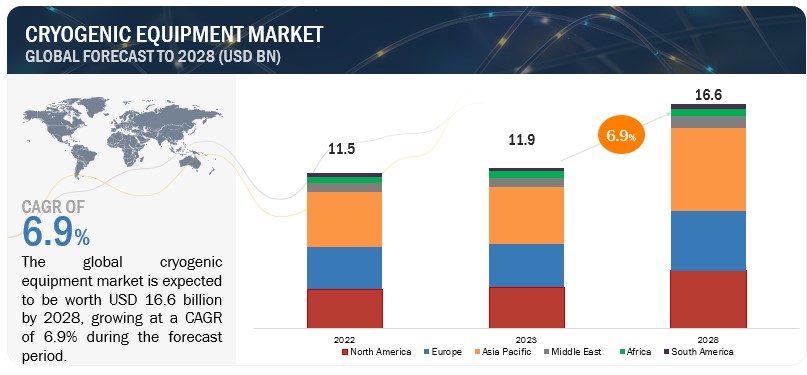

According to the market report published by

MarketsandMarkets™ “Waste

Heat Boiler Market by Temperature (Medium, High, Ultra High), Source (Oil

Engine, Gas Engine, Gas Turbine, Incinerator, Cement Plant Kiln, Steel Plant,

Glass Furnace), Orientation (Horizontal & Vertical), End-User, and Region -

Global Forecast to 2023”, The global waste heat boiler market is expected to grow at a CAGR of 6.72%, from

2018 to 2023, to reach a market size of USD 8.04 billion by 2023. The

increasing demand for energy and rising electricity prices are forcing

companies to opt for decentralized power supply which is increasing the demand

for waste heat boiler. Also, efforts to reduce GHG emissions is expected to

drive the waste heat boiler market during the forecast period.

Click To Access Full TOC of this

Report @ https://www.marketsandmarkets.com/Market-Reports/waste-heat-boiler-market-143622127.html

The waste heat boiler market is dominated by major players that are established brand names with

wide regional presence, along with many local and regional players in the

emerging economies. The global market is dominated by major

players such as General Electric (US), Siemens (Germany), Thermax (India), CMI

Group (Belgium), Amec Foster Wheeler (UK), and Nooter/Eriksen (US).

77 - Tables

28 - Figures

153- Pages

The market

growth strategies adopted by the key players in the waste heat boiler market

include contracts & agreements, mergers & acquisitions, and partnership

& collaborations. Contracts & Agreements were the most commonly adopted

strategy by market players from February 2014 to December 2018.

The industrial segment is a key segment of the waste heat

boiler market, by end-user, from 2018 to 2023. The market for this segment is driven by increasing investments in oil

& gas industry in the developing countries of Asia Pacific and Middle East & Africa. Therefore, need to

reduce carbon emissions is leading to the increased demand for cleaner sources

of power generation, which, in turn, is causing the rise in demand for waste

heat boiler that would significantly boost the efficiency of natural gas fired power plant.

Kiln and furnace gases segment is expected to grow at the

fastest rate from 2018 to 2023. Rising investments in power generation sector

and primary metal industries are expected to drive the Kiln and furnace gases

segment of the waste heat boiler market.

High temperature segment is expected to be the largest

waste heat boiler market, by waste heat temperature, in 2018.

High Temperature segment of the waste heat boiler market,

by temperature, is estimated to grow at the fastest rate from 2018 to 2023.

Factors such as high investment in primary metal industries and non-metallic

mineral industries are driving the waste heat boiler market. Most of the

process industries, including iron & steel, cement, aluminum, chemical, and

refineries, produce flue gases at a high temperature range, which is driving

the market for high temperature waste heat boilers.

Request for Sample Pages of the Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=143622127

Asia

Pacific: The largest waste heat boiler market during the forecast period.

The waste heat boiler market

has been segmented by region into Asia Pacific, Europe, North America,

Middle East & Africa, and South America. Asia

Pacific is projected to grow at the fastest rate, from 2018 to 2023, followed

by North America and Europe. Countries such as China and India are the largest

markets in Asia Pacific and have

increased their investments in the infrastructure and power sectors in the

recent past. China accounted for the maximum share in the Asia Pacific market in 2017 and is projected to

grow at the highest CAGR of 9.47%, from 2018 to 2023. Growing urbanization,

increasing industrialization, growing construction

sector, and increasing investments in oil

& gas and chemical segments are the major factors impacting the growth of

the waste heat boiler market in this region.

MarketsandMarkets™ provides quantified B2B research on 30,000 high growth

niche opportunities/threats which will impact 70% to 80% of worldwide

companies’ revenues. Currently servicing 7500 customers worldwide including 80%

of global Fortune 1000 companies as clients. Almost 75,000 top officers across

eight industries worldwide approach MarketsandMarkets™ for their painpoints

around revenues decisions.

Mr. Shelly Singh

MarketsandMarkets™ INC.

630 Dundee Road

630 Dundee Road

Suite 430

Northbrook, IL

60062

USA :

1-888-600-6441