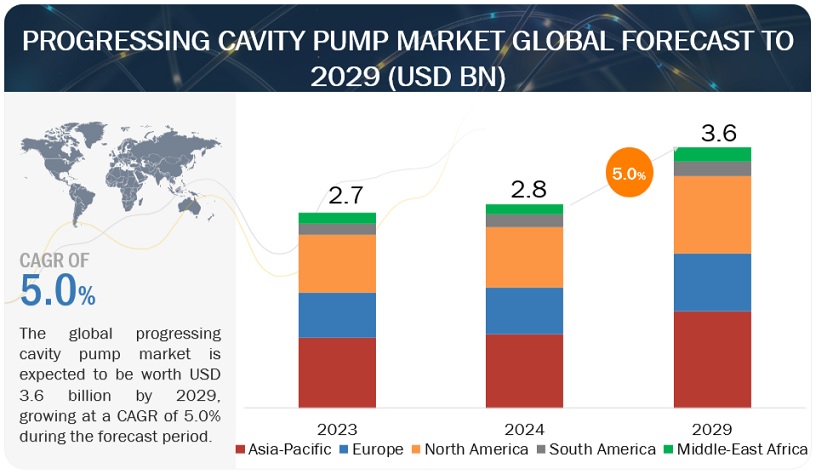

According to the new market research report “Oil Accumulator Market by Type (Bladder, Piston, and

Diaphragm), Pressure Rating (Up to 6,000 Psi and Above 6,000 Psi), Onshore vs

Offshore, Application (Blowout Preventer & Well Head Control, Offshore

Rigs, and Mud Pumps), and Region - Global Forecast to 2023”,

published by MarketsandMarkets™, the global oil

accumulator market is expected to grow at a CAGR of 4.78%, from 2018 to

2023, to reach a market size of USD 617.1 million by 2023. Digitalization in

the oil & gas industry and shale gas exploration boom in the US are

expected to drive the oil accumulator market, during the forecast period.

Browse and

in-depth TOC on "Oil Accumulator Market"

82 - Tables

31 - Figures

124 – Pages

Don’t miss out on business opportunities in Oil

Accumulator Market. Download our PDF Brochure and gain crucial industry

insights that will help your business grow:

The oil accumulator market is dominated by major players

that are established brand names with wide regional presence, along with many

local and regional players in emerging economies. The leading players in the

oil accumulator industry include Hydac (Germany), Parker Hannifin (US), Eaton

(Ireland), Freudenberg (Germany), Bosch Rexroth (Germany), and Nippon Accumulator

(Japan).

The mud pump segment is a key segment of the oil

accumulator market, by application, from 2018 to 2023. The market for this

segment is driven by increasing investments in the oil & gas industry in

developing countries of Asia Pacific and Middle East & Africa.

View more detailed

TOC @

The up to 6,000 psi segment is expected to be the fastest

growing oil accumulator market from 2018 to 2023. This is due to various

factors, including increased investments in the offshore industry. Rising

investments in the oil & gas industry is expected to drive the up to 6,000

PSI segment of the oil accumulator market.

The offshore segment of the oil accumulator market, by

onshore vs. offshore, is estimated to grow at the fastest rate from 2018 to

2023. Factors such as high investment in oil & gas industries either in top

side application or in subsea application are driving the oil accumulator

market. Most of the industries, including oil & gas, renewable, and

refineries, are using accumulators at various pressure ranges; this is driving

the high temperature oil accumulator market.

Request Sample Copy @ https://www.marketsandmarkets.com/requestsample.asp?id=84277665

The oil

accumulator market has been segmented by region into Asia Pacific, Europe,

North America, Middle East & Africa, and South America. North America is

projected to grow at the fastest rate, from 2018 to 2023, followed by Asia

Pacific and Europe. Countries such as the US and Canada are the largest markets

in North America and have increased their investments in the oil & gas

sectors in the recent past. Growing urbanization, increasing industrialization,

and increasing investment in the oil & gas industry are the major factors

impacting the growth of the oil accumulator market in this region.