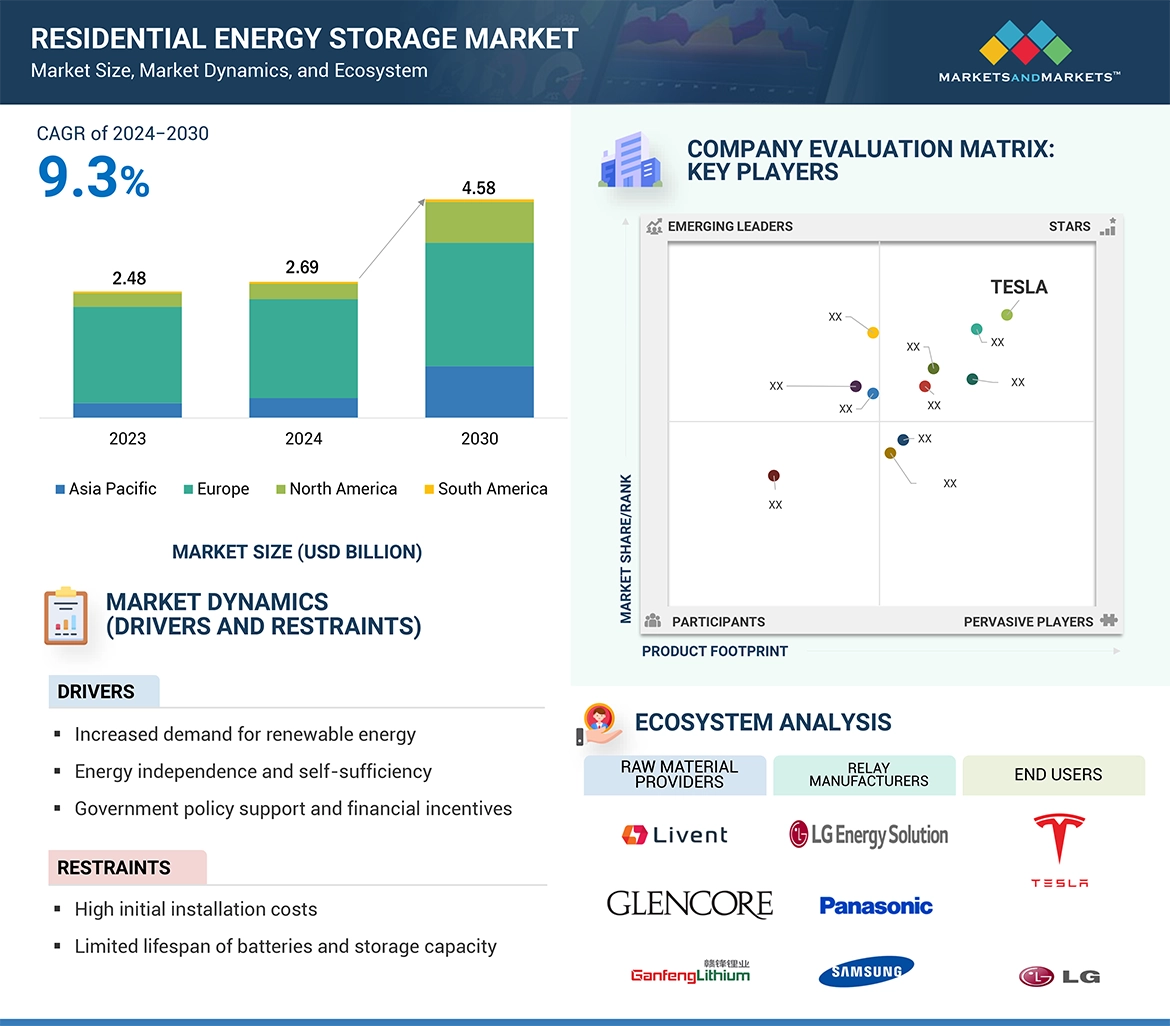

The global Residential Energy Storage Market is anticipated to grow from estimated USD 2.67 billion in 2024 to USD 4.30 billion by 2030, at a CAGR of 8.2% during the forecast period. Rapid developments in battery technologies, especially in lithium-ion systems, have led to cost decline at levels that see energy storage systems increasingly come closer to the residential customer. Improvements in manufacturing processes as well as an economy of scale combined with growing competition in the energy storage industry mainly contributed to the cost decrease. Thus, what is previously too expensive for most consumers was possible for homeowners to invest in and hence more widely adopted. In addition, modern batteries have better energy density, longer lifespans, and more efficiency, pushing their cost-effectiveness toward households in terms of reliable, long-term energy-demand management. This pattern serves to promote a systematic transition toward sustainable energy systems while also promoting the integration of renewable sources, such as solar power, into housing energy frameworks.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=153284325

Customer owned, by ownership type

Rising grid electricity tariffs have made household energy expenses scale, compelling homeowners to seek low-cost alternatives. Residential energy storage systems serve as a useful solution whereby users can store energy when prices are low and use them during peak hours when the prices are relatively higher. Energy storage also reduces the dependence of this power on utility companies thereby cushioning the homeowner against the continual fluctuation of energy prices. This would hold particularly true in regions with dynamic pricing models or where high energy costs are experienced, where the economic benefits of self-sufficiency become more pronounced.

