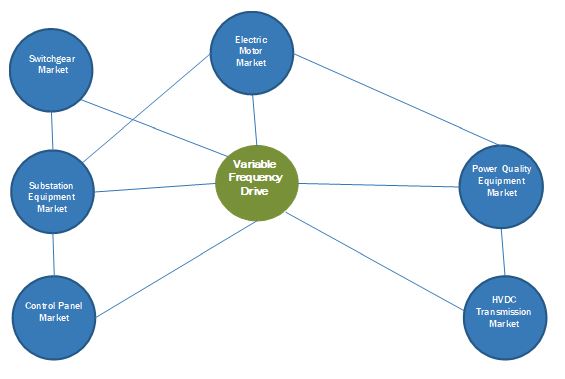

The global variable frequency drive market is estimated USD 19.2 billion in 2020 and is projected to reach USD 24.3 billion by 2025, at a CAGR of 4.8% during the forecast period. This growth can be attributed to factors such as the growth of supportive regulatory environment towards effective and efficient energy utilization, the upgradation and modernization of aging infrastructure for safe & secure electrical distribution systems, and rapid industrialization and urbanization across the globe. However, the stagnant growth of the oil & gas industry coupled with the decrease in the exploration & production activities are hindering the growth of the variable frequency drive market.

The low voltage segment is expected to hold the largest share of the variable frequency drive market, by voltage type, during the forecast period

The low voltage segment segment, by voltage, is estimated to account for the largest share during the forecast period. Low voltage variable frequency drives are used across a wide range of applications including pumps, fan, belt conveyor, centrifugal pumps, and centrifugal compressors. These drives are designed for industrial applications, especially in process industries such as pulp & paper, power, water & wastewater, and oil & gas. Thus, the increasing use of low voltage drives in a wide range of applications is expected to boost the growth for this segment

Download PDF Brochure – https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=878

The low power drive segment, by power rating, is expected account for the largest share during the forecast period

The low power drive segment is expected to hold the largest market share and is projected to grow with the highest CAGR during the forecast period. Low power drives, due to higher energy savings at low capital costs and better process control with increased motor control, offer a quick payback period. Variable frequency drives with a 6–40 kW power range are used across various industries such as building, automation, oil & gas, food & beverage, and pulp & paper. Therefore, the growing need for energy efficiency in the respective industries is expected to drive the growth of the segment.

Asia Pacific: The leading variable frequency drive market

The Asia Pacific region is estimated to be the largest and fastest growing variable frequency drive market during the forecast period. The growth of this region is primarily driven by countries such as China, South Korea, India and Japan, which are considered as the main manufacturing hubs for variable frequency drives. Countries in Asia Pacific are focused towards energy efficiency and variable frequency drives are expected to play an important role in helping these countries to meet their energy efficiency targets, as the primary function of these drivers is to save energy. Thus, The rapid industrialization due to growing automation in manufacturing sector and increased investments in renewables sector are driving the growth of the variable frequency drive market in the Asia Pacific region.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=878

The growth in industrialization is driving a continuous need for electric motors, which consume one-third of the total electricity produced globally. The factors such as limited conventional power generation and the continuous rise in electricity prices, has encouraged companies to invest in energy-efficient equipment to increase energy efficiency. Industries such as oil & gas, metals & mining, pulp & paper, cement, and water & wastewater, which are considered to be energy intensive industries, are using variable frequency drives to reduce energy consumption and CO2 emissions. Therefore, the increasing need for energy efficiency is expected to drive the growth of the variable frequency drives market.

The global variable frequency drive market is dominated by a few major players such as ABB (Switzerland), Siemens (Germany), Schneider Electric (France), Danfoss (Denmark), Rockwell Automation (US). These players have a wide regional presence.

New product launches, investments & expansions, mergers & acquisitions, contracts & agreements, partnerships, alliances, joint ventures, and collaborations are few of the key strategies adopted by the players of the variable frequency drive market. From January 2017 to December 2020, new product launches was the most commonly adopted strategy, followed by adoption of mergers & acquisitions as a major strategy during that period.

ABB is among the leading companies in the automation and power technologies businesses offering a wide range of products, solutions, services, and systems to customers in the utility, industrial, and infrastructure & transportation verticals. The company operates through 4 business segments, namely, Electrification, Robotics & Discrete Automation, Industrial Automation, and Motion. Variable frequency drives are offered through the Motion segment to utilities and industries. The Motion business segment provides products, services, and solutions that increase industrial productivity and energy efficiency. This business segment also offers products such as motors and generators for a wide range of industrial applications. ABB has its research centers in 7 countries, namely, China, Germany, India, Poland, Sweden, Switzerland, and the US. The company currently owns and operates 300 manufacturing plants and has established its operational presence in over 100 countries. The company marks a global presence—Europe, the Americas, Asia Pacific, the Middle East, and Africa. ABB has adopted both organic and inorganic business strategy to enhance its growth in the variable frequency market. For instance, in January 2019, ABB launched a series of ACS880 industrial drives and ACH580 Ultra-Low Harmonic (ULH) HVAC drives, which are used in many industries and applications to tackle harmonic issues

Request Sample Pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=878

Siemens is a major technology company with core business activities in the field of electrification, automation, and digitalization. The company operates through 6 business segments, namely, Digital Industries, Siemens Healthineers, Smart Infrastructure, Mobility, Portfolio Companies, and Financial Services. The company offers variable frequency drives through the Portfolio Companies business segment. The other products offered under this business segment are motors, synchronous condensers, integrated automation systems, electric motors, converters, generators, gear units, and couplings. The variable frequency drives offered by the company find applications in the oil & gas and power industries. Siemens has its operational presence in Europe, North America, South America, the Middle East, and Asia Pacific. Through the operation of an accomplished global network of regional offices, warehouses, R&D facilities, and sales offices, the company has established its presence in more than 100 countries across the globe. The company owns and operates factories in Sacramento, Louisville, Indiana, New Castle, Pittsburgh, Portland, and Georgia, among many other locations in the US. The company has adopted organic business strategy for its growth in variable frequency market. For instance, in April 2018, to extend the performance spectrum of the synchronous reluctance drive system, Siemens has expanded its product portfolio of Simotics synchronous-reluctance motors by including two new shaft heights, AH90 and AH225. These motors are available in a power range of 0.55–45 kilowatts (kW) and at a speed of 1,500 and 3,000 revolutions.

Browse Related Reports:

Marine VFD Market by Type (AC Drive, DC Drive), Voltage (Low Voltage (Up to 1 kV), Medium Voltage (Above 1 kV)), Application (Pump, Fan, Compressor, Propulsion / Thruster, Crane & Hoist) and Region – Global Forecast to 2024

Switchgear Market to Hit $88.5 Billion by 2025; Rising Investment in Rrenewable Energy Worldwide to Augment Growth

Servo Motors and Drives Market by Offering (Hardware, Software and Services), Product Type (Servo Motors, Servo Drives), System, Voltage, Communication Protocol, Brake Technology, Material of Construction, Industry, and Region – Global Forecast to 2025