbon footprint management market in this region.

Browse Related Reports:

Carbon Credit Validation Verification and Certification Market by Type (Voluntary, Compliance), Service (Validation, Verification, Certification), End User (Energy & Utilities, Agriculture & Forestry, Industrial) & Region - Global Forecast to 2030

Carbon Credit Trading Platform Market by Type (Voluntary, Regulated), System Type (Cap and Trade, Baseline and Credit), End Use (Industrial, Utilities, Energy, Petrochemical, Aviation) and Region - Global Forecast to 2027

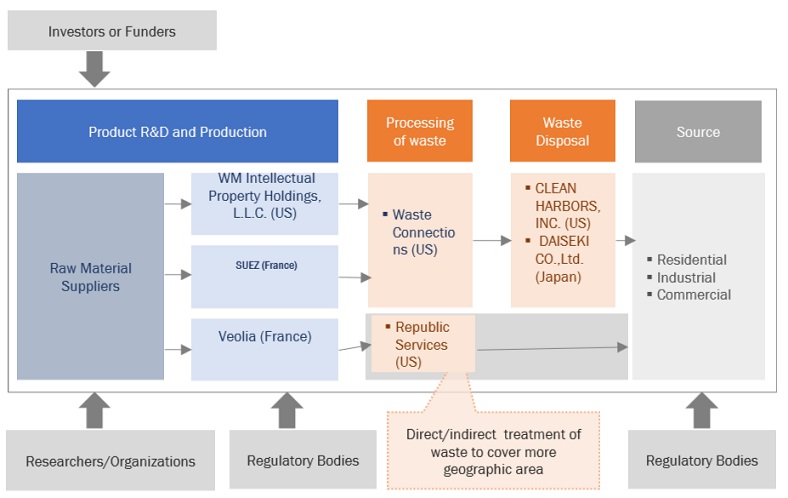

Waste Management Market by Waste Type (Hazardous Waste, E-Waste, Municipal Solid Waste, Medical Waste, Construction & Demolition, Non-Hazardous Industrial Waste), Disposal (Open Dumping, Incineration/Combustionl), Source & Region - Global Forecast to 2029

About MarketsandMarkets™

MarketsandMarkets™ has been recently recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

Founded in 2009, MarketsandMarkets recognized uncharted business potentials within disruptive trends, forecasting a surge of $25 trillion in new B2B revenues by 2030. In our 13-year journey, we've collaborated with over 10,000 companies, generating $140+ billion in revenue impact. From a market research publisher, we've transformed into a growth-enabling leader, backed by a 1500+ strong team.

Contact:

Mr. Rohan Salgarkar

MarketsandMarkets™ INC.

630 Dundee Road, Suite 430

Northbrook, Illinois - 60062

USA : 1-888-600-6441

UK +44-800-368-9399