Standalone systems, by operation type

With awareness of climate change, homeowners are increasingly motivated to minimize their reliance on fossil fuels. Energy storage systems and renewable energy sources, built solely but combined with solar and wind sources, prove very effective in reducing household carbon emissions. These systems enable homeowners to power their homes with clean, renewable energy, even in instances of low generation and high demand by holding excess energy generated during the day or favourable weather conditions. This change benefits the energy future to become more sustainable and supports the requirements for the overall environmental goals set globally and personal aspirations for sustainability besides cutting down greenhouse emissions.

Europe is expected to be the largest region during the forecast period.

Rising electricity prices in the European region have provided a strong economic motivation for homeowners to seek residential energy storage solutions. With this typical growth and increase in energy prices, the consumers are on a lookout for solutions that can help them cushion the impact of erratic utility bills. Energy storage systems, especially when combined with solar energy production, will enable households to store excess power generated during off-peaking times and use them as needed during peak demand periods, thereby reducing their dependence on the grid. Indeed, a shift like this promises instant benefits-when it comes to savings in energy bills-but long-term financial advantages, also: by cushioning the rise in electricity costs.

Further support for the growing adoption of such systems is brought about by the promise of self-sufficiency. Households increasingly see energy storage as part of an overarching strategy to make sure that stable and affordable energy will remain when this unstable market situation prevails. Considering that energy prices are expected to maintain their levels over the next few years, the return for residential storage is becoming clearer, and thus it’s a smart move for those wishing to optimize their energy usage and minimize ongoing costs.

Key Players

Some of the major players in the Residential Energy Storage Market are Panasonic Holdings Corporation (Japan), Tesla (US), Sonnen GmbH (Germany), BYD Company Ltd. (China), and Enphase Energy (US) among others. The major strategies adopted by these players include new product launches, acquisitions, joint ventures, and expansions.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=153284325

Panasonic Holdings Corporation

Panasonic Holdings Corporation, is the industry leader in the Residential Energy Storage Market, with very advanced lithium-ion battery technology and innovative energy solutions. Its EverVolt systems come with modular scalability, smart energy management, and reliable backup power that allows households to maximize energy usage and carbon footprints. With its strong presence in the global markets of the US, Japan, and Europe, Panasonic also utilizes its worldwide partnerships and brand recognition to secure an edge in sustainable, high-quality energy storage solutions. For this reason, combined with its development plan for carbon neutrality and investments in R&D, Panasonic will continue to play a large role in the emerging need for residential energy management.

TESLA

TESLA is a leader in the Residential Energy Storage Market due to the revolutionary Powerwall system that flows smoothly with solar energy options to deliver safe, scalable, and sustainable energy storage. Building on this deep knowledge of advanced lithium-ion battery technology combined with cost efficiency at the Gigafactories, Tesla proffers high-performance solutions that are globally accessible. Advanced features like real-time energy monitoring, backup power support, and modular expandability realize the growing interest in smart and energy-independent homes focused on sustainability. One of Tesla’s strategic initiatives in boosting the adoption of widespread battery systems has been particularly successful in North America, Europe, and Australia. These markets place emphasis on renewable energy and a resilient grid. Good brand recognition for the company combined with favorable dynamics at the market place and supportive policies by the government makes the company the leader in driving renewable energy. Tesla continues to innovate in battery technologies and redefining household consumption, thus taking a strong position in the global transition to sustainable energy solutions.

BYD Company Ltd

BYD Company Ltd, is another leader in residential energy storage. The company is famous for its highly advanced lithium iron phosphate (LFP) battery technology. The company offers safe, durable, and thermally stable solutions. Its vertically integrated supply chain and modular products, such as the Battery-Box Premium series, provide scalable and cost-efficient energy storage tailored to residential needs. It has an outstanding global footprint, excellent partnerships and seam-free integrability with renewable energy systems like solar PV. Thus, BYD is better posed to maintain an edge despite growing competition and pressure on supply chains. Its focus on sustainability and innovation will ensure its pivotal role in advancing the transition of the global energy equation.

For more information, Inquire Now